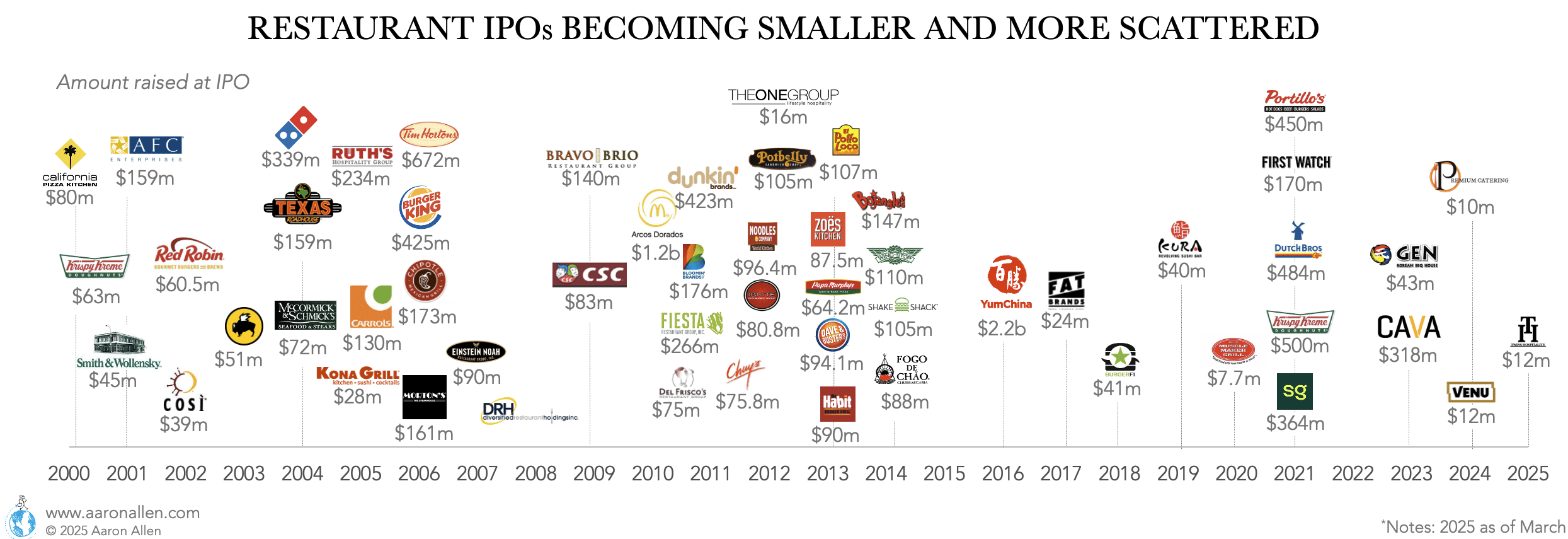

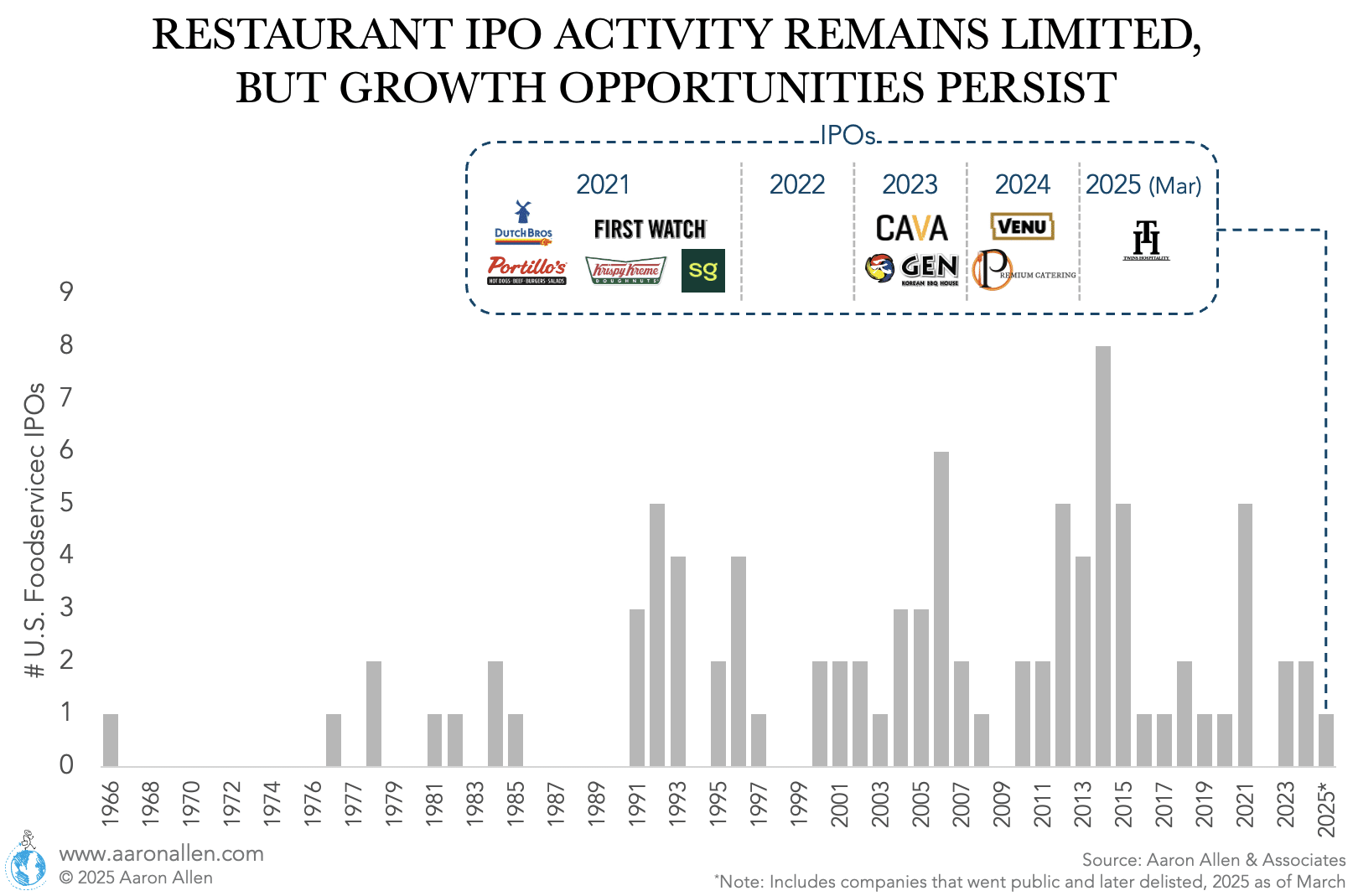

Since the year 2000, we’ve seen several high-profile restaurant initial public offerings (IPOs), from Domino’s to Sweetgreen. Much of it, though, has occurred in spurts. There was a span of nearly two years (2008-2010), for instance, in which only one restaurant made its initial public offering, which can be largely attributed to the recession.

Between 2011 and 2015, though, the tables had turned, with dozens of big names (Dave & Buster’s, Potbelly’s, Bojangle’s, etc.) cropping up on stock exchanges in what some analysts dubbed “the restaurant IPO craze.”

There wasn’t a significant restaurant IPO between 2016–2018. IPOs, in general, saw a downtick in 2016, so the fact that no restaurant chains went public was hardly surprising (106 companies went public on U.S. exchanges in 2016, down from 164 in 2015). But that doesn’t mean 2016-2017 was a bad span for capital markets. On the contrary, we’ve seen plenty of activity on the Private Equity side, with angel investors, PE funds, and seed capital making their way into restaurant chains large and small.

There was a new flurry of restaurant chains going public in 2021, including unicorn Sweetgreen and Portillo’s, First Watch, Dutch Bros, and Krispy Kreme. And though 2022 was a quiet year, CAVA and Gen Restaurant Group went public in June 2023 (raising more than $300 million and $40 million, respectively).

The foodservice industry continues to evolve, showcasing resilience and adaptability in the face of changing economic landscapes. Restaurant IPOs over the past two decades reflect the sector’s dynamic nature, with emerging brands carving their place in a competitive market. While some of the most recent IPOs (2023-2025) raise smaller amounts, this trend underscores the opportunities for niche concepts and innovative dining experiences to access capital markets.

RESTAURANT IPO STATISTICS

- Since 2002 there has been at least 1 restaurant initial public offering every year except for 2009 and 2022.

- 2021 was the best year for Restaurant IPOs since 2015 and classifies as one of the second-best years along with 2015 and 1992, each with 5 IPOs.

- Five companies went public in 2021: drive-thru coffee chain Dutch Bros, casual dining First Watch, Krispy Kreme, QSR hot-dogs chain Portillos, and fast-casual salad focused Sweetgreen.

- 2014 was the year with most restaurant IPOs with 8 stocks going public including Dave and Buster’s, Del Taco, El Pollo Loco, One Group, Papa Murphy’s, Restaurant Brands International, Habit, and Zoe’s Kitchen.

- Except for years without restaurants’ initial public offerings, there are many with only one foodservice IPO: 1966, 1976, 1978, 1981, 1982, 1985, 1997, 2002, 2003, 2007, 2008, 2010, 2016, 2017, 2019, 2020.

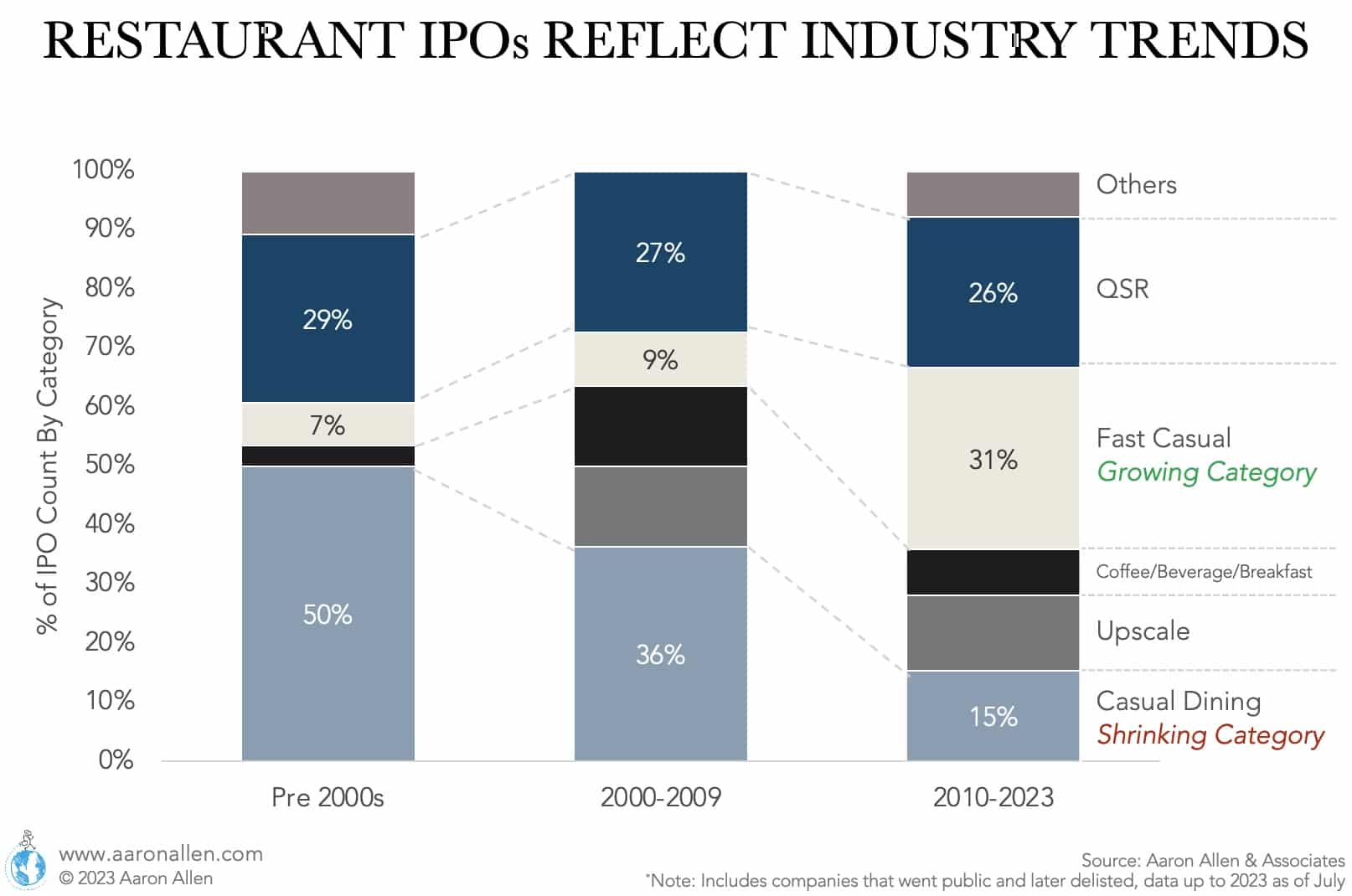

- IPOs reflect economic and sector trends, and the foodservice industry is no exception. Over time, we can spot the evolution of restaurant categories: before the 2000s (our records start in the mid-60s), half of the IPOs were in the casual dining category. Between 2000-2009 the share went down to about a third, and after 2010 only 15% of IPOs were casual dining restaurants (but there was a number of upscale chains going public such as Del Frisco’s and The ONE Group).

- On the other hand, the number of fast-casual chains going public increased to 31% of IPOs — reflecting the premiumization of limited-service.

FOODSERVICE MARKET CAPITALIZATION

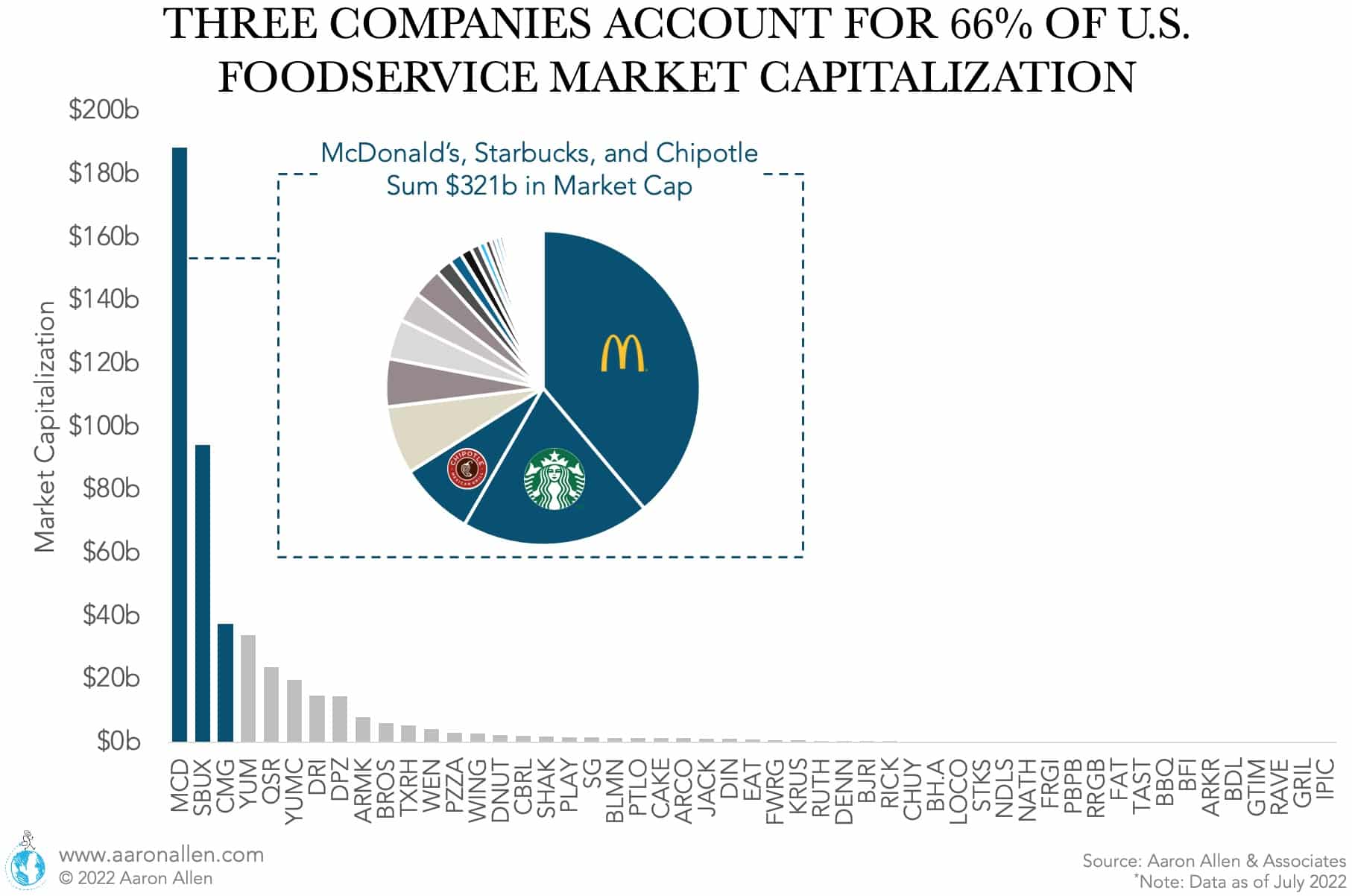

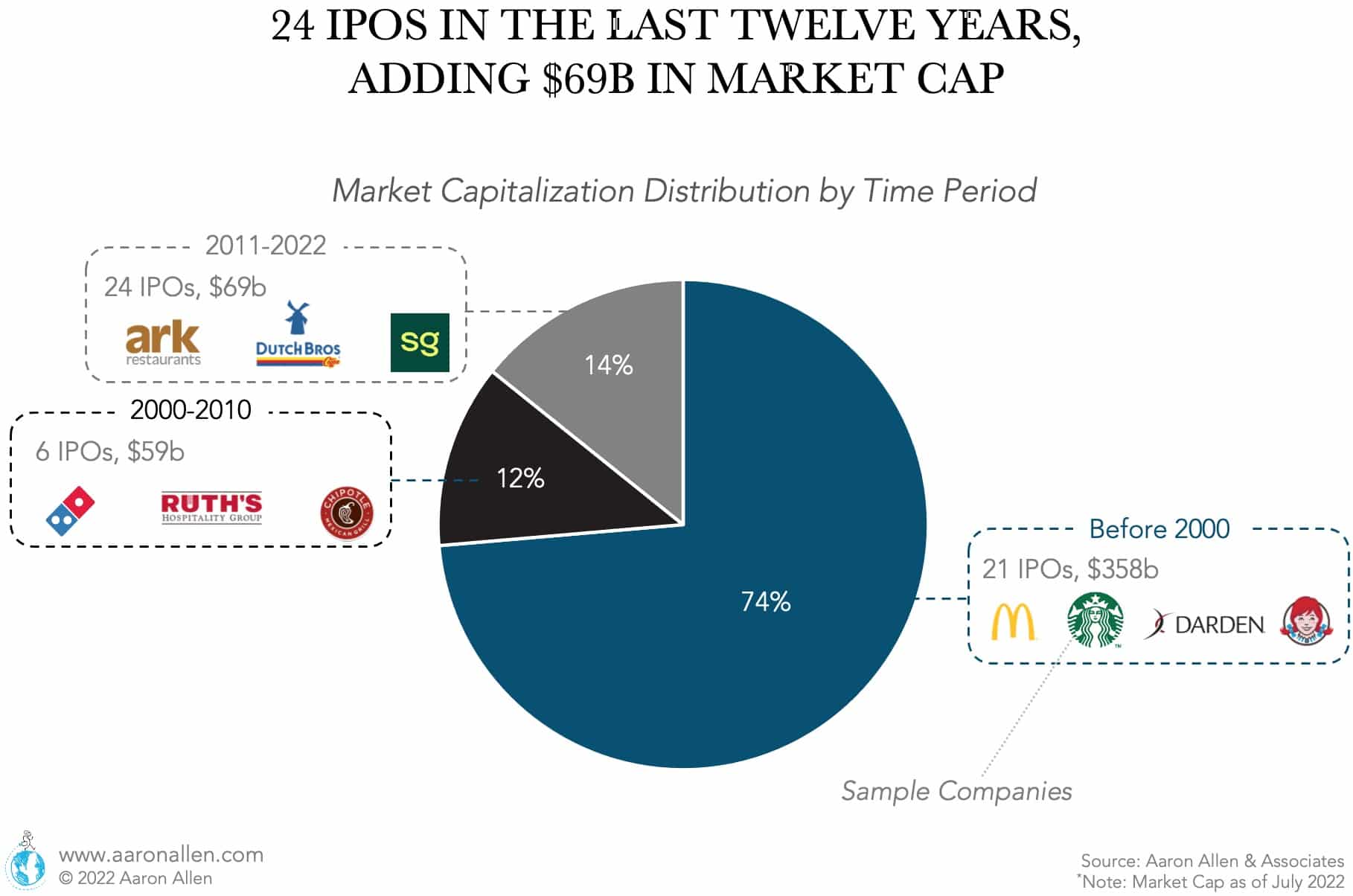

- The total market capitalization of foodservice stocks in the U.S. as of July 2022 is $485.5 billion (51 stocks between NASDAQ and NYSE, excluding over-the-counter stocks).

- There is a high level of concentration with the largest three restaurant chains McDonalds, Starbucks, and Chipotle accounting for 66% of foodservice market capitalization.

- The current market capitalization of McDonald’s (IPO 1978) is the largest in the history of the industry. So much so that it makes the initial public offerings of years 2017-2020 almost insignificant.

- The further in the past an IPO, the larger today’s market capitalization.

- Restaurant companies whose initial public offering was before 2000 have a much larger market capitalization than the other periods. Even though this is largely driven by McDonald’s (1978) and Starbucks (1992), the percentage of market cap by timeframe doesn’t change much if we exclude these two giants.

- It must be noted that the pre-2000 period is composed of IPOs since 1966 (34 years) while the following two are roughly decade periods.

- There were 37 foodservice companies’ IPOs in the last decade (2011-2023), which surpasses the number of public companies currently in the market that went public before the 2000s.

- Between 2000 and 2010 there were a IPOs (24). Similarly, between 2011 and 2023 there have been 26 IPOs.

