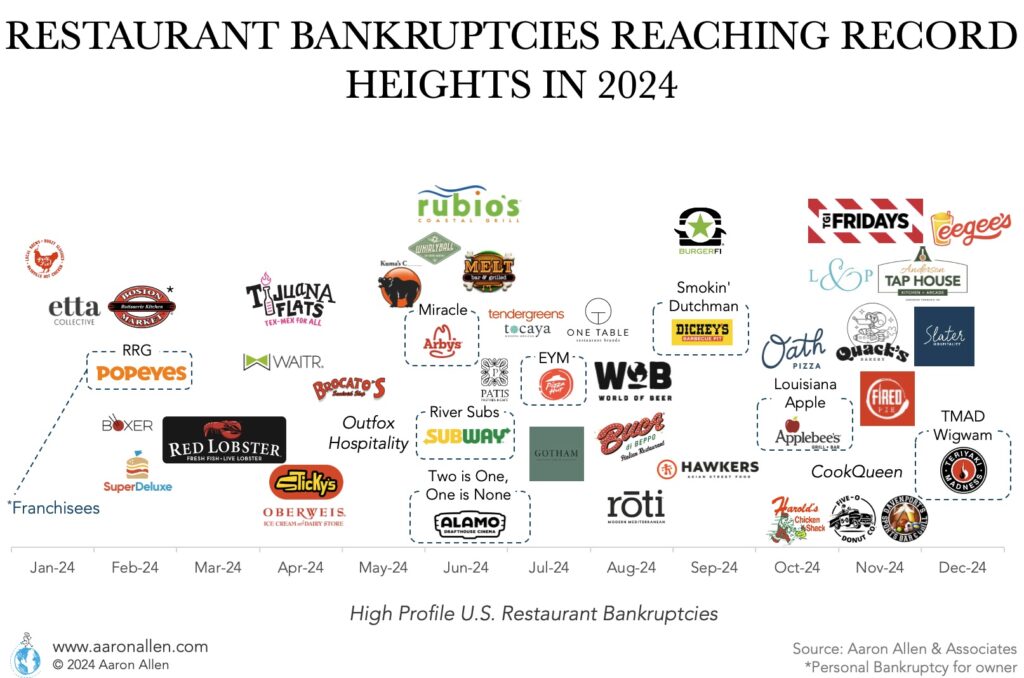

The following restaurant chains have gone bankrupt or are in a bankruptcy process between 2020 and 2024. Many still cite the pandemic as the reason for their demise and will have to liquidate their assets or be subject to massive reorganizations (though others — especially in the casual dining segment — were in trouble before Covid-19 hit).

Increases in labor costs, higher interest rates, negative same-store sales, years of negative EBITDA, flawed real estate strategies, high food prices, customers cutting down on dining out, and COVID lingering government support withdrawal are some of the factors chains and franchisees were unable to surpass and leading to a soaring number of restaurant bankruptcies in 2024.

We are seeing this play out in many geographies. Despite the pain and pressures of challenging conditions, it seems like in some organizations it hurts less to remain indecisive — holding one’s breath waiting for the situation to improve itself – than it does to bite the bullet on bolstering the team, capabilities, competencies, and critical thinking that’s needed to confront the issues head-on. It somehow hurts less to lose millions slowly over many months than to plunk down a few hundred thousand to get the shot in the arm that’s so desperately needed. Our advice? Waiting may hurt less, but it costs a lot more in the long run.

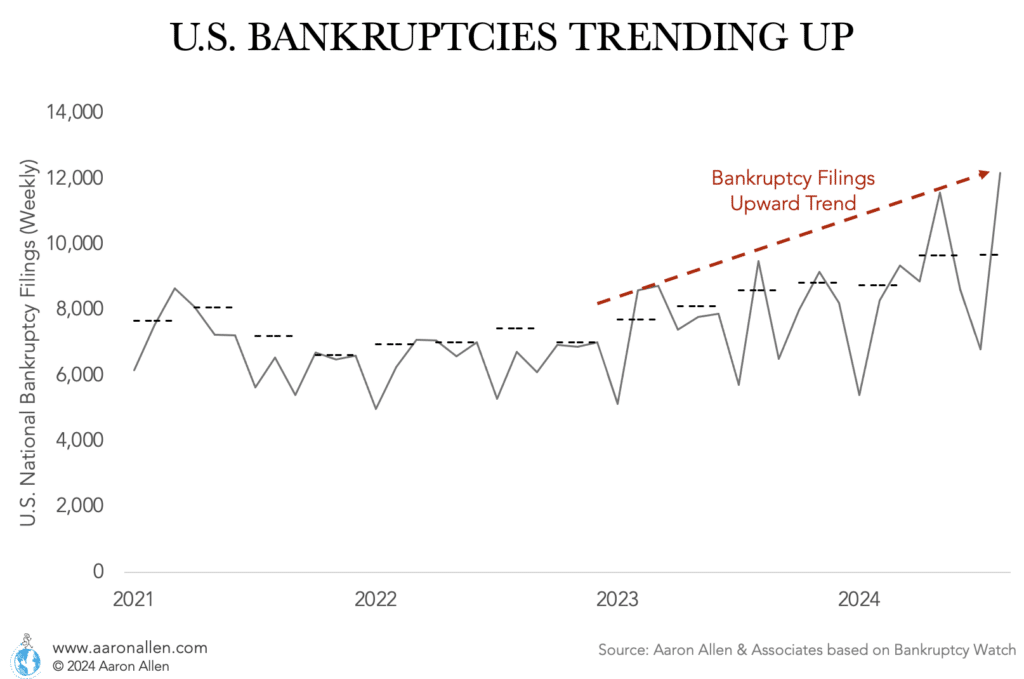

The number of struggling businesses filing for bankruptcy has been showing an increasing trend since the end of 2022. 2024 has so far shown the worst average numbers of the last few years.

And though many companies are able to restructure and continue operating, in many industries (in the restaurant industry in particular) in most cases the businesses aren’t able to bring the shine back.

It’s an imperative to develop new business models and plans ahead of sitting down with creditors. In many cases, effective turnaround plans can gain traction and confidence, but they require credibility and objectivity to convince other shareholders and stakeholders to come along. It’s essential to win not just their consent, but their renewed trust and enthusiasm for a new and inspired vision.

