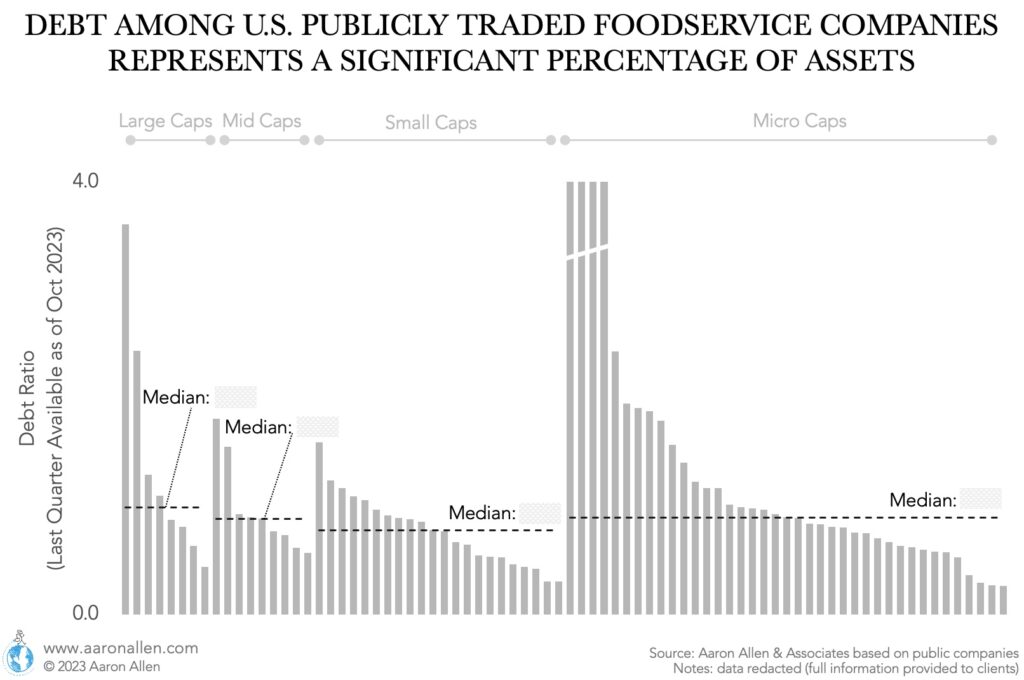

Restaurant debt represents an average 90% of assets. With these numbers, raising interest rates can be fatal for some — and fortune-building for others. This period will usher in a fresh wave of consolidation through mergers and acquisitions. In many cases, recessionary M&A involves distressed and dislocated assets that can be purchased for pennies on the dollar. However, it’s not always predatory or unwelcome. In our view, this period of change will just be accelerating the transformation that was already underway and being profitably harnessed by industry leaders.

Secondary markets allow investors or lenders to get liquidity and exit a position or an investment before the initially expected termination period. A new investor or lender will assess the value of the asset, negotiate, and offer a price to buy out the original investor. There are secondaries markets for debt as well as for private equity investments.

In this article we examine what’s happening in the markets for private debt secondaries, private equity secondaries, and how these trends affect restaurant chains in debt. Whether you are a lender, investor, operator, part of a management team, or in executive leadership, you can benefit from looking at debt through this lens.

