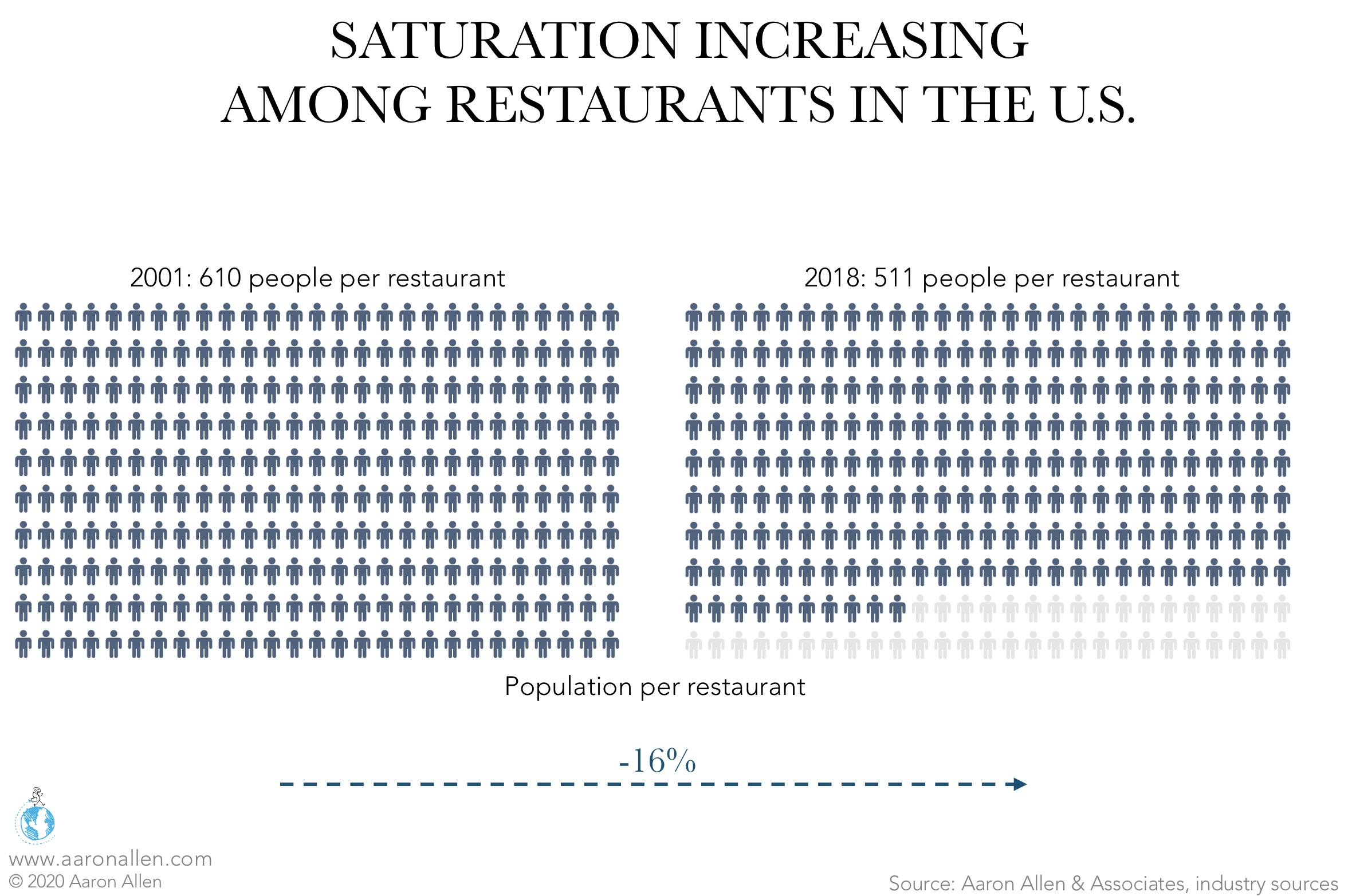

In many mature markets, the industry has reached a point of saturation such that any one company’s growth is coming at the expense of another. The number of restaurants in the U.S. is estimated at 652.8k as of 2019. Saturation has increased in the last years: the number of people per restaurant decreased by 16% from 2001-2018 (or, in other words, the number of establishments grew at rate 150% faster than the population). Saturation signals the onset of consolidation, and many of our clients are looking not just to get better but to get far ahead. Leaders are waking up to the realization that those who are not growing fast are dying slowly. Strong castles are built before the invaders arrive — and fortifying castles for the future means commissioning reinforcements today.

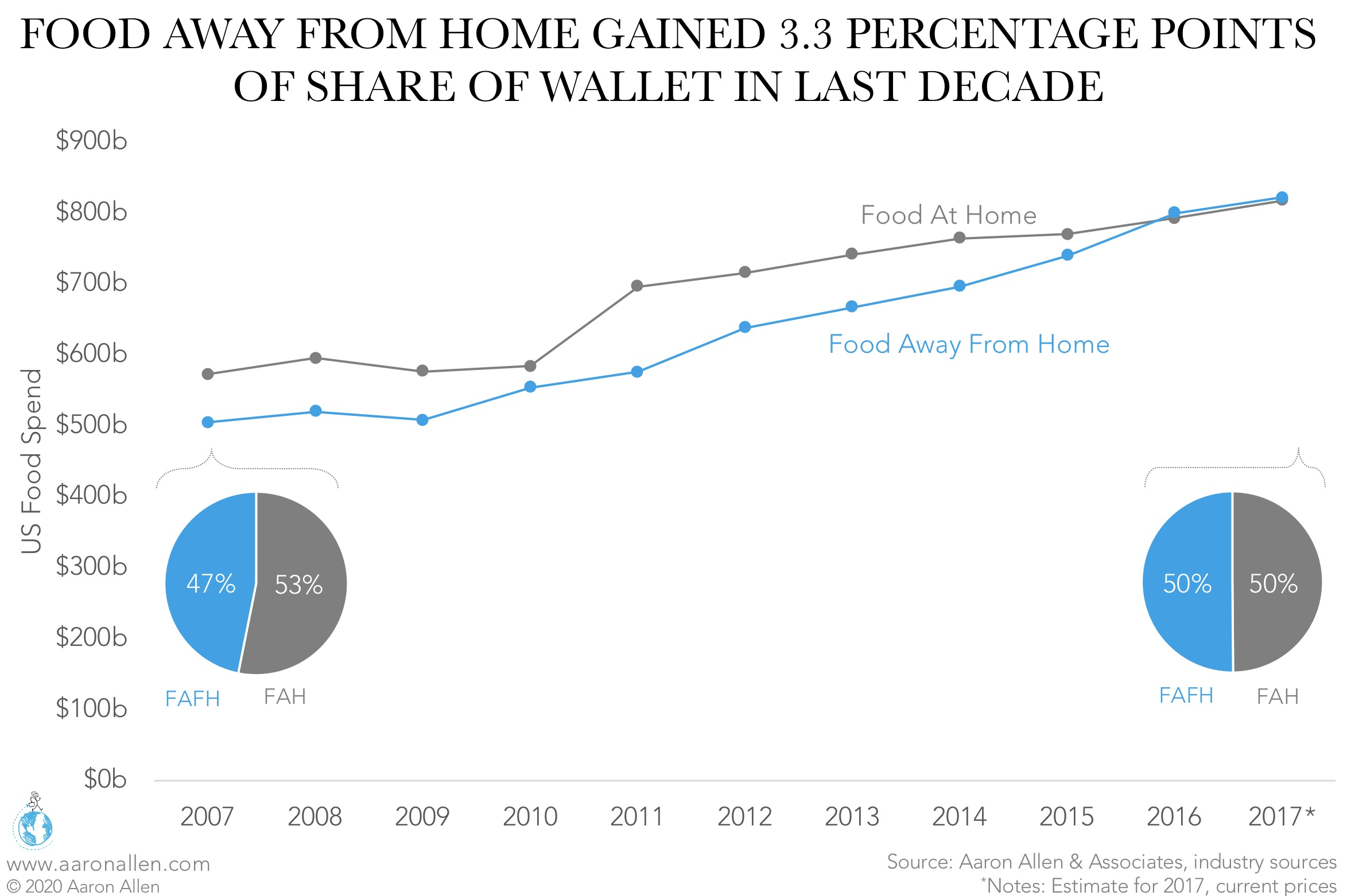

Food spend in the U.S. is estimated to have totaled $1.6t last year. Americans split their budgets almost equally between groceries (Food At Home) and restaurants (Food Away From Home). This was not always the case: the share for Food Away From Home has increased by 3.3 percentage points in the decade since 2007, gaining about $53.6m in business from Food At Home.

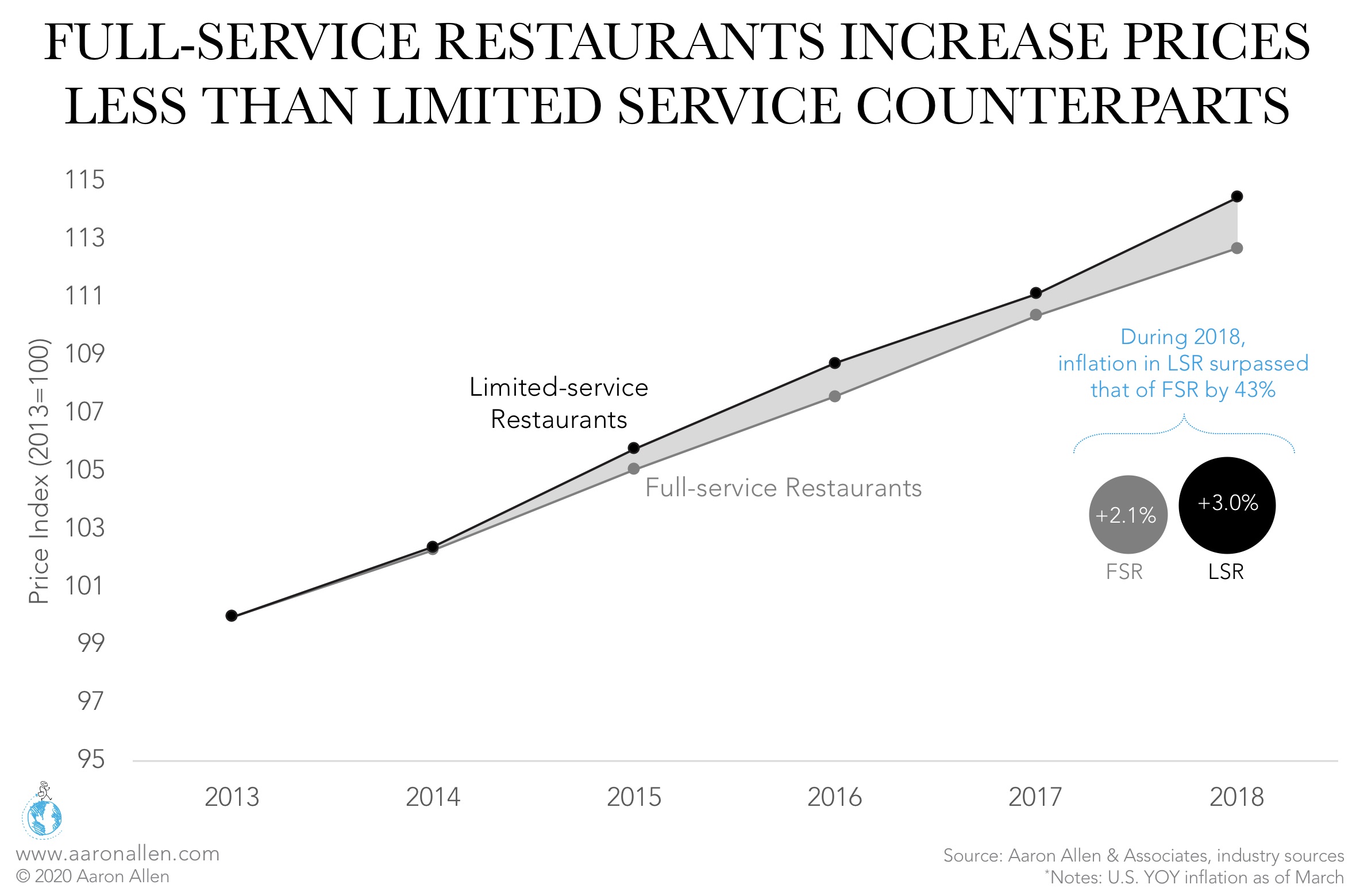

With consumers favoring faster foodservice options, full-service restaurants have been wary to raise prices — in fact, many of the major chains, especially in casual dining, have been offering deep discounts over the last few years. In four of the last five years, inflation for limited-service restaurants has been higher than that of full-service restaurants, and, in the past year (as of March 2018), inflation in LSRs surpassed that of FSRs by 43%.

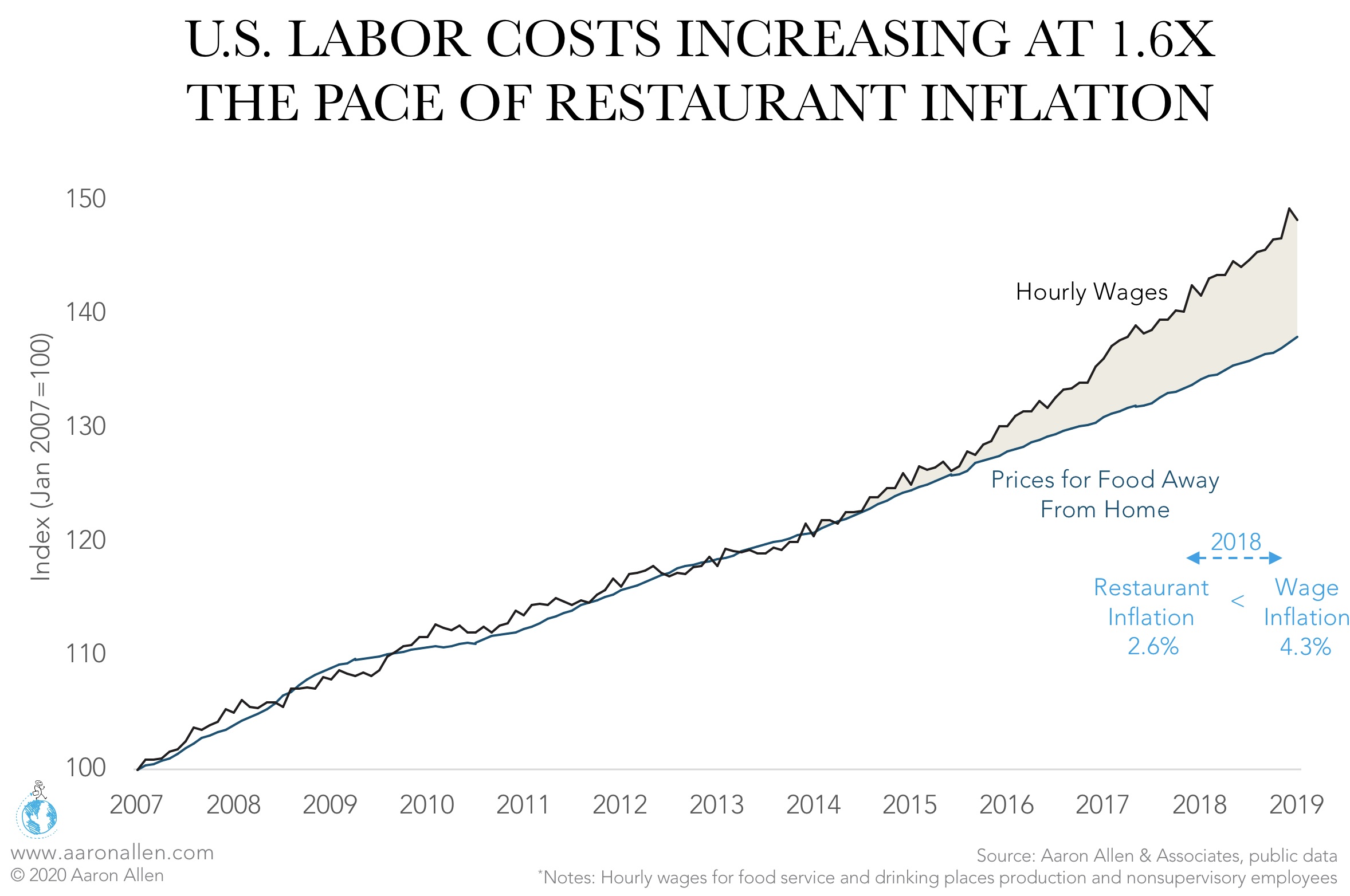

In many markets, labor costs are increasing faster than restaurants are able to increase prices. While hourly wages reached average inflation of 4.3% during 2018 in the U.S., restaurant inflation was 2.6%. Many restaurant groups have been unable to grow same-store sales at a pace faster than inflation. Sagging sales and falling thin margins urges investment in new tools and fresh thinking —but for many it feels like a bold decision that is riskier than kicking the can to next quarter or budget meeting; waiting for the board to push the agenda versus building the case for leapfrog investments. Waiting may hurt less, but it costs a lot more in the long run.

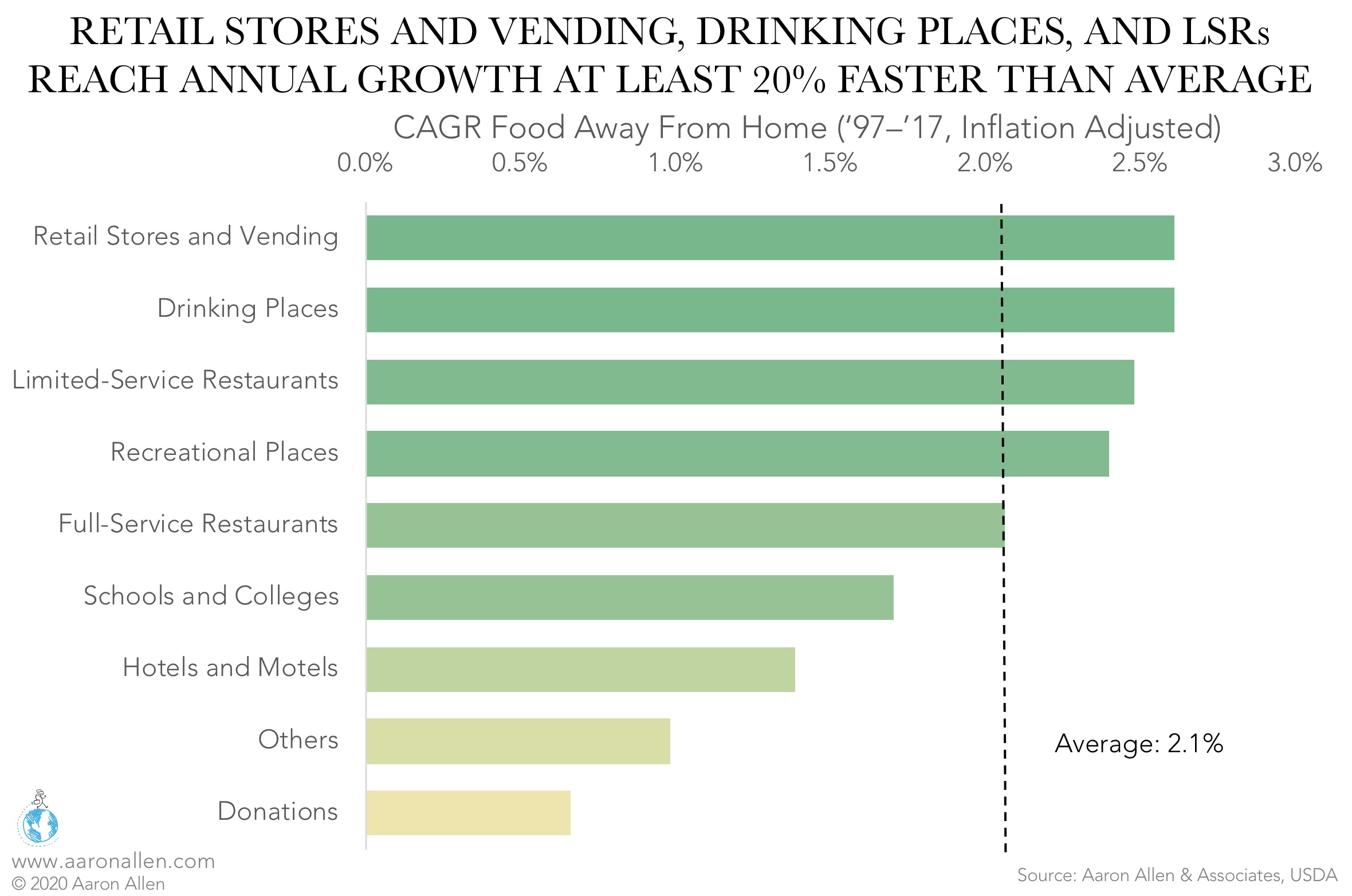

In the last 20 years, the U.S. restaurant industry has grown at a 2.1% CAGR (after accounting for inflation). Some segments, including retail stores and vending, drinking places, and limited-service (QSR and fast-casual restaurants), are growing at least 20% faster than average each year. Meanwhile, other segments, like full-service (casual dining and fine dining restaurants) schools and colleges as well as hotels and motels, are struggling to keep up. Quantifying the opportunity in a specific category allows for targeted expansion strategies and lower risk.

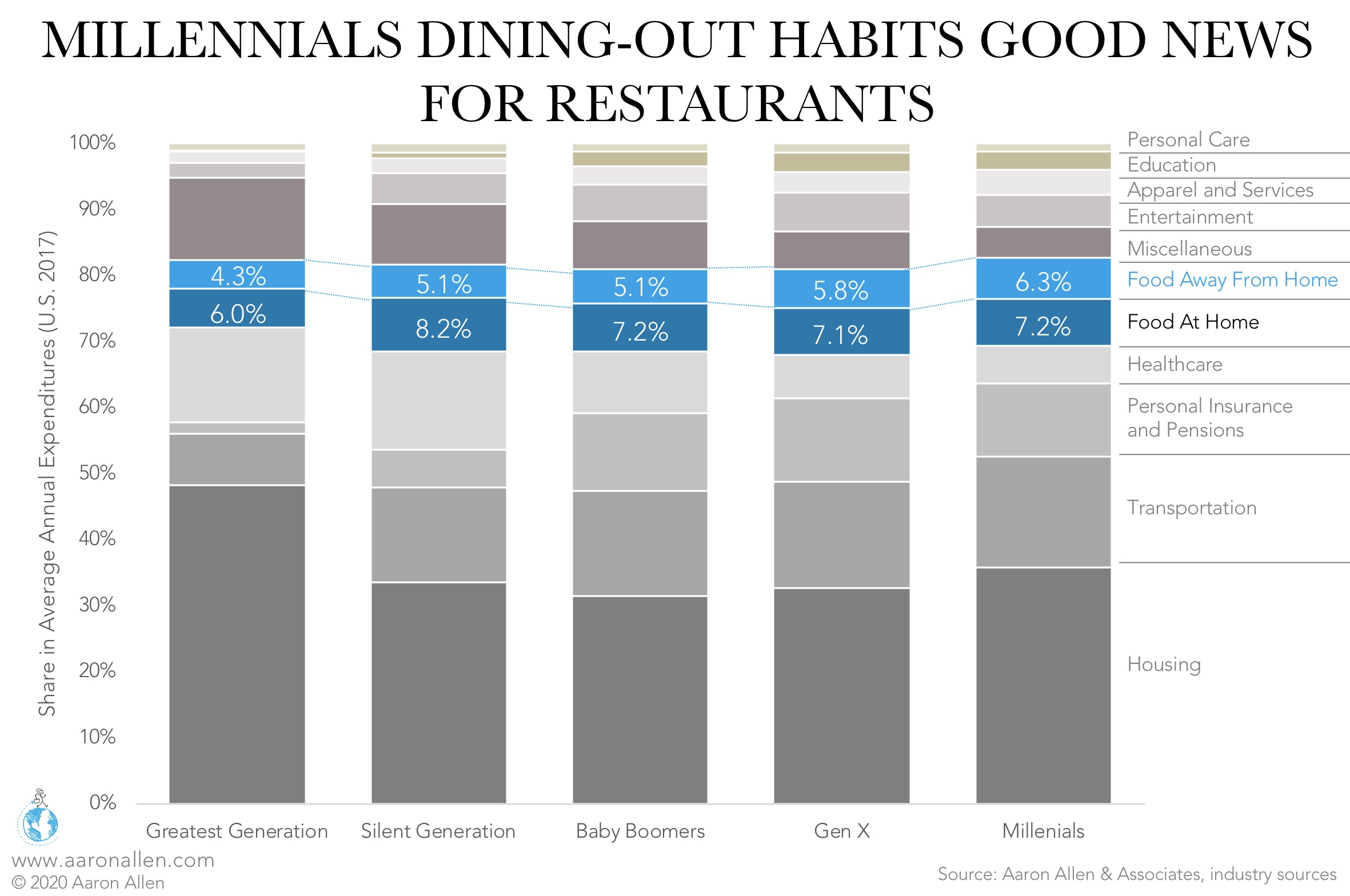

“Millennials” are one of the most common buzzwords when discussing restaurant trends. Though Millennials make less than both Gen X (who earn 41% higher wages) and Baby Boomers (23% higher wages), this young groups devotes a larger percentage of their expenses to dining out than any other generation (6.3% of annual expenditures). In fact, they spend more on food overall, likely a result of their generational preference for healthy diets. As this cohort ages and sees increases in discretionary income, they will continue to have a profound effect on the foodservice industry.

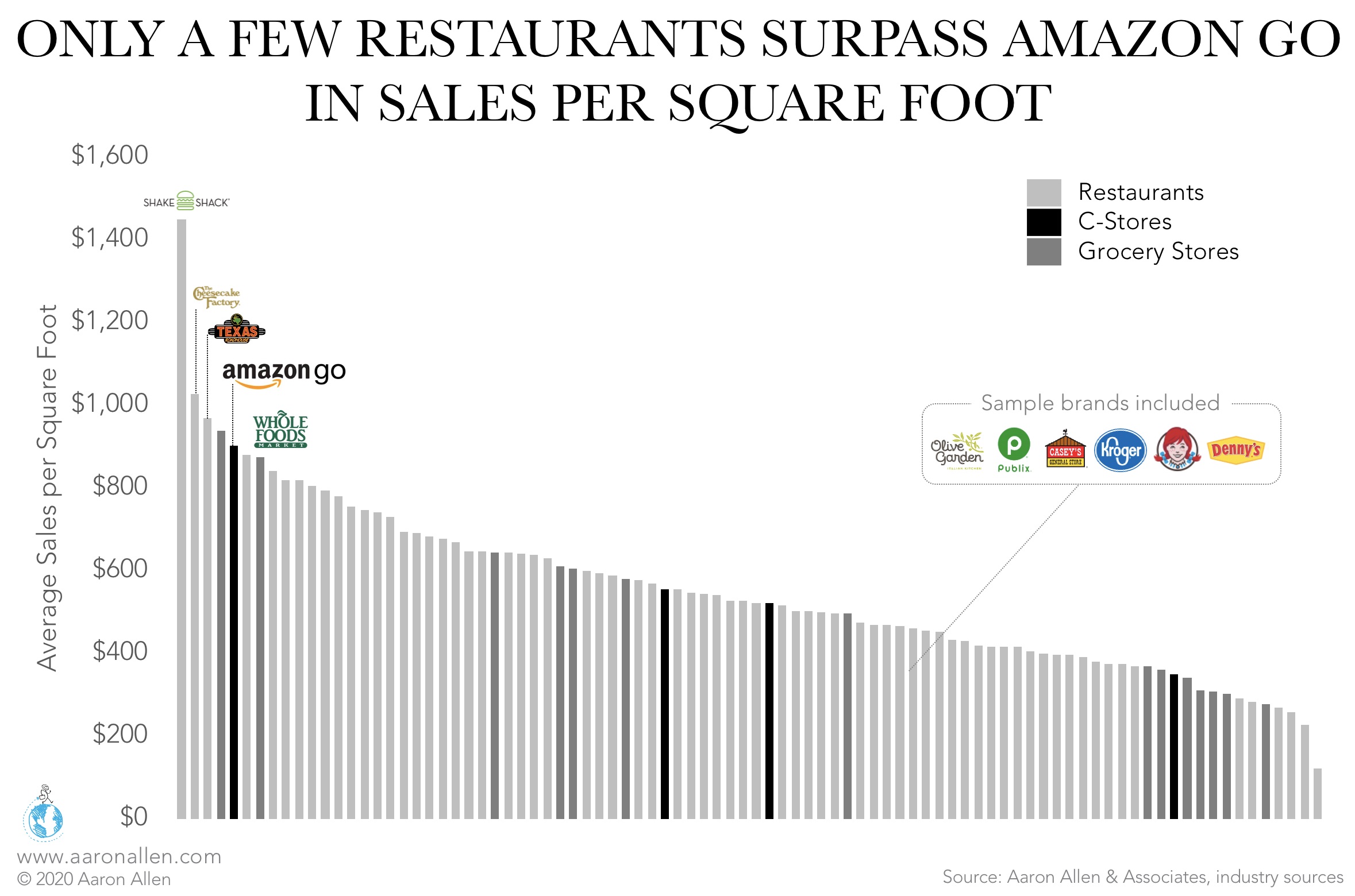

Amazon is converging several weapons it has built or acquired into something more deadly than any one component (Amazon Go, Amazon Restaurants, Amazon Basics, Amazon Fresh, Prime Now, one-click ordering, voice ordering, Whole Foods) is, independently. And though the unit models for grocery stores or C-stores are different than those for restaurants — though we see these categories as competitors for share of stomach and wallet of the same consumer; only a handful of restaurant chains surpass Amazon Go and Whole Foods in sales per square foot.

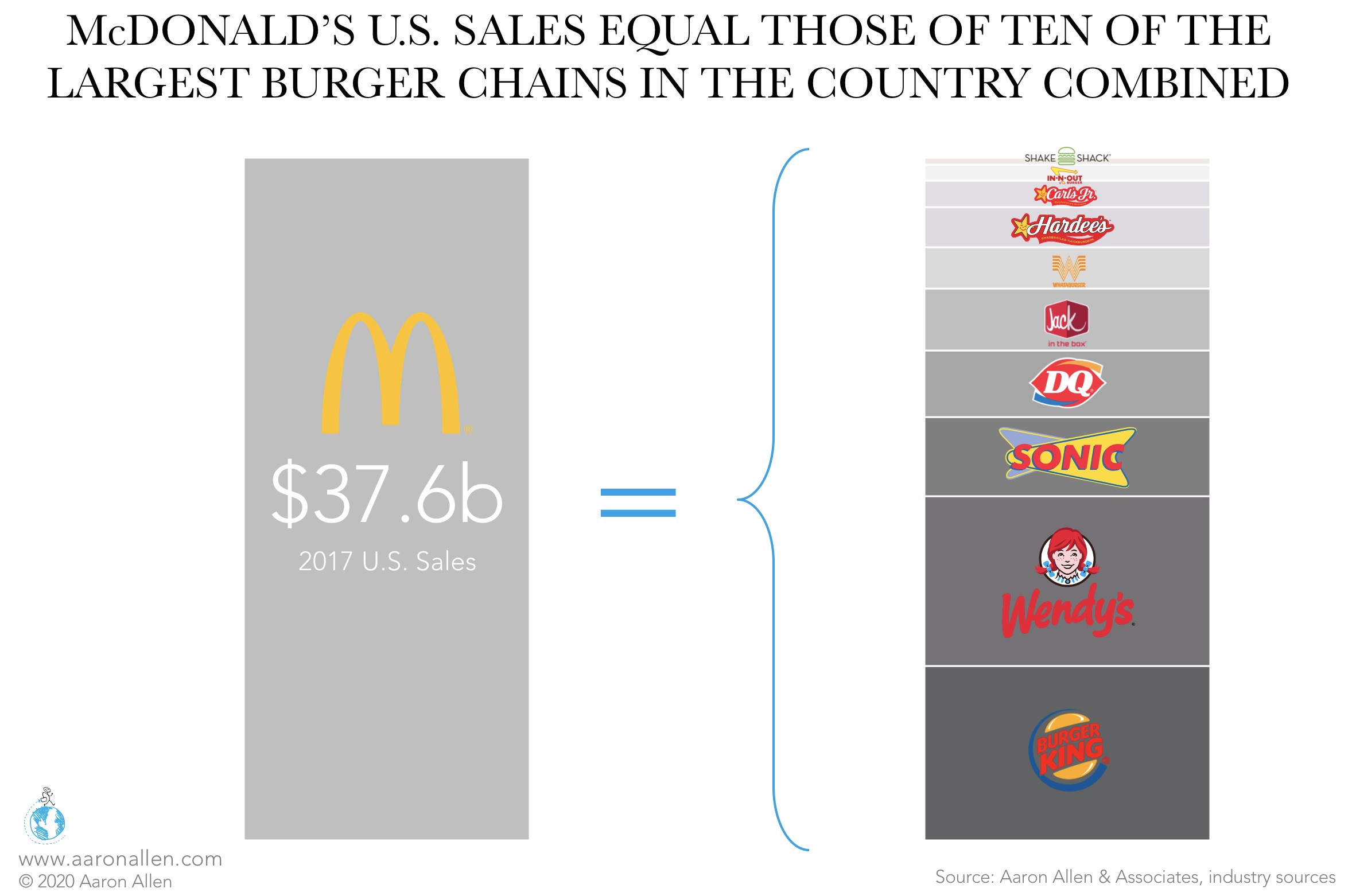

In 2017, McDonald’s sales in the U.S. reached $37.6b, amounting to about 5.5% of what Americans spend in restaurants. The leader in the burger segment has sales equal to those of ten of the largest chains combined. Burger King and Wendy’s (the second and third largest burger chains) only claim half of McDonald’s sales.

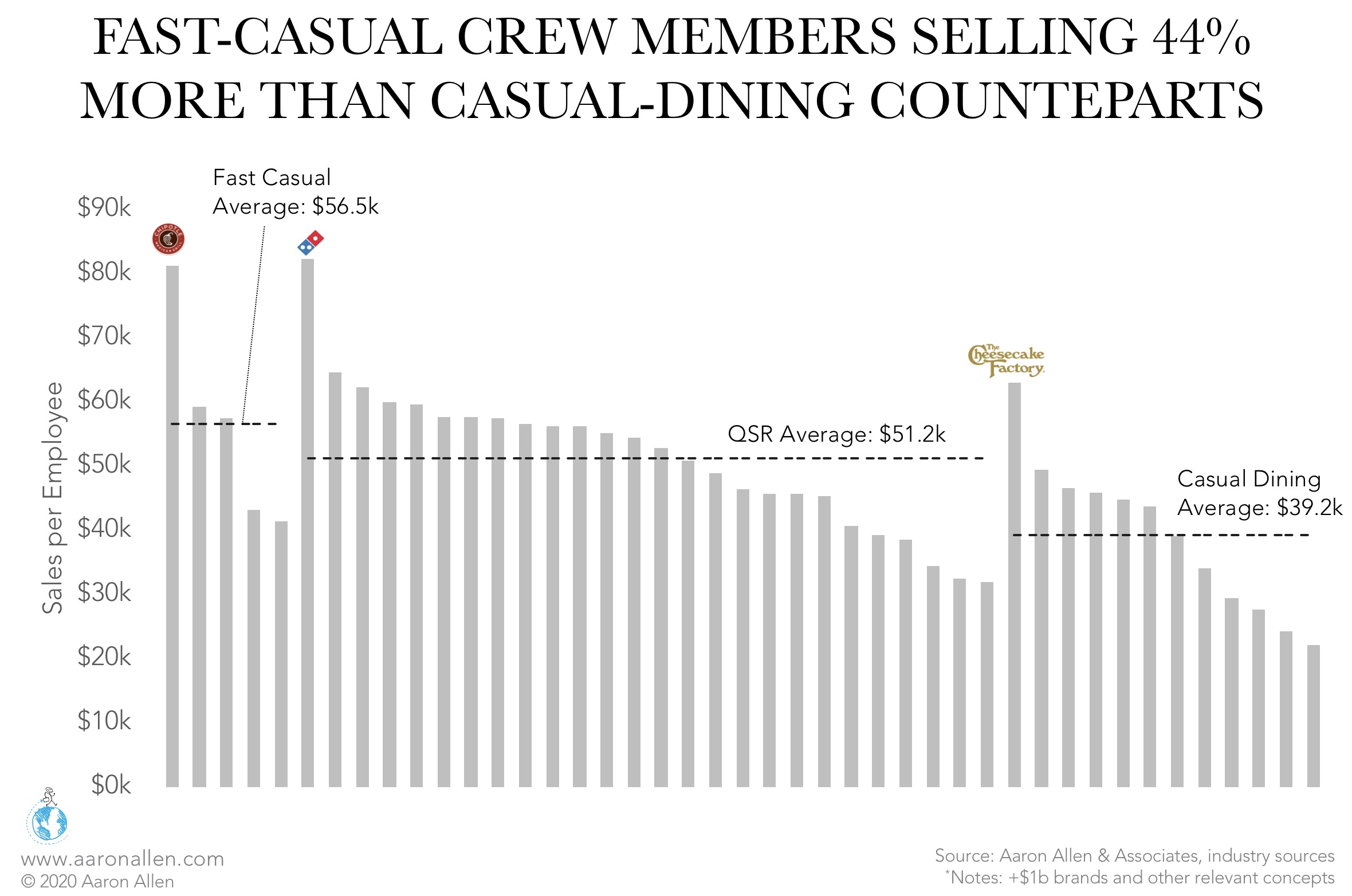

Fast-casual chains average 44% higher sales per employee ($56.5k per year) than their casual-dining peers ($39.2k per year). QSR chains are also more productive than the typical CDR operation, claiming 31% higher sales per employee. The swing within categories is large as well: the most productive fast-casual system makes twice the sales per employee as the least productive. That ratio is even higher for QSR (2.6x) and casual dining (2.8x). Performance optimization can help restaurant operators find gaps so that their systems compete with the most productive brands.

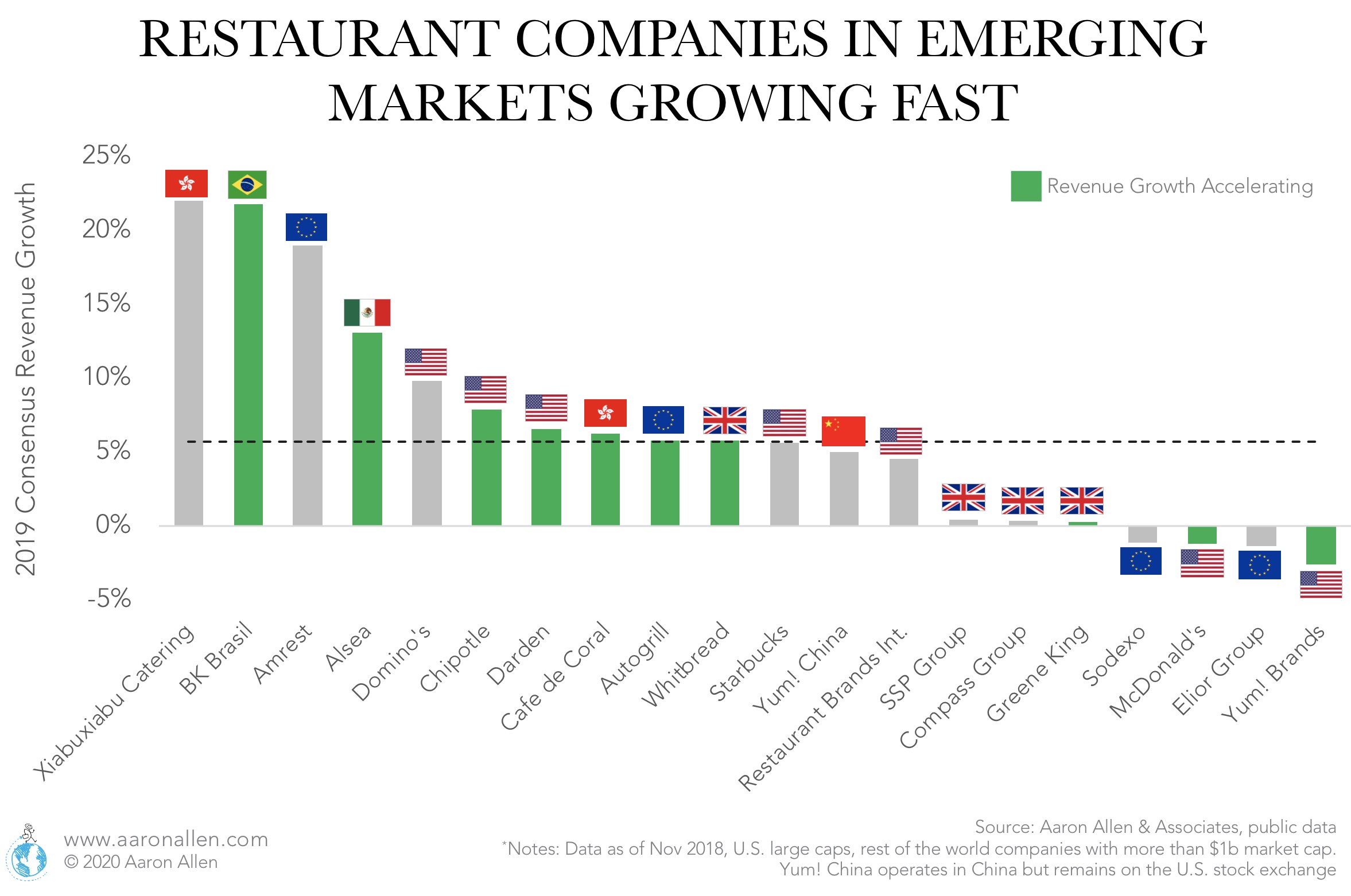

Consensus forecasts for twenty of the largest publicly traded foodservice companies around the world favor emerging markets. In this group, three of the five fastest growers (based on revenue) are in emerging markets: Xiabuxiabu Catering (a QSR hot pot chain), BK Brasil (Burger King franchisee), and Alsea (multi-concept operator of brands including Domino’s Pizza, Burger King, California Pizza Kitchen, Chili’s Grill & Bar, PF Chang’s China Bistro, and Starbucks). It’s worth noting that revenue growth may differ from sales depending on the organization’s franchise level, and some of the weakest growers, like McDonald’s and Yum! Brands, have recently undertaken re-franchising initiatives.

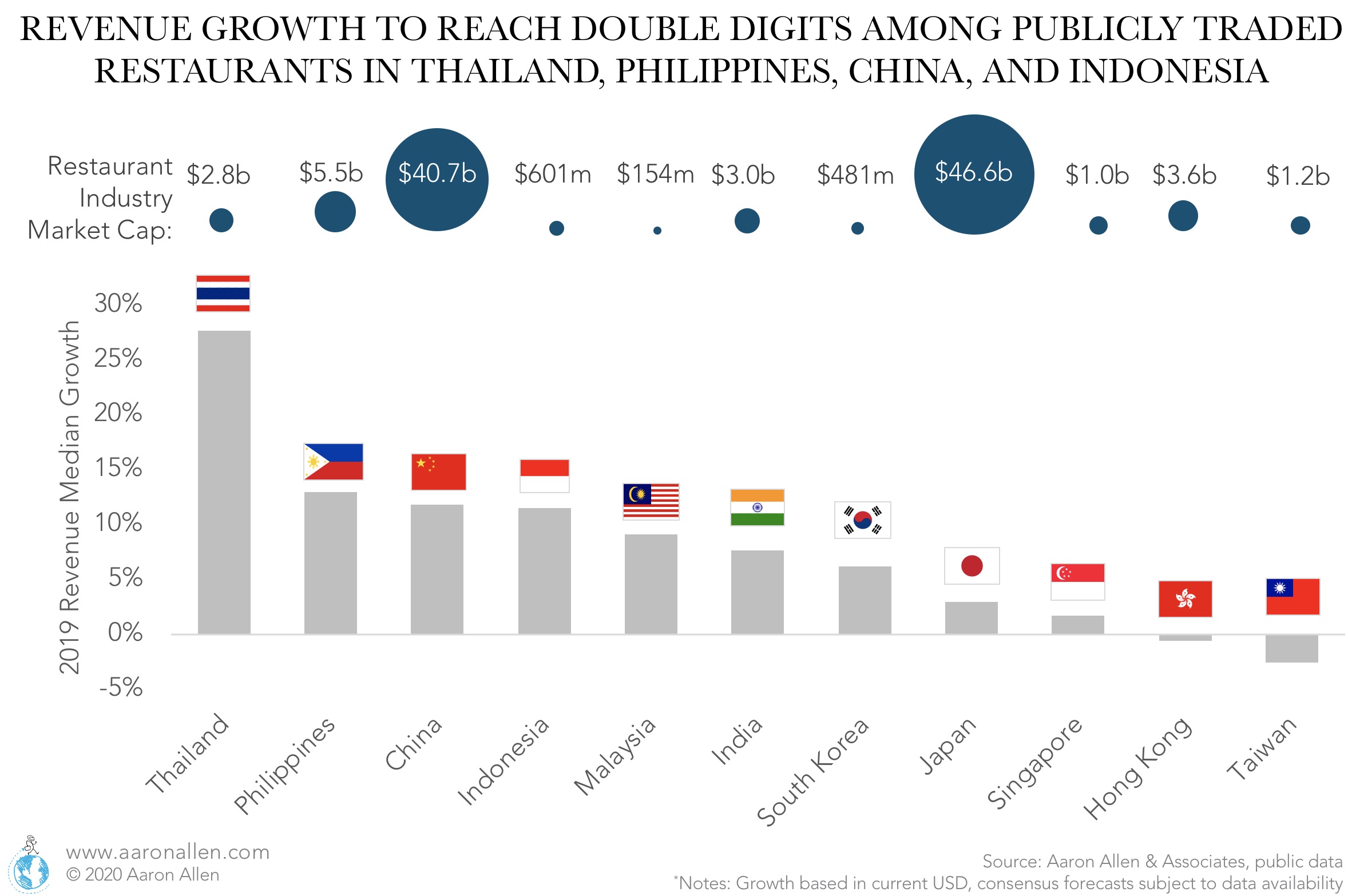

Publicly traded restaurants in some Asian Pacific emerging markets including Thailand, the Philippines, China and Indonesia are expected to reach double-digit growth medians in 2019. China, India, and others in the region have some of the lowest chain restaurant penetration levels in the world. These markets pose an opportunity for foodservice brands willing to invest in strategic plans that will secure a successful cross-border expansion.