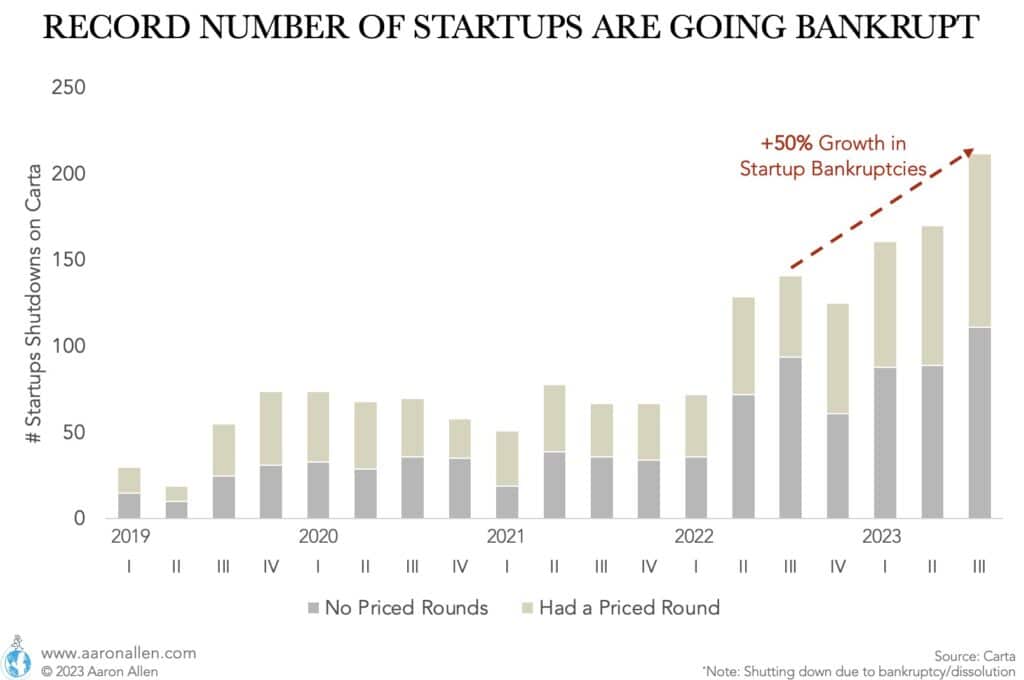

Relevant for foodservice technology companies, startups funding dried up and they are going bankrupt.

Reports are indicating that startups are seeing record levels of bankruptcies, with a 50% increase in Q3 of 2023 compared to 2022.

When you look at 2024 it’s not all doom and gloom but it’s very different from what we had in the last two years.

What should have happened during the pandemic didn’t happen because of the amount of stimulus (with governments pumping cash into the economy). As a result, bankruptcies were delayed — but here they come.

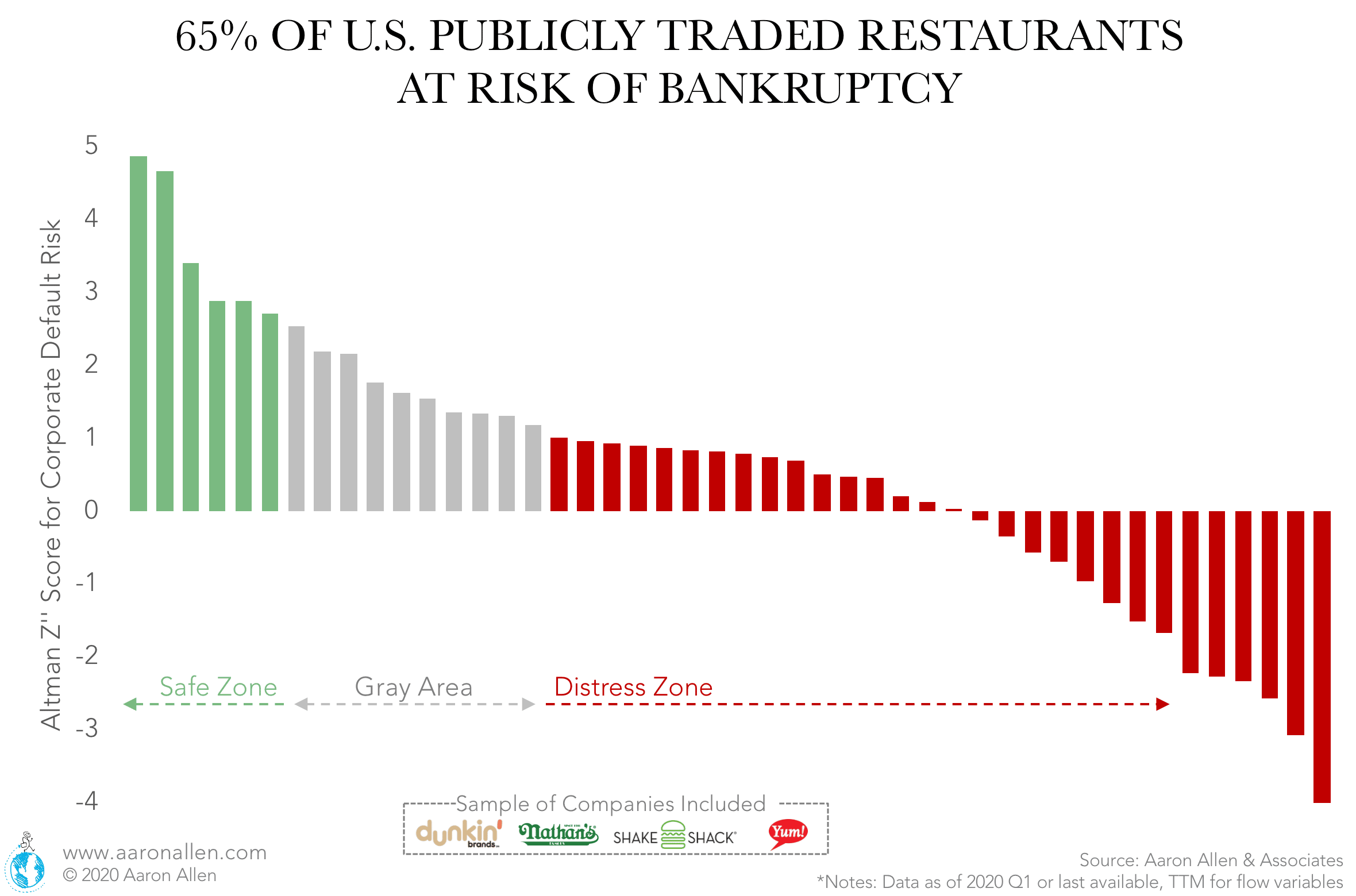

In early 2020 we conducted a study of public restaurant companies in the U.S. to assess their risk of bankruptcy in the wake of the economic uncertainty brought on by the coronavirus pandemic. This analysis is based on a calculation called the Altman-Z” Score (a variation of the Altman-Z Score which is commonly used to calculate the credit strength of manufacturing companies), based on key financial metrics including: Current Assets, Current Liabilities, Total Liabilities, EBIT, Total Assets, Retained Earnings, and Book Value of Equity.

Generally speaking, an Altman-Z” Score greater than 2.6 is deemed “safe”, between 1.1–2.6 is in the “gray area,” and lower than 1.1 is viewed in the ”distress zone.” These calculations were completed in May 2020 using Q1 2020 data for U.S. publicly traded restaurant companies, or the last available data (depending on companies’ fiscal year in the analysis set).

A total of 46 companies are included in the analysis ranging service styles (QSR, fast-casual, casual dining, etc.) and both franchisee and franchisor business models. These companies total an estimated $148b in annual U.S. system-wide sales and account for 100k locations across the country. The analysis also includes Arcos Dorados and Yum! China which operate exclusively in Latin America and China, respectively. For the purposes of classification, companies considered “highly franchised” have greater than 66% franchised units system-wide, “moderately franchised” between 33–66%, and “lightly franchised” below 33%.

Some highlights of our analysis include:

We’d like to not that these are not predictions nor forecasts, but rather calculations based on working capital, retained earnings, EBIT, market value, sales, and assets. Many restaurant companies operating with different models (highly franchised systems versus wholly corporate-owned systems, for instance) have naturally varied financial metrics that impact the calculations and financial performance.

This period will usher in a fresh wave of consolidation through mergers and acquisitions. In many cases, recessionary M&A involves distressed and dislocated assets that can be purchased for pennies on the dollar. However, it’s not always predatory or unwelcome. In our view, this period of change will just be accelerating the transformation that was already underway and being profitably harnessed by industry leaders.

Those that are most optimistic often tend to be either those that are under-informed and bubbly optimists by nature — or, they are those that have done their homework and developed a silver-lining investment thesis. Foodservice is a multi-trillion dollar global industry that has remained as consistent as inflation and population growth for decades and spend has been irreversibly redirected in a single quarter — displacing and shifting hundreds of billions of dollars in global consumer discretionary spending. While it will be fatal for some and fortune-building for others.

We found that more than six every ten restaurant chains are in the “distress zone” when using this calculation (highly leveraged, low earnings, or a combination of both). While this is not a direct indicator of bankruptcy risk — and there are significant differences in operating models for these companies (franchisors versus more corporate-owned locations, etc.) — there are some fascinating findings.

Even with the injection of liquidity, it is not enough to cover what the losses are — with the industry down tens of billions per month right now it’s going to be very hard to get back, even once restaurants are at full capacity.

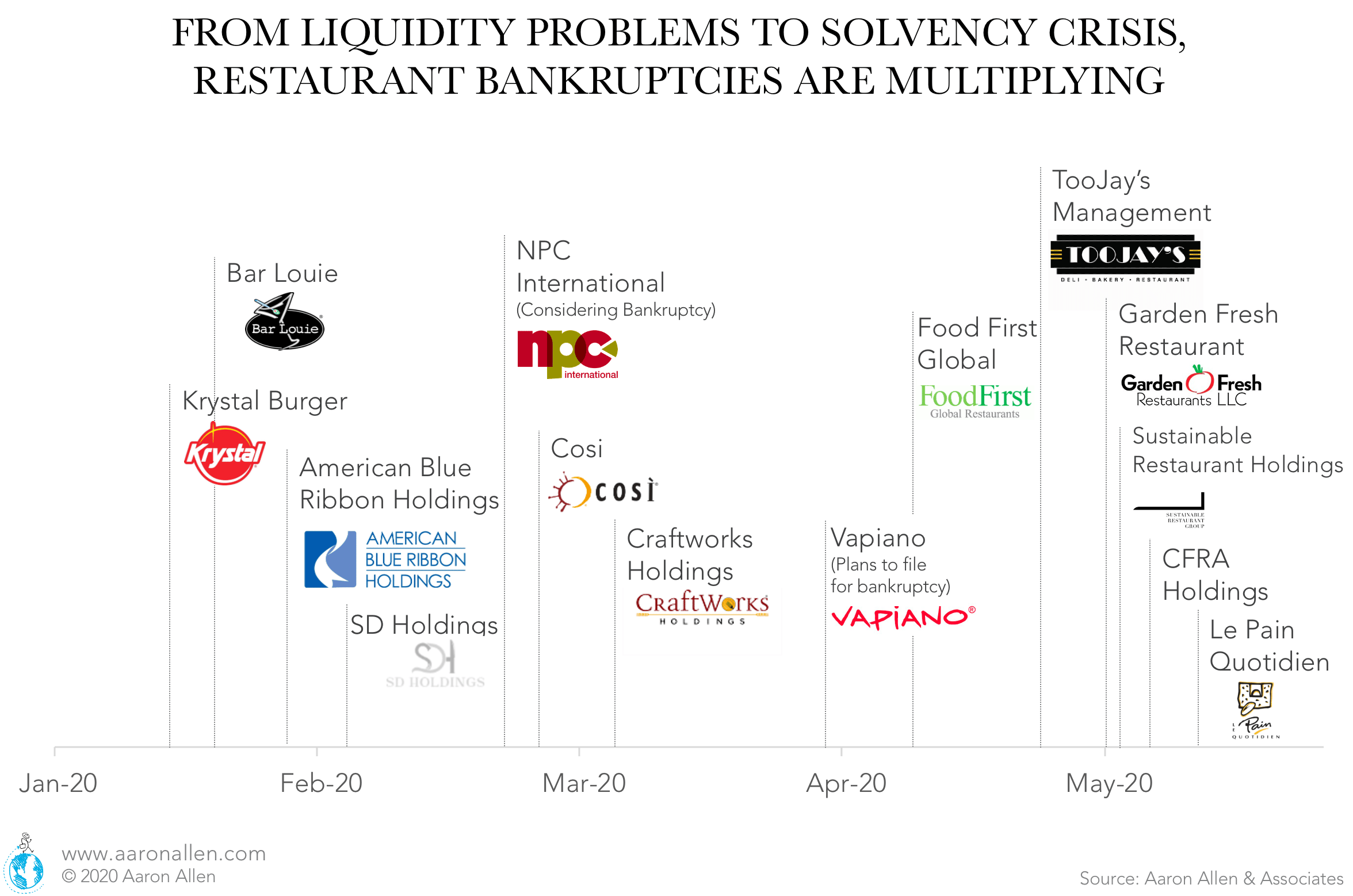

Restaurant bankruptcies are multiplying in 2020 and several chains filed for chapter 11 or debt protection across all segments: from quick-service restaurants Krystal Burger (declared bankruptcy back in January), to fast-casual chains Vapiano, Cosi and Le Pain Quotidien to buffet Garden Fresh Restaurant.

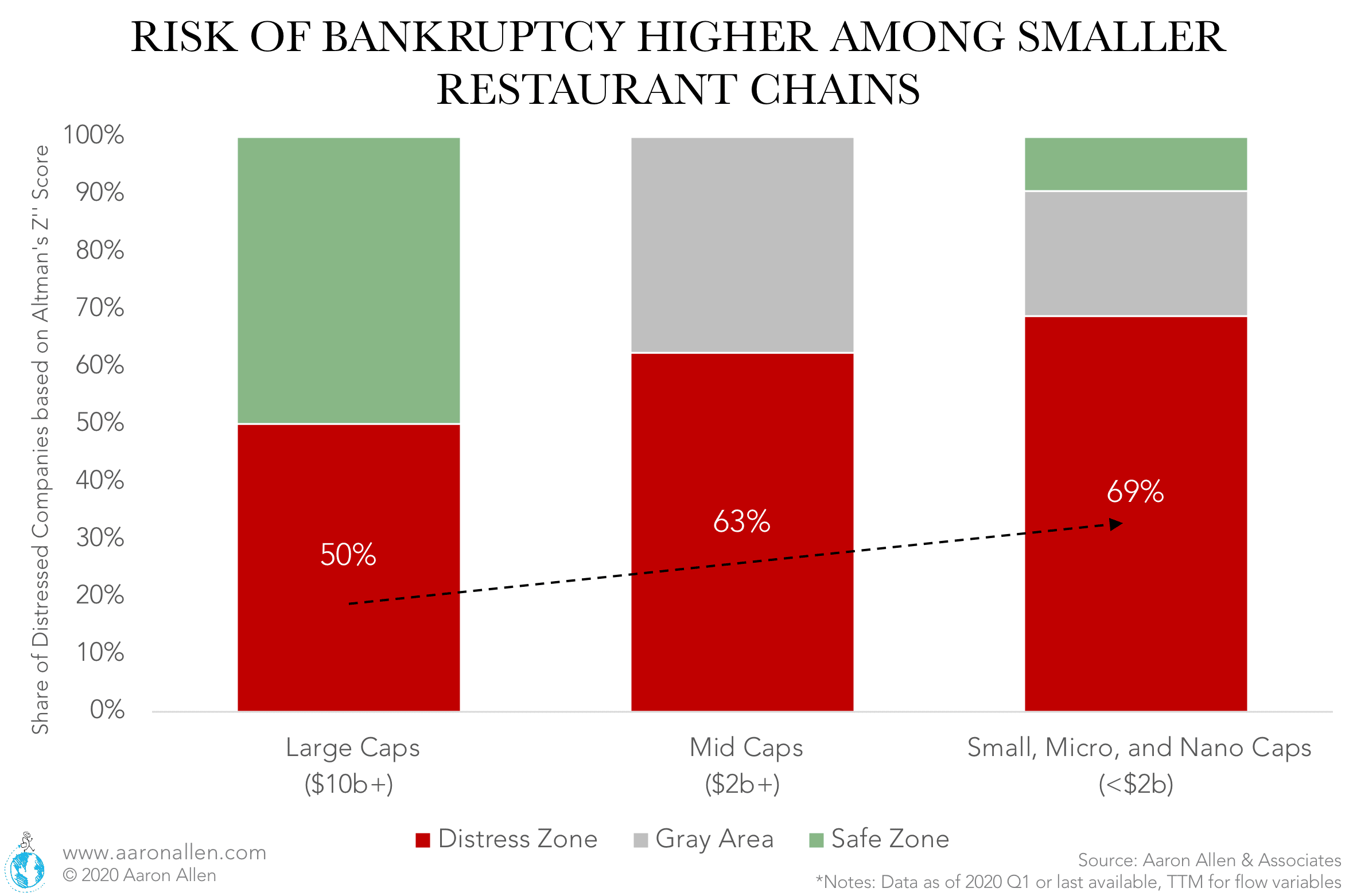

It’s usually the case that smaller companies are more vulnerable to economic shocks than large companies. Among U.S. public restaurants, the risk of bankruptcy increases by more than a third when comparing small-, micro-, and nano-caps to large caps. While 50% of large caps are in the distress zone according to Altman’s Z’’-score, the share of companies in the red zone increases to 69% for public restaurants with less than $2b in market cap.

The retooling that was already in motion is accelerating and the industry will look very different a few years from now.

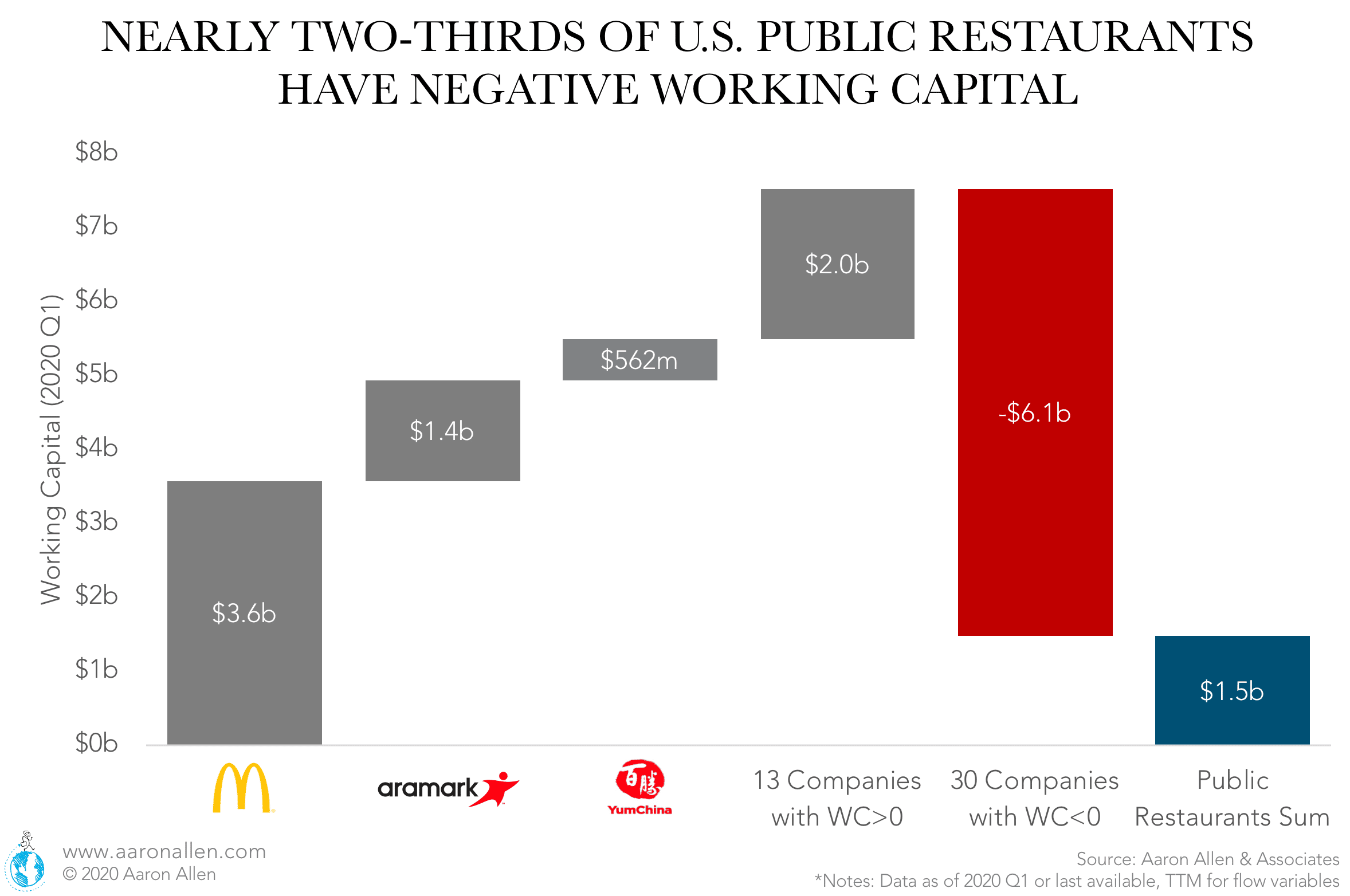

Companies with negative working capital are most likely to face liquidity issues because they lack sufficient current assets to cover current debt. In the U.S., publicly traded restaurants have a total of $1.5b in working capital (46 companies). However, 65% of chains have negative working capital (accounting for a deficit of $6.1b).

The restaurant industry received 9% of the first Paycheck Protection Program (PPP) loan batch ($31b) and it’s not nearly enough to cover what the losses are. Greater consolidation will happen than in any of the recessions before.

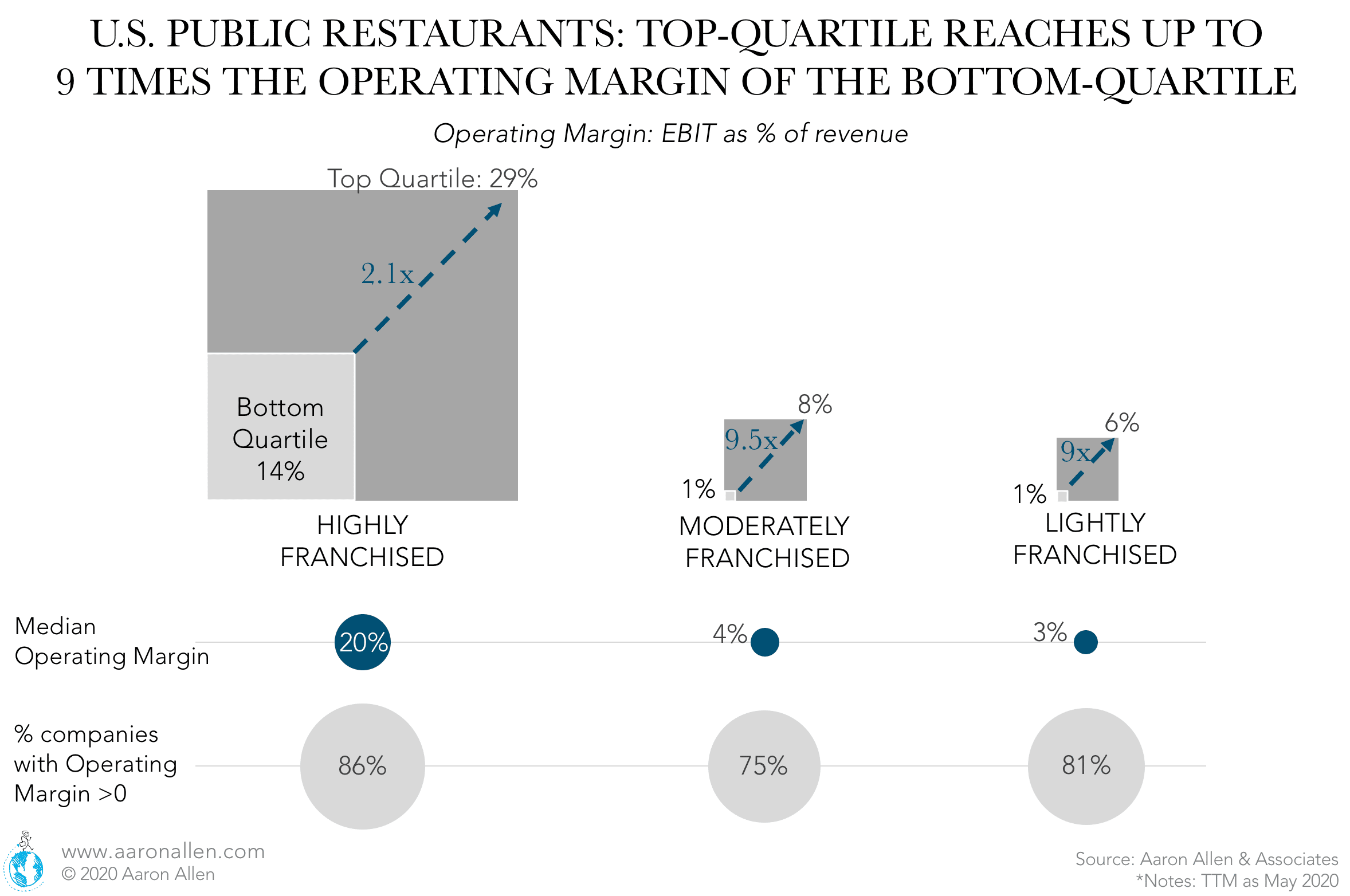

There are many proof-points to demonstrate the differences in approach of top-quartile and bottom-quartile performers. When we look at Operating Margins, the differences are staggering. In moderately and lightly franchised publicly traded restaurants in the U.S., the top-quartile Operating Margin is 9x the margin for the bottom-quartile. For highly franchised restaurants, the top-quartile makes twice the profit margin of the bottom-quartile.

The top performers are also putting more toward R&D and building proprietary systems that are reinforcing the moat around their business and locking out their competition. This is a great time to make operations faster, leaner, and more agile to optimize margins and achieve top-quartile performance.

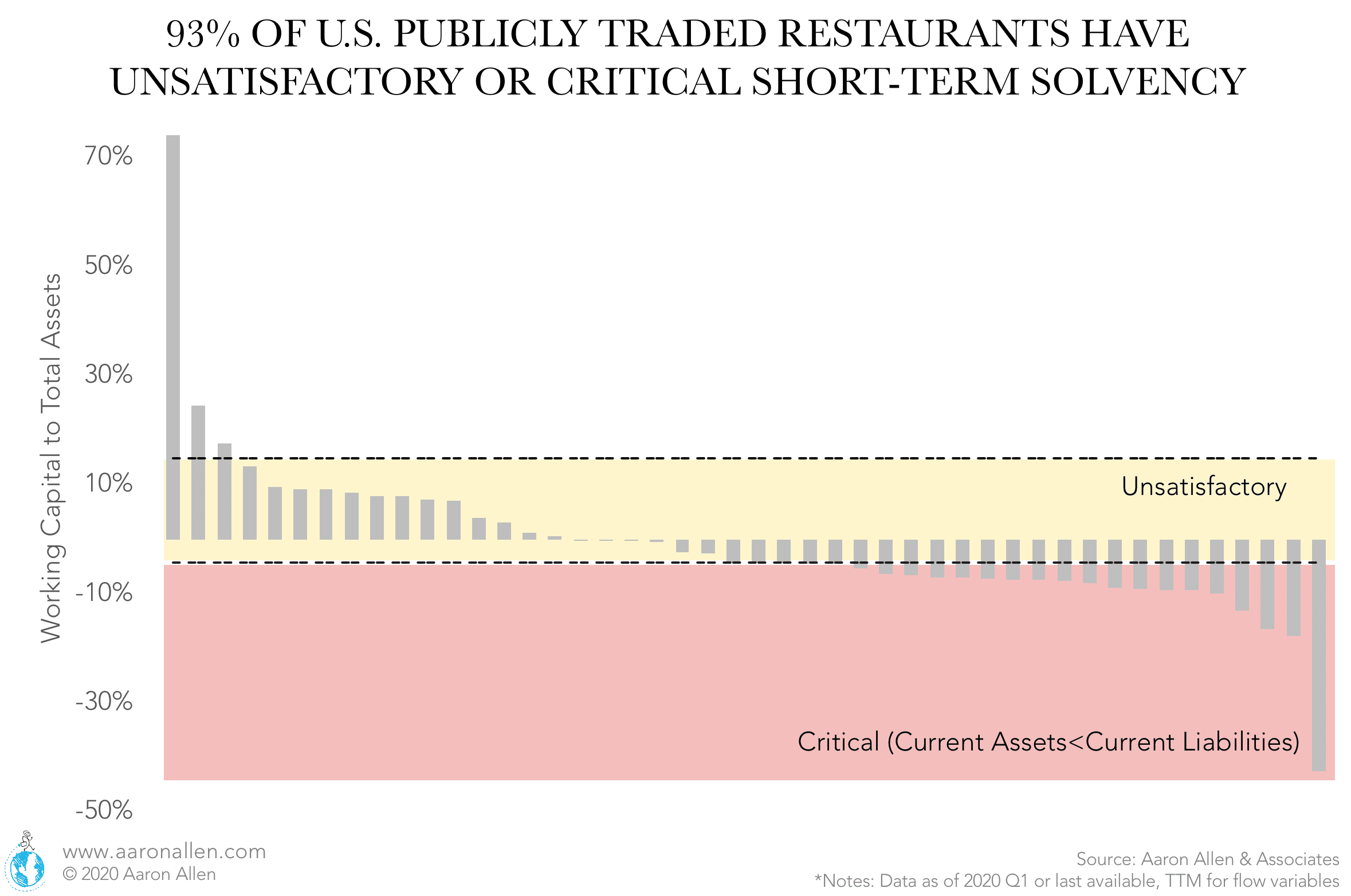

The Working Capital to Total Assets ratio reveals the percentage of remaining liquid assets, once Total Current Liabilities are paid out, compared to the company’s Total Assets. As a rule of thumb, ratios lower than 15% are generally considered unsatisfactory, and negative values are considered critical. 93% of U.S. publicly restaurants are in these zones. For many restaurant chains, investors will have to step in to solve the liquidity crisis ahead of other critical initiatives focused on innovation and re-inventing the economic model.

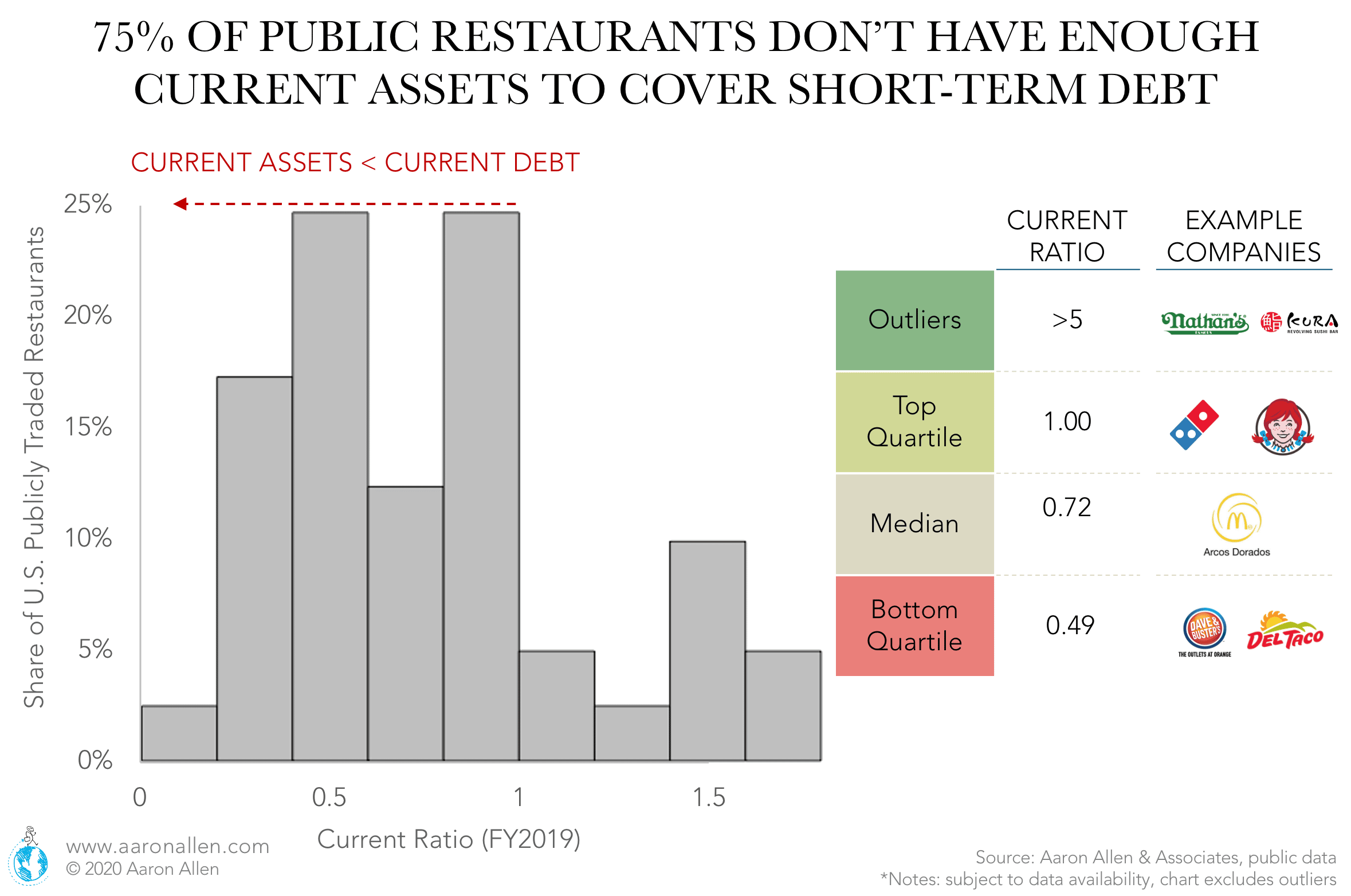

The higher the Current Ratio (Current Assets to Current Liabilities), the more able a company is to pay short-term debt. In the restaurant industry, the current ratio reached a median of 0.72 (FY 2019 for publicly traded companies in the U.S.) and for three-quarters of the industry, the current assets are not enough to cover all short-term debt. Some foodservice companies in the bottom quartile had current ratios lower than 0.50 (current assets covering less than half of current debt).

While liquidity pumping into the economy is buying time, many restaurants won’t be able to sustain their existing debt levels. This scenario will likely lead to plenty of distressed restaurant assets in the near future, which will spur activity as the global pause on M&A lifts as travel restrictions are loosened.

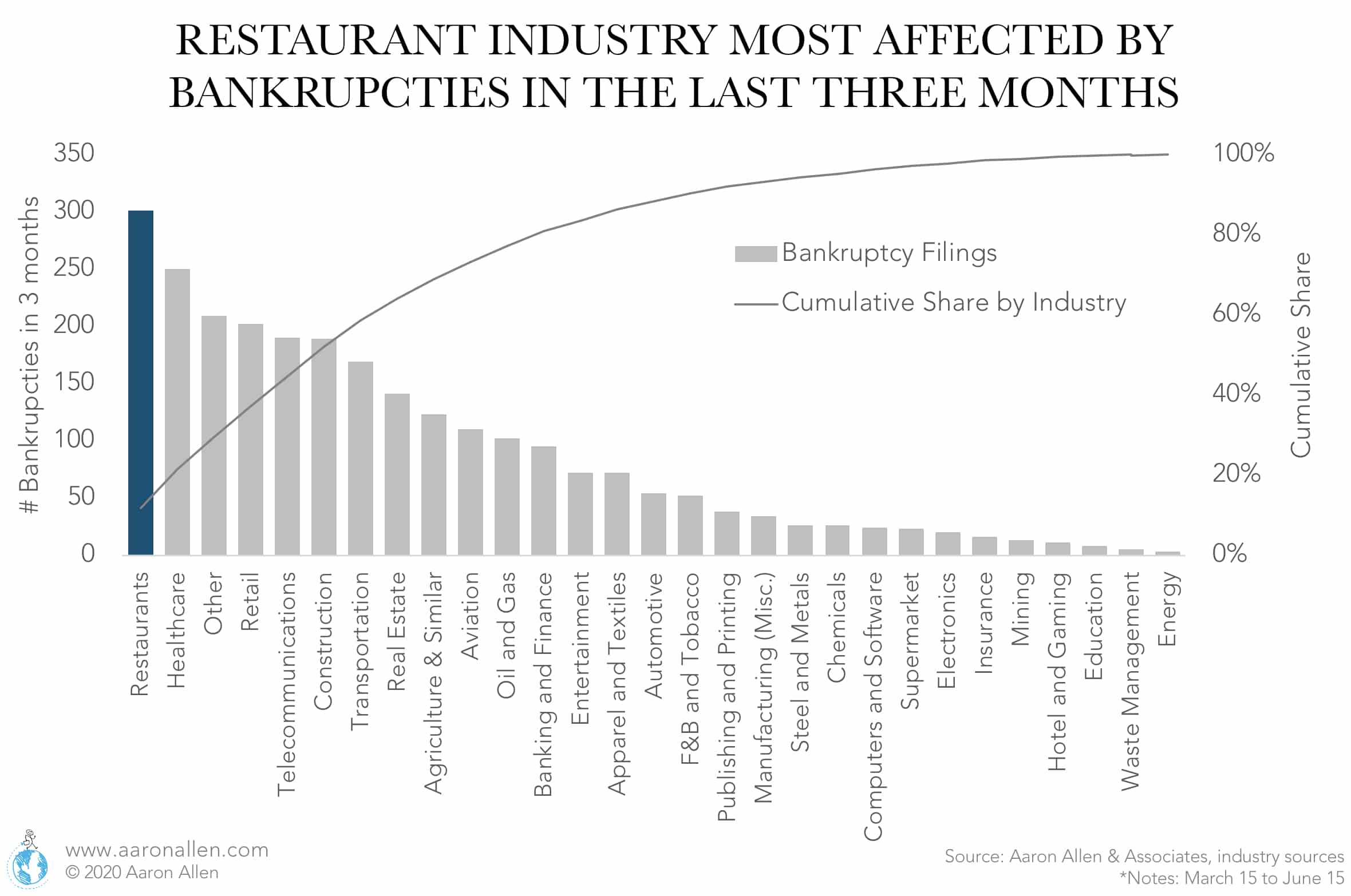

A sobering stat: the restaurant industry has been the sector with the most bankruptcies in the last three months, with 12% of U.S. bankruptcies (more than 300) coming from this industry alone.

More consolidation will happen than in any previous recession. We think 10-15% of restaurants in America will close permanently by the end of the year (with that potentially increasing to 20% if another wave of the virus hits and without further government assistance). The bulk of that will be Casual Dining, full-service restaurants and independents.

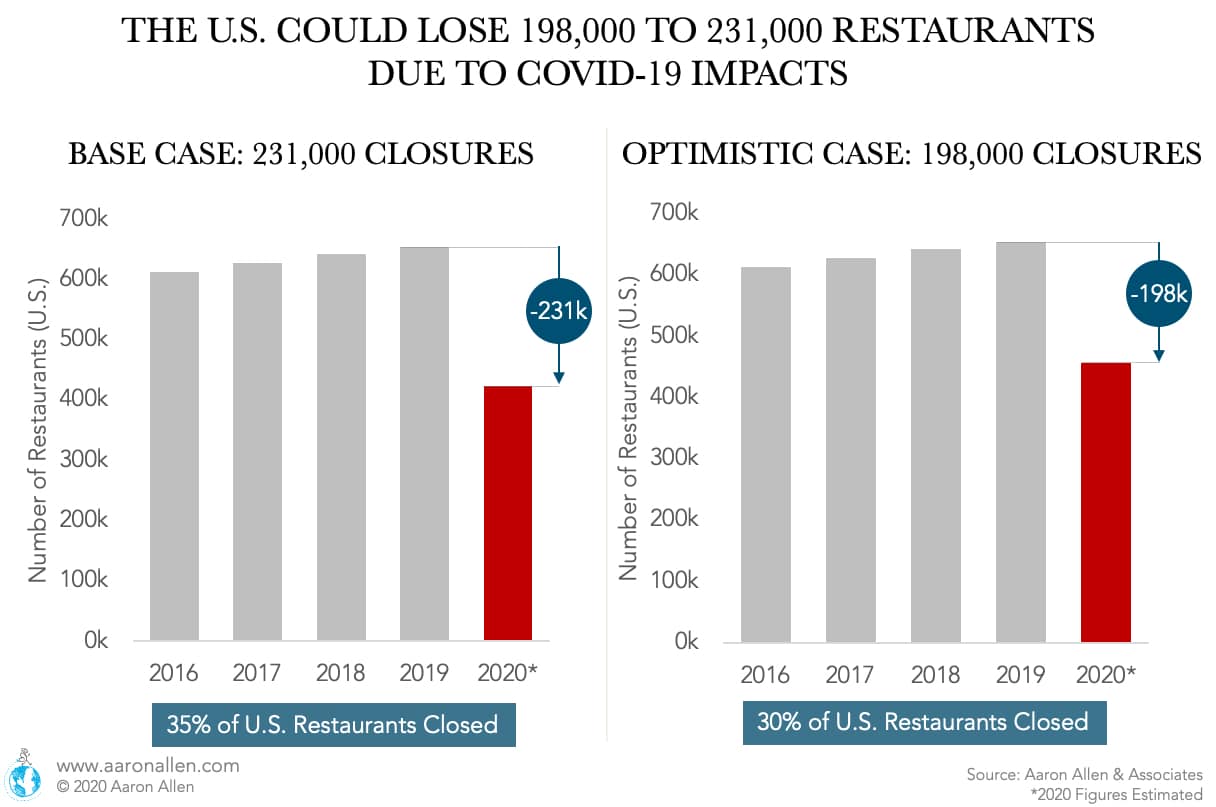

In the U.S., 4.4 million restaurant jobs have been lost (comparing 2019 with the average employment for April–June 2020), and though there are no official figures for closings, we estimate between 198,000–231,000 restaurants will close in 2020. This will be the first year the number of establishments doesn’t climb in at least 20 years (even during the 2008/2009 recession the number of restaurants continued to grow).

Highlights of this analysis were featured in Bloomberg News.