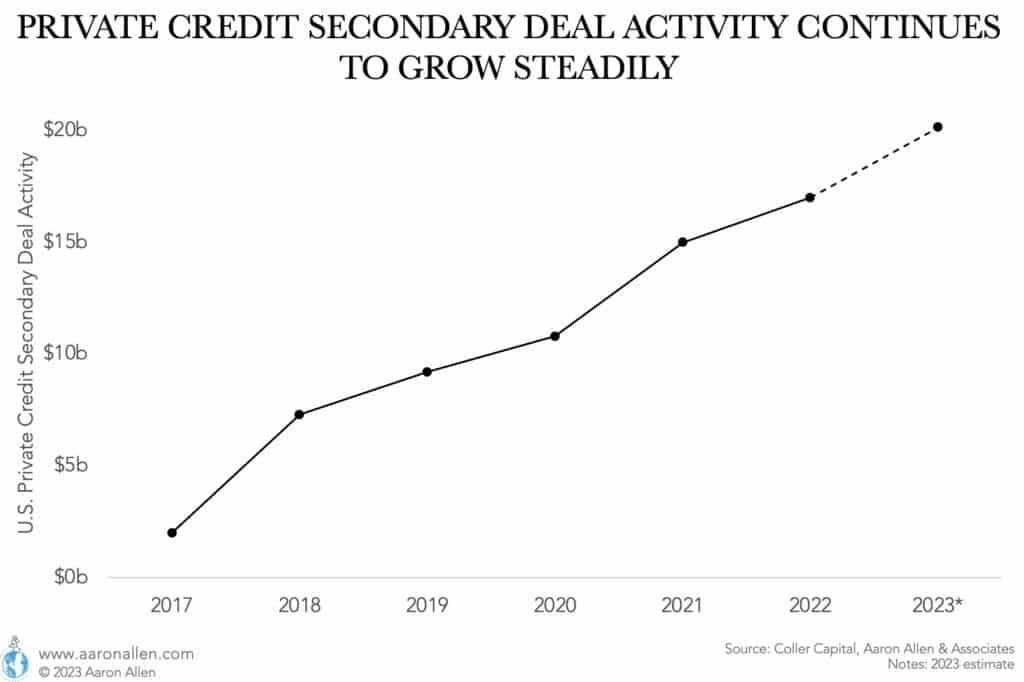

Private Debt Secondaries Are on The Rise

Private debt secondary markets activity has grown steadily over the last five years, and we expect 2023 to continue that trend. Private debt (bonds, loans, direct lending, mezzanine debt, or other credit strategies) can switch hands (likely at a discount) when the original lender is seeking liquidity and there is a buyer that can benefit from buying at a discount to the face value of the debt.

As higher interest rates cause a slowdown in loan repayments, some private debt funds are seeing limited capital inflow and have to exit some of their current positions.

The restaurant industry is no exception, and we are seeing more restaurant chains struggling with debt payments, covenants, and interest payments.

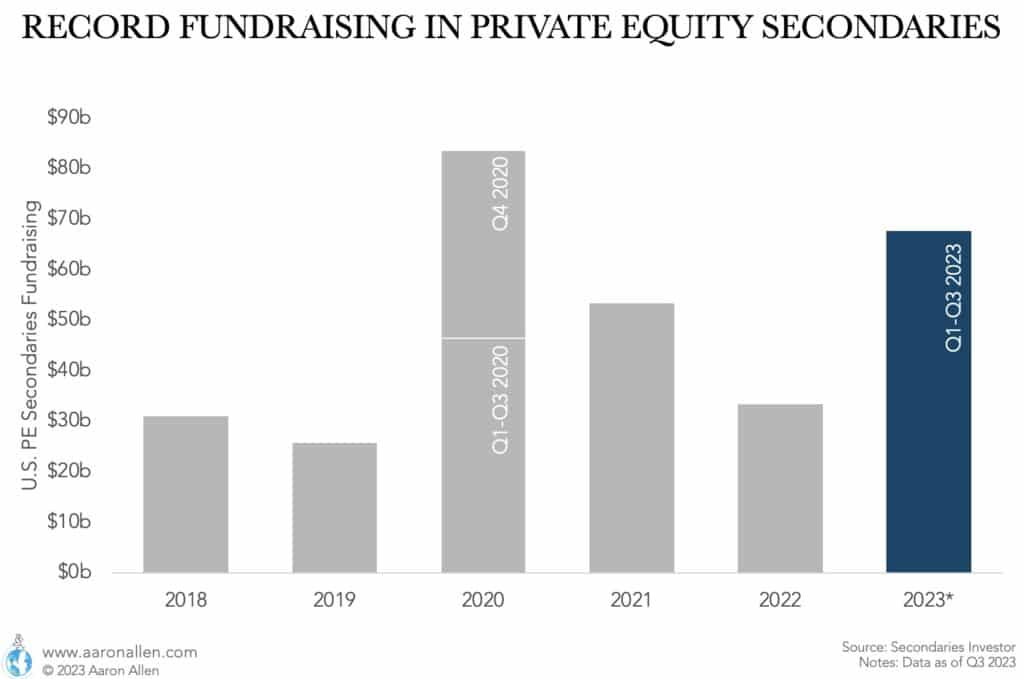

Private Equity Secondaries Funds Are Raising Record Capital

Secondaries funds raised record amounts of capital in 2023. Up to September, reports indicate that the total raised was close to $70 billion, surpassing all previous years for Jan-Sep and already surpassing the amount raised for the full year 2021 and 2022. Secondaries accounted for more than 10% of private equity fundraising, doubling the market share for the previous year.

With estimates indicating around $200 billion in dry powder, secondaries funds are actively seeking investment targets. We believe the increased activity in this market together with a slowdown in the capital raised for traditional PE vehicles is signaling a difficult 2024 to come. Investors are selling parts of their portfolios generating a new type of dealflow — and at significant discounts. For buyers, it can be a shortcut to increase exposure in certain industries (buying rather than building from scratch) and gain economies of scale.

Restaurant Debt KPIs and Benchmarks

Restaurant Debt Ratio

U.S. publicly traded restaurant companies are highly leveraged and the median debt-to-assets ratio shows no big difference between large, mid, small, and micro caps.

