While the challenges facing the foodservice industry in the GCC are more complex than regional operators have had to deal with in the past, the right strategies can put them on the path for long-term, sustainable growth (check out our Middle East Restaurant Growth insights).

Margins in GCC Decline but Remain Higher than Global Average

It’s time both investors and executive management teams come together to discuss how to optimize their operations in light of the new normal.

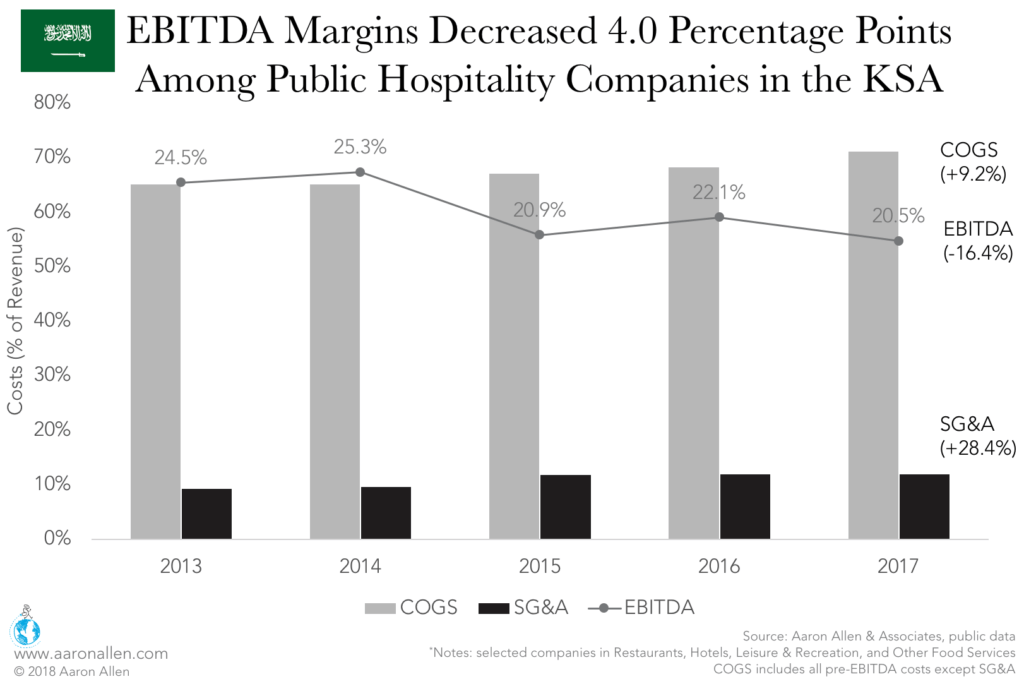

Once, EBITDA margins in the mid- to high twenties were not only frequent, they were expected. No longer (and this has led to disillusionment and an understandable but unnecessary despondence).

Once, EBITDA margins in the mid- to high twenties were not only frequent, they were expected. No longer (and this has led to disillusionment and an understandable but unnecessary despondence).

While MENA may have the fastest falling margins among major foodservice economies around the world, it’s still performing at high levels. Saudi restaurants averaged 20.5% EBITDA margins in 2017 while publicly traded restaurants in the U.S. claimed just 13.3%.

Macroeconomic Conditions Making It Harder to Grab Top-Line Growth

Between 2000 and 2015, GDP growth in the GCC averaged 5.1% annually. This rapid expansion allowed restaurants to capture large revenue growth and margins. However, as growth moderates — GDPs are forecasted to increase by an average of 2.5% until 2023 — disposable income will follow suit. Organic revenue growth through same-store sales won’t come as easily as it did before.

Food Costs Falling but Will Follow Oil Prices

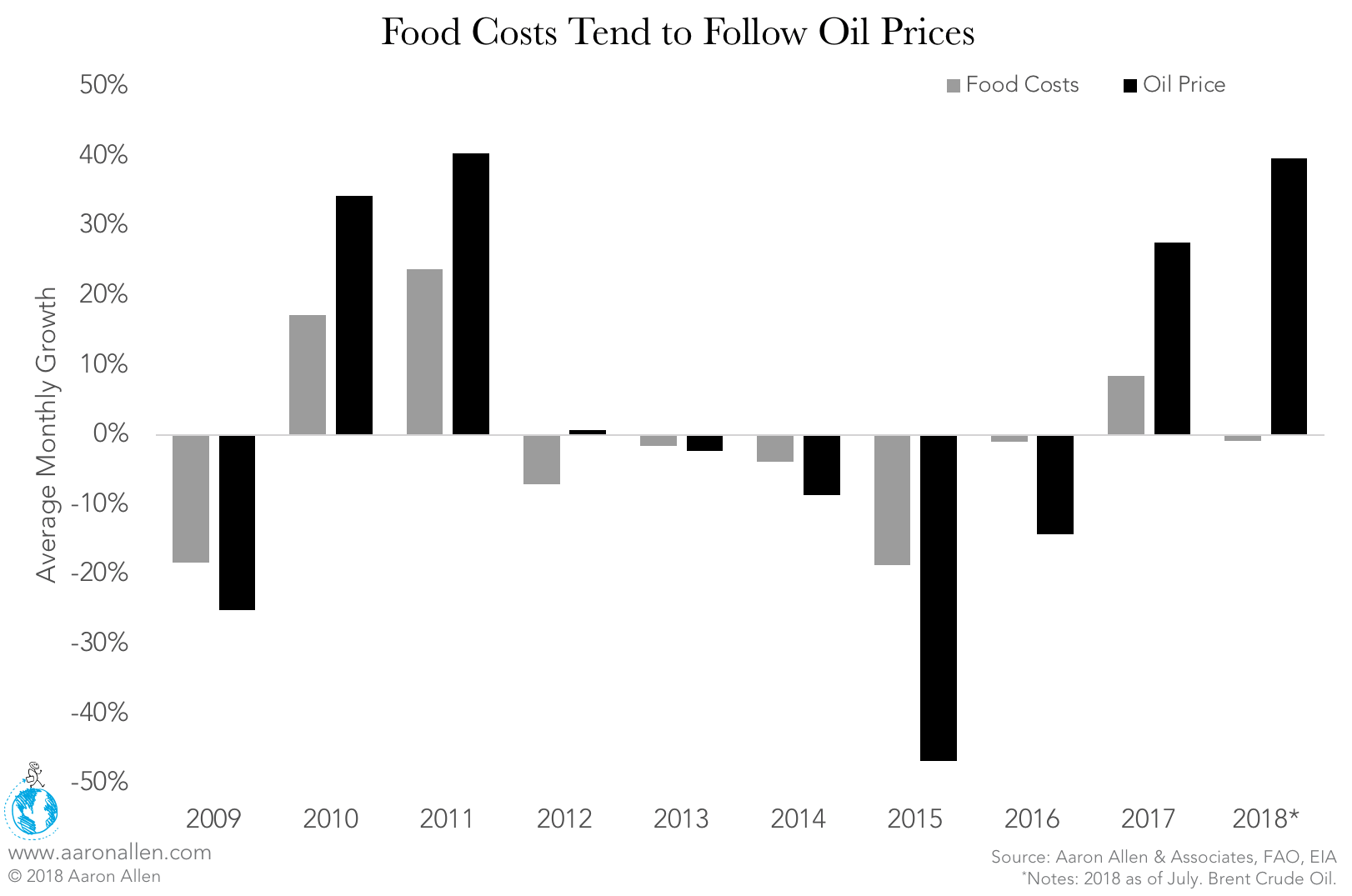

In eight of the last nine years, food costs globally have moved in the same direction as oil prices: rising alongside the price per barrel in 2010 and 2011, then falling (albeit less steeply) in 2015.

In eight of the last nine years, food costs globally have moved in the same direction as oil prices: rising alongside the price per barrel in 2010 and 2011, then falling (albeit less steeply) in 2015.

In 2017, food costs rose slightly, but, in 2018, they’ve fallen behind, with oil prices climbing 40% so far and food prices stagnating. These lower food costs have been offset by rising labor and occupancy costs.

Labor Costs Are Rising

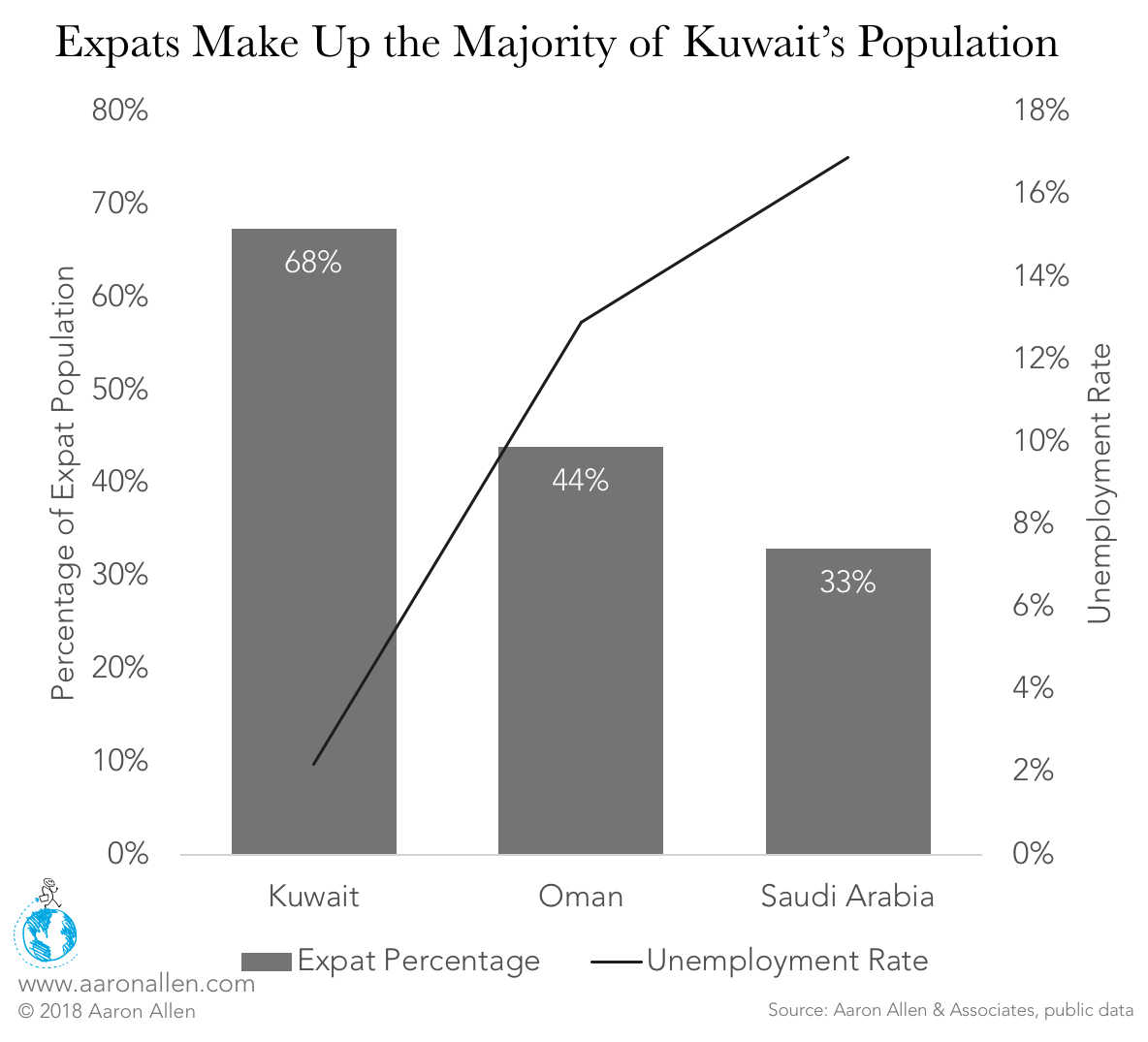

As several GCC nations continue to work to nationalize their workforces and address unemployment, the governments of Saudi Arabia, Oman, and Kuwait are implementing several initiatives to make it less attractive for companies to hire expats.

While reducing the number of expats should decrease unemployment among citizens, it will also raise labor costs. In the KSA, average wages in the private sector have increased every year since 2009. Between 2015 and 2017 the average annual increase was 4.6%. These increases are more expensive for Saudi nationals, whose minimum wage is SR5,300 ($1,412) compared to SR2,500 ($666) for expat workers. Oman has no minimum wage for expat workers, but nationals must earn at least OMR 325 ($844) a month.

While reducing the number of expats should decrease unemployment among citizens, it will also raise labor costs. In the KSA, average wages in the private sector have increased every year since 2009. Between 2015 and 2017 the average annual increase was 4.6%. These increases are more expensive for Saudi nationals, whose minimum wage is SR5,300 ($1,412) compared to SR2,500 ($666) for expat workers. Oman has no minimum wage for expat workers, but nationals must earn at least OMR 325 ($844) a month.

As a result of these changes, an estimated 730,000 non-Saudis have left the KSA’s workforce, which not only cuts into restaurants’ labor pool but also affects their revenue. For expats, average spend on food away from home is $500 per capita, so 730,000 fewer expat workers could translate into as much as $365m in annual lost revenue for restaurants. In Kuwait, which is calling for the exit of one million expats, the foodservice industry can expect an even larger impact on revenue.

Rent is Coming Down, at Least for Now

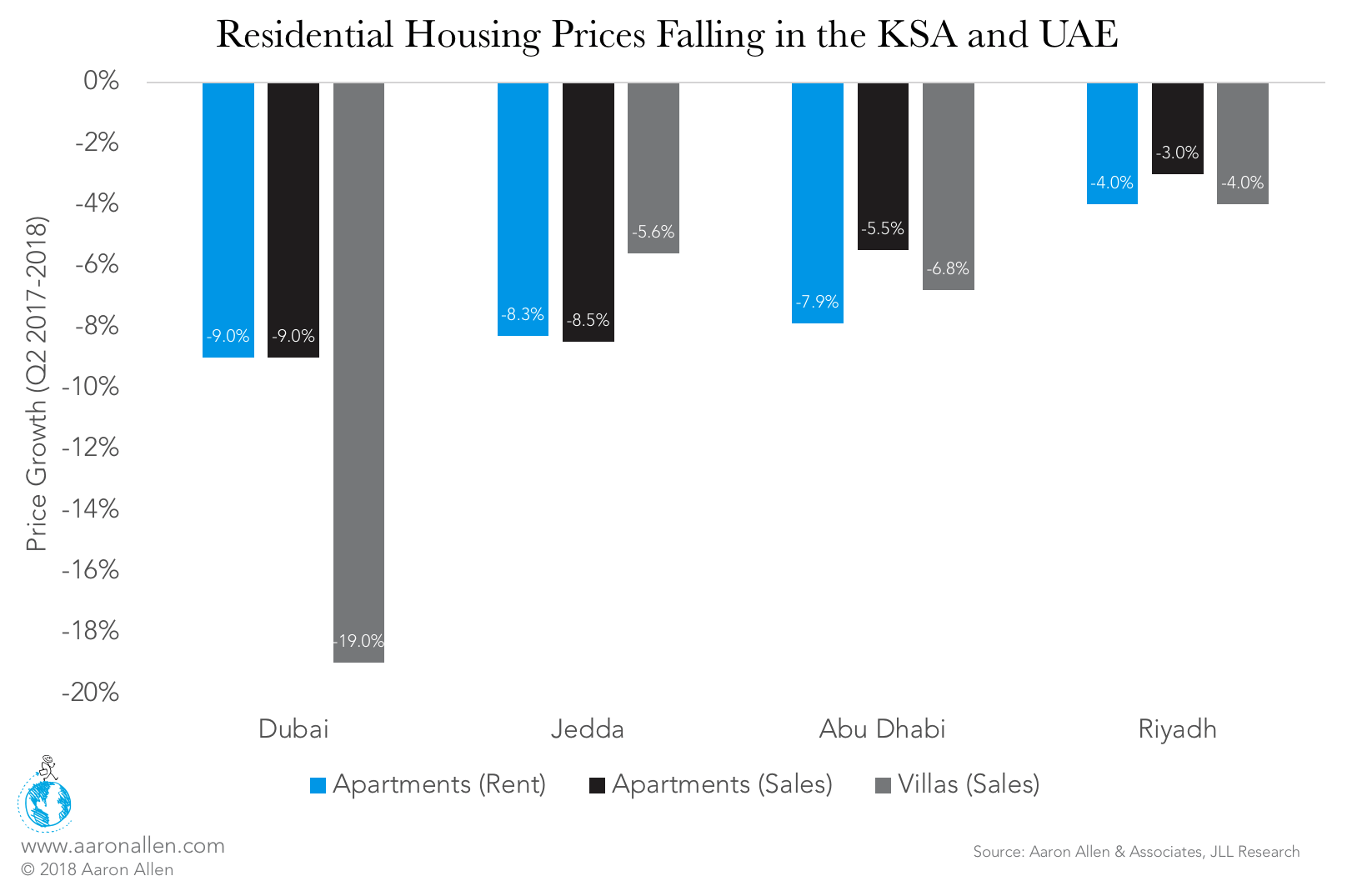

Restaurants will benefit from falling housing costs: as both rent and sale prices drop, consumers will have more to spend on dining out.

Restaurants will benefit from falling housing costs: as both rent and sale prices drop, consumers will have more to spend on dining out.

Commercial occupancy costs have also come down, but not because of increased supply or reduced demand. Rather, restaurants, retailers, and other mall tenants have pushed back against the exorbitant prices.

Two developing trends will impact rent prices in malls over the next decade. On the one hand, convenience is becoming a stronger driver of consumer behavior than the mall experience, so we expect to see these locations become less popular among foodservice operators. (See “Think Outside the Mall,” below.) But, as Gen Z becomes a stronger force in the market, the demand for mall space may once again go up. Despite being digital natives, these young people are reviving brick-and-mortar retail: though they rely on their smartphones to connect with influencers and to research products, many are as hesitant as baby boomers to buy something without seeing it in person.

Potential Paths to Increased Revenue

In developed markets, growth in foodservice typically mirrors increases in GDP, population, inflation, and disposable income. In emerging markets like the GCC, many more factors can play a role in the size of the pie — and who gets the biggest slice.

Consumer Spend Per Capita on the Rise

Growth in GDP per capita is expected to accelerate in 2018, which means more money in more people’s pockets — some of which is destined for restaurants.

Growth in GDP per capita is expected to accelerate in 2018, which means more money in more people’s pockets — some of which is destined for restaurants.

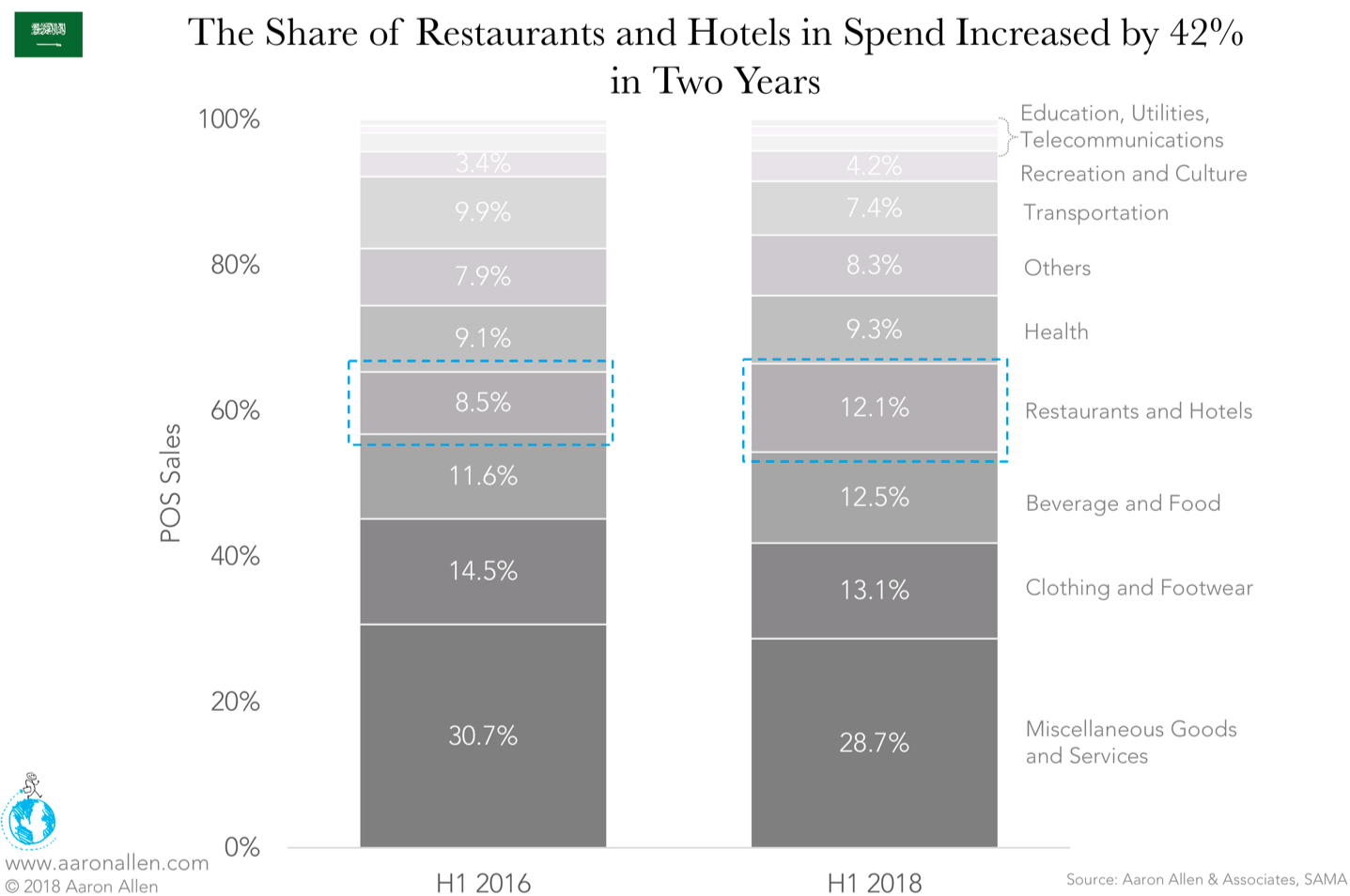

Based on credit-card transactions, restaurants in the KSA are claiming both a greater share and a greater amount of consumer spending. In H1-2018, restaurants and hotels received 12.1% of consumer discretionary spending, a 42% increase in share when compared to the same period in 2016.

Chains Gaining Strength, Cannibalizing Less Sophisticated Independents

In both the UAE and KSA, independents account for about 80% of restaurants. However, chains are expanding much faster, growing their footprints 2.3x as fast as independents. Of the 5,500 new units projected to open by 2020, chains will claim 40% of the growth, taking about 900 potential new units away from independent operators. Chains are slowly but surely shifting the weight of the industry in their direction.

During this period of growth, the players that make the smartest investments in technology, complete strategic acquisitions, and build systems that satisfy shifting competitive and consumer trends won’t just steal market share from independents, they will also cannibalize competing chains that can’t keep up.

During this period of growth, the players that make the smartest investments in technology, complete strategic acquisitions, and build systems that satisfy shifting competitive and consumer trends won’t just steal market share from independents, they will also cannibalize competing chains that can’t keep up.

These chains’ market share is already significant — the biggest ten account for around 10% of foodservice sales — but developed economies have even higher rates of consolidations. In North America, the top ten brands account for 21% of the market.

Focus Essential to Successful Large Portfolios

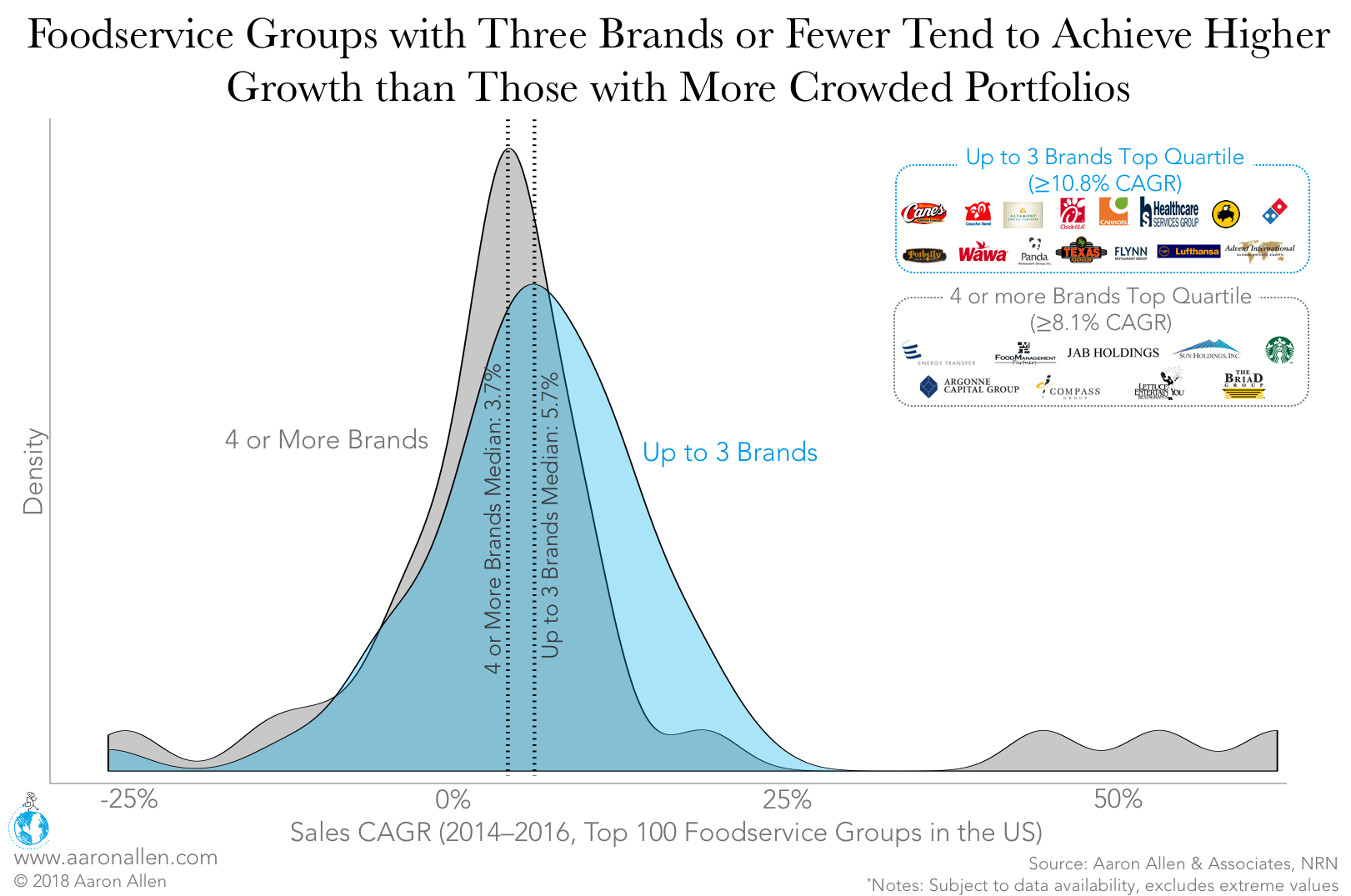

Though acquisitions are proven growth drivers, an under-performing brand can become a costly drag on a portfolio. Among publicly traded restaurant companies in the U.S., more focused conglomerates had higher CAGRs than groups with more concepts.

Of course, some large portfolios — such as JAB Holdings, which owns eight foodservice brands — perform very well. JAB has remained focused on one segment within the foodservice industry (coffee), giving them an advantage over portfolios with stakes across categories. Its subsidiary, Keurig Green Mountain, just purchased Dr. Pepper Snapple Group, which will create a merged beverage company with a combined $11b in annual revenue.

Of course, some large portfolios — such as JAB Holdings, which owns eight foodservice brands — perform very well. JAB has remained focused on one segment within the foodservice industry (coffee), giving them an advantage over portfolios with stakes across categories. Its subsidiary, Keurig Green Mountain, just purchased Dr. Pepper Snapple Group, which will create a merged beverage company with a combined $11b in annual revenue.

In MENA, two of the largest foodservice operators have 20 or more brands in their portfolio, and at least five have more than ten concepts. As the restaurant industry in the region consolidates, it likely won’t be the group with the most brands that wins. The winner will be the group with the best acquisition strategy.

If knowledge is power, buying more of it is the smartest move. Market research helps executive teams understand the factors and forces driving the foodservice industry so that they can anticipate the moves and countermoves of their competitors — both the ones they know about and the ones that may not be on the radar.

Meanwhile, installing dashboards that provide the right reports and the right KPIs at the right time will move knowledge beyond the qualitative and anecdotal to the quantitative and data-driven, giving executives a clear-eyed and objective perspective on their operations. These diagnostic tools provide transparency and accountability, allowing leaders to evaluate the whole organization in real-time.

The fast-moving GCC market has encouraged quick decision making and short-term goal setting. As markets continue to mature and stabilize, the organizations that look further into the future will have greater success. Strategic planning programs that find, define, and deploy the initiatives that will have the biggest impact on the organization can help executives envision two, ten — even 25 years — into the future.

It’s essential, however, that these plans be tailormade. Just because someone walks into the boardroom with a shoebox full of another company’s training manuals and strategic initiatives doesn’t mean they have the capabilities to adapt them, much less recreate them in a fit-for-purpose way that aligns with the brand’s unique value proposition and moves it toward its goals. Instead, leaders end up with a counterfeit strategy that’s a mimic of someone else’s masterfully conceived plans, as ill-fitting as a stranger’s bespoke wardrobe.

Having a long-term strategy informed by a complete understanding of operations, competition, and market conditions doesn’t count for much unless it can be effectively communicated both within the organization and out to guests and the media. Developing robust corporate communications departments will set successful businesses in the GCC apart from competitors and quickly become mandatory as Western standards of journalism begin to prevail in the region.

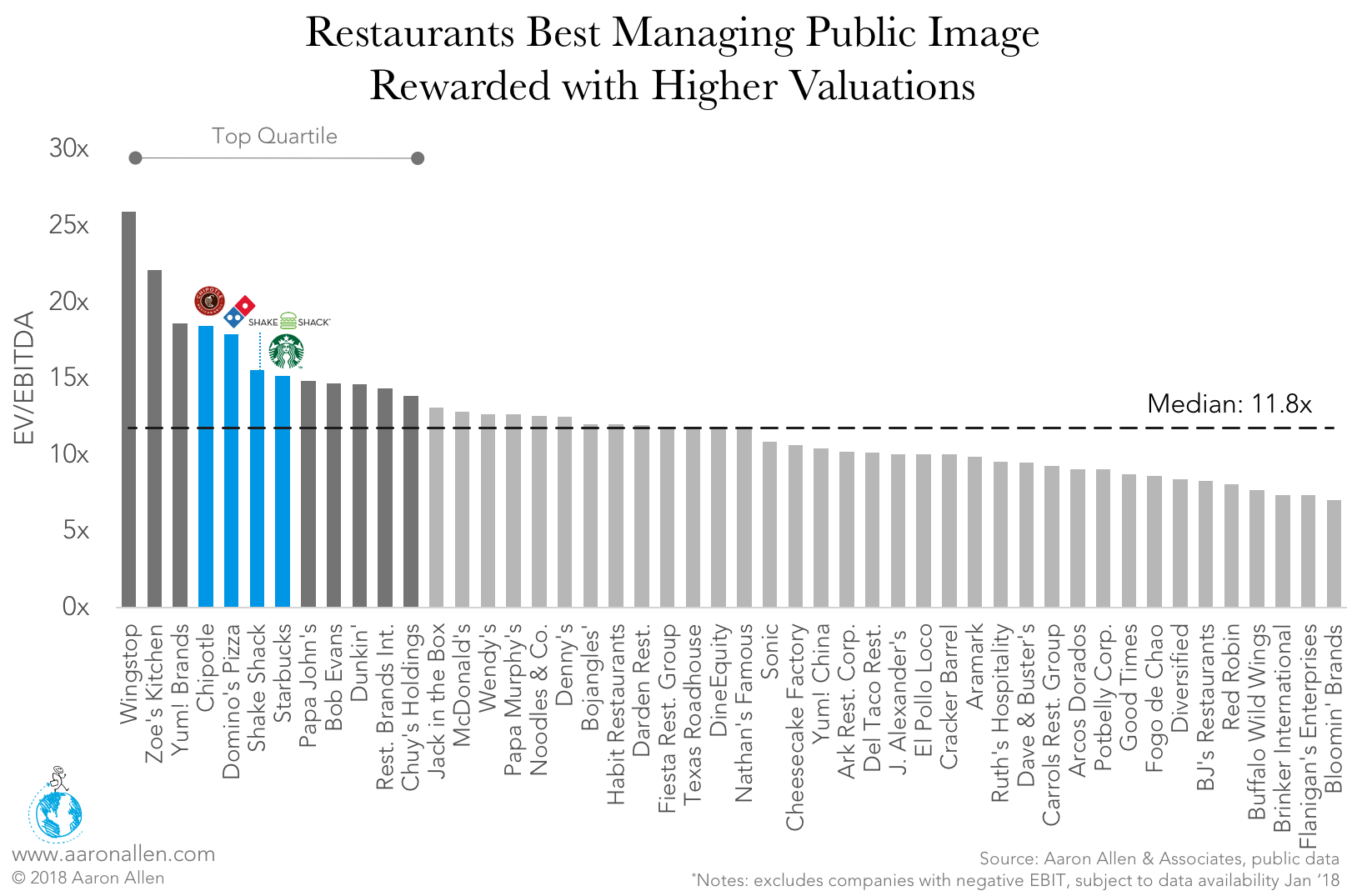

Modernizing marketing to keep pace with the number of new channels for communicating with guests and media is one of the more urgent tasks facing operators in the GCC. Marketing is invaluable not just for reaching new and existing guests but also for building valuations: the organizations with well-managed public images reap EV/EBITDA multiples 15x and above.

Modernizing marketing to keep pace with the number of new channels for communicating with guests and media is one of the more urgent tasks facing operators in the GCC. Marketing is invaluable not just for reaching new and existing guests but also for building valuations: the organizations with well-managed public images reap EV/EBITDA multiples 15x and above.

Even without hiring a team to handle social and earned media, however, these companies will benefit from simply reallocating their budgets. The global average for yearly marketing spend in restaurants is 3% of revenue (though some leading chains in the region devote up twice that), and organizations that cut their marketing budgets significantly — or entirely — during the downturn will have to catch up to compete. No matter where their annual spend on marketing currently sits, most operations will benefit from making capitalized expenditures in order to modernize their capabilities.

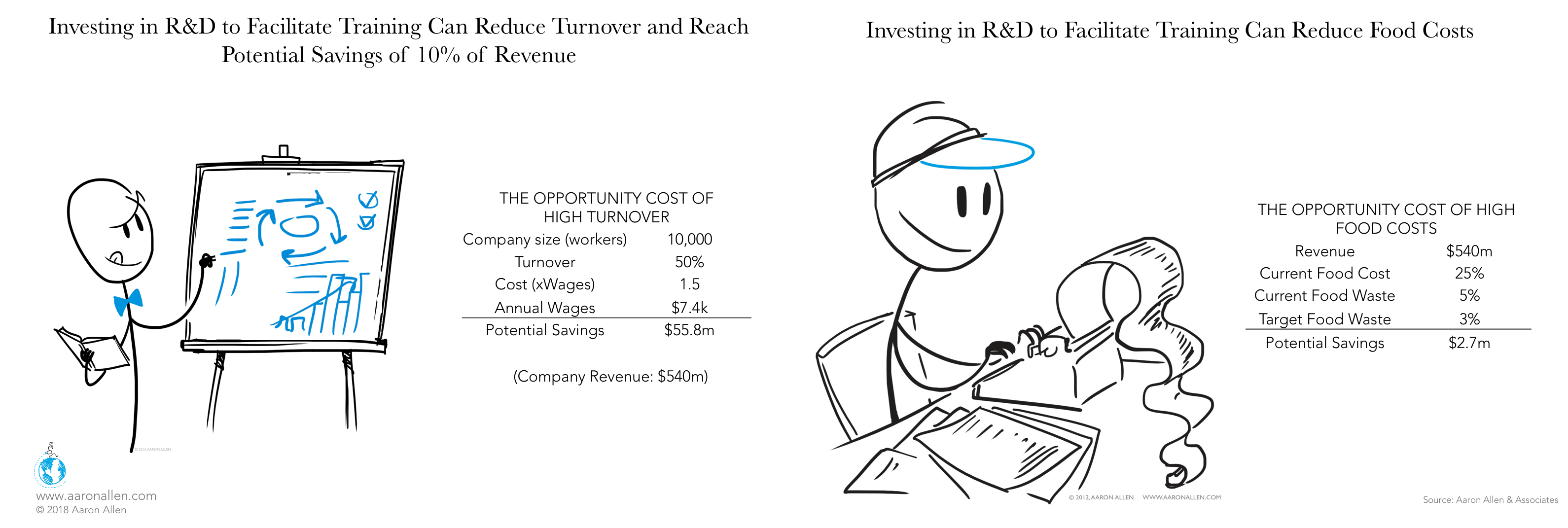

Many regional foodservice operations see training crew-level employees as an unnecessary investment, but the organizations that choose to forgo the expense are most likely paying for it other ways: untrained (or poorly trained) cooks and servers impact the P&L statement in lots of ways, from food that has to be thrown away because it was prepared incorrectly to guests who will never return thanks to bad service.

Proper training can reduce food costs by 0.5% of revenue. This figure may seem insignificant until you imagine it across a $1b system. In that instance, a training program focusing just on preventing food waste could save the operation $5m annually. Restaurants that don’t invest in training also tend to have higher rates of turnover. Since the cost of replacing an employee is about 1.5x their wages, a 50% turnover rate would drain about 10% of the revenue from an operation. Most training programs cost only half that.

The lack of training speaks to a commonplace perception in the region: working in foodservice is a dead-end career. The U.S. restaurant industry once faced a similar challenge, until the National Restaurant Association (NRA) developed a vocational program that effectively linked the practical skills needed to work in foodservice operations with career development opportunities. The organizations in the GCC that create equivalent programs will not only benefit from more efficient labor models but will also play an important role in easing national unemployment rates, furthering the industry as a whole, and improving the perception of service.

The best, surest way to cut costs is to increase sales. And the surest way to increase sales is to invest in the existing operation. Most foodservice systems are aware that their operations have inefficiencies, a few drags on the operation, but these agitations and pain points haven’t become prominent enough to be prioritized as necessities. Instead, they remain chores that the company hopes to get around to someday. But taking care of these nagging issues can quickly increase same-store sales.

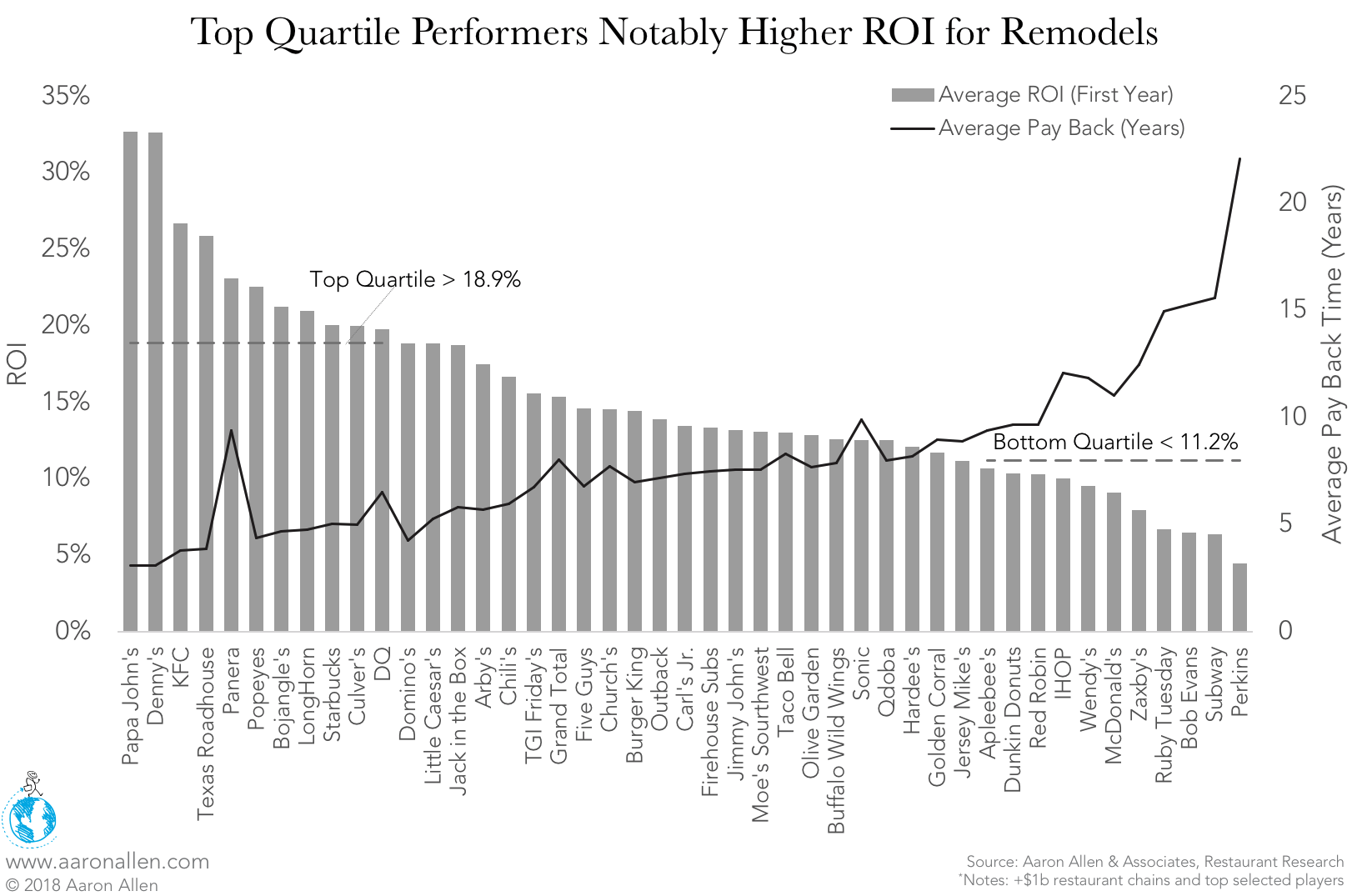

Performing basic repairs and maintenance, improving cleanliness standards, and conducting QA/QC audits can lead to fast same-store sales gains. Remodels, if done correctly, can create average sales lifts of between 3% and 10%, depending on the category. In the U.S., these initiatives get an average 15% ROI, with top performers reaching 18.9% and higher. Leveraging organizational design, industrial engineering, and branding into the creation of store of the future prototypes will allow operations to bake greater efficiency and consumer relevance into each location.

Performing basic repairs and maintenance, improving cleanliness standards, and conducting QA/QC audits can lead to fast same-store sales gains. Remodels, if done correctly, can create average sales lifts of between 3% and 10%, depending on the category. In the U.S., these initiatives get an average 15% ROI, with top performers reaching 18.9% and higher. Leveraging organizational design, industrial engineering, and branding into the creation of store of the future prototypes will allow operations to bake greater efficiency and consumer relevance into each location.

Considering the economic downturn that operations in the GCC face, it may be hard to convince boards and other C-Suite staff to commit to new investments. After all, they’ve been watching revenues and margins fall for three years, so caution is justified. But this penny pinching is part of what’s squeezing margins, as operations try to make more efficient that which shouldn’t be done at all rather than making the investments into people, process, plant and physical environment, and professional services that will create a more secure future for the organization.

Early movers will have the opportunity to acquire full regional rights or a territory buy-out of best-fit future brands. In contrast to the acquisition and franchise strategies that have prevailed in the GCC previously, these purchases should be based on a proper mandate, rather than the desire to accumulate short-term wins. The goal is not to have the biggest portfolio, but rather to build a portfolio that attracts the largest and most loyal audience.

Other areas of the industry, specifically catering and contract foodservice, offer opportunities for consolidation. In Western markets, one or two large brands control the majority of the share of foodservice operations in airports, hospitals, and schools. The organization that begins consolidating these services in the GCC — particularly in airports, many of which are expanding to accommodate the increasing number of tourists — could combine them into a large system with sustainable growth potential.

Arguably, franchise brands are easier to manage because systems and standards are already in place. But they often turn out to be more expensive, between paying out franchise fees and missing out on the benefits of enhanced valuation. Moreover, an emerging consumer trend, among both domestic guests and tourists, is the desire to experience an authentic sense of place. (Al Baik’s cult-like popularity attests to this development.)

There is an area of opportunity for homegrown concepts and flavors to flourish, and potentially be exported globally, which would open up new lines of revenue for GCC operators. For example, 20% of Domino’s 2017 revenue came from royalties. International franchisees pay an average of 3% of sales in royalties, so, with more than 9k international stores, the pizza chain earns an average fee of $22.3k per location every year.

Technology will soon become an essential component of the restaurant industry, and the underlying infrastructure is one of the most significant areas of opportunity for both regional operators and technology companies. Over the next three to five years, hundreds of billions of dollars will shift within the $2.7t global foodservice industry, as guests seeking convenience, accuracy, and speed will buy more from companies or through channels that provide those services.

From mobile ordering and self-service kiosks to predictive analytics and automated kitchens, the restaurants that install these innovations first will likely win a disproportionate amount of market share and reap stunning valuations in the process. Tech companies that create and license these products can expect a boom, as operations unequipped to develop technology in-house will turn to them for help.

While there has been a recent downward trend in occupancy costs, there is still a need for operators to look beyond what will once again be very high retail rent costs. Though the prestige of new shopping centers has been an important factor in real-estate decisions, guests’ desire for convenience will soon matter just as much as securing a location in a newly opened or highly trafficked mall.

Delivery-only locations, pop-up kitchens, food halls, and other non-traditional formats are something to be considered. Different location types will not only optimize occupancy costs, they will also create new dining experiences, offering another way for brands to stand out.

While there has been a recent downward trend in occupancy costs, there is still a need for operators to look beyond what will once again be very high retail rent costs. Though the prestige of new shopping centers has been an important factor in real-estate decisions, guests’ desire for convenience will soon matter just as much as securing a location in a newly opened or highly trafficked mall.

Delivery-only locations, pop-up kitchens, food halls, and other non-traditional formats are something to be considered. Different location types will not only optimize occupancy costs, they will also create new dining experiences, offering another way for brands to stand out.Over the next 5+ years, food sustainability will play a major role in national economic diversification programs. These efforts aim to make GCC countries less reliant on imported foods, even moving them toward exporting agricultural products.

Though governments are leading these efforts, food sustainability initiatives provide new opportunities for foodservice operations, both regionally and internationally, to invest in vertical farms, aquaculture, and other ways of creating a sustainable agriculture sector in the GCC. The impact of these developments could fundamentally transform these nations’ economies and improve the health of residents.

About Aaron Allen & Associates

Aaron Allen & Associates works alongside senior executives of the world’s leading foodservice and hospitality companies to identify, size, and seize opportunities to drive growth, optimize performance, and maximize enterprise value. Our due diligence services help chained restaurant operations and private equity firms plan, evaluate, and close strategic acquisitions.

Collectively, our clients span six continents and 100+ countries, collectively posting more than $200b in revenue. Our strong specialization in the Middle East is complemented by engagements in nearly every geography, category, cuisine, segment, operating model, ownership type, and phase of the business life cycle.