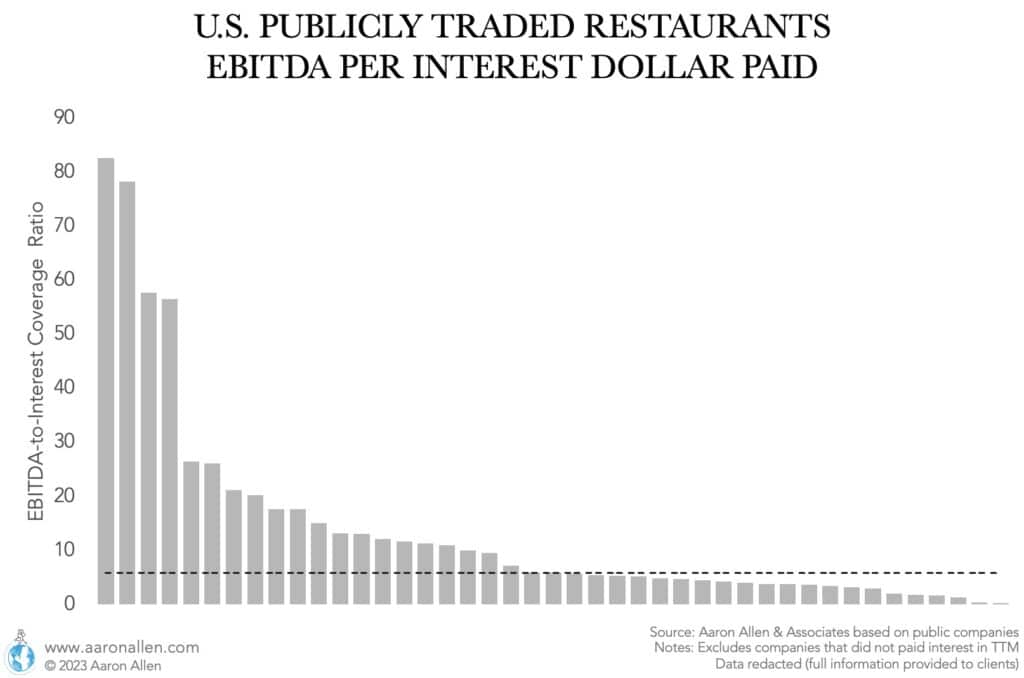

EBITDA-to-Interest Coverage Ratio

Financial metrics such as the EBITDA-to-Interest ratio help us anticipate what the situation could be for an industry in the face of rising interest rates and a potential economic slowdown. In general, an EBITDA coverage ratio of over 10 is considered good (10 dollars of EBITDA for every dollar paid in interest). In the U.S., more than a third of publicly traded foodservice companies have a ratio lower than 10.

We don’t want to see restaurant bankruptcies multiply, but it may be the time to build the top line and organize financing.

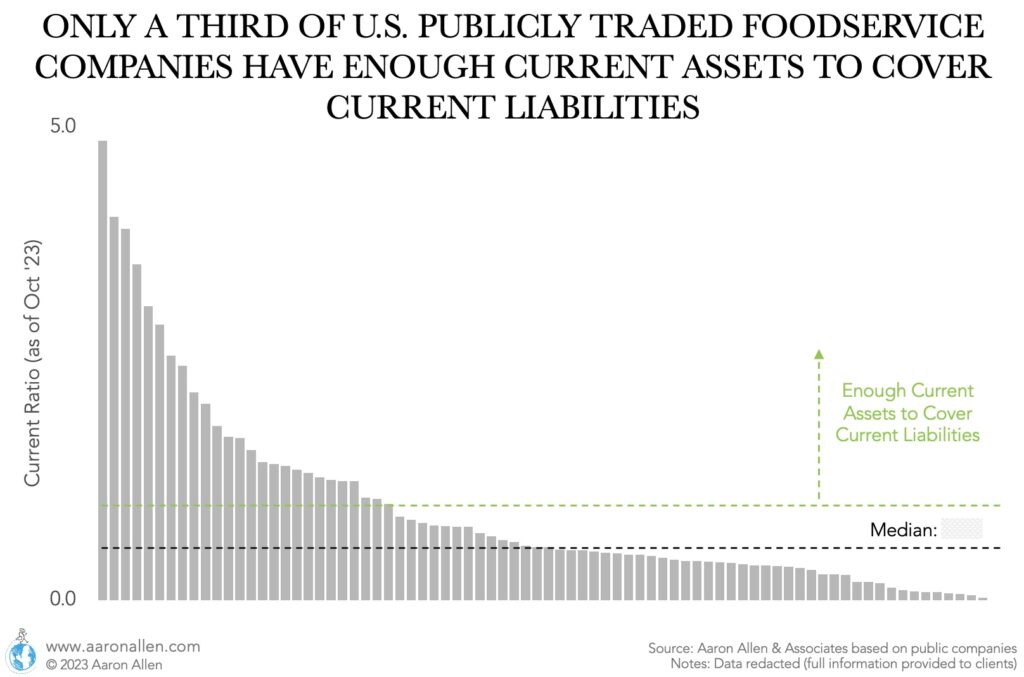

Restaurant Current Ratio

The current ratio (the total current assets of a company divided by its current liabilities) helps understand a company’s ability to pay short-term debt. In the U.S., only a third of the publicly traded foodservice companies has enough current assets to cover current liabilities. The restaurant industry tends to operate with a low current ratio, and it hasn’t changed much compared to pre-pandemic benchmarks.

However, it can be a vulnerability. If the economic situation deteriorates, for many restaurant chains investors will have to step in to solve the liquidity crisis.

The retooling that was already in motion is accelerating and the industry will look very different a few years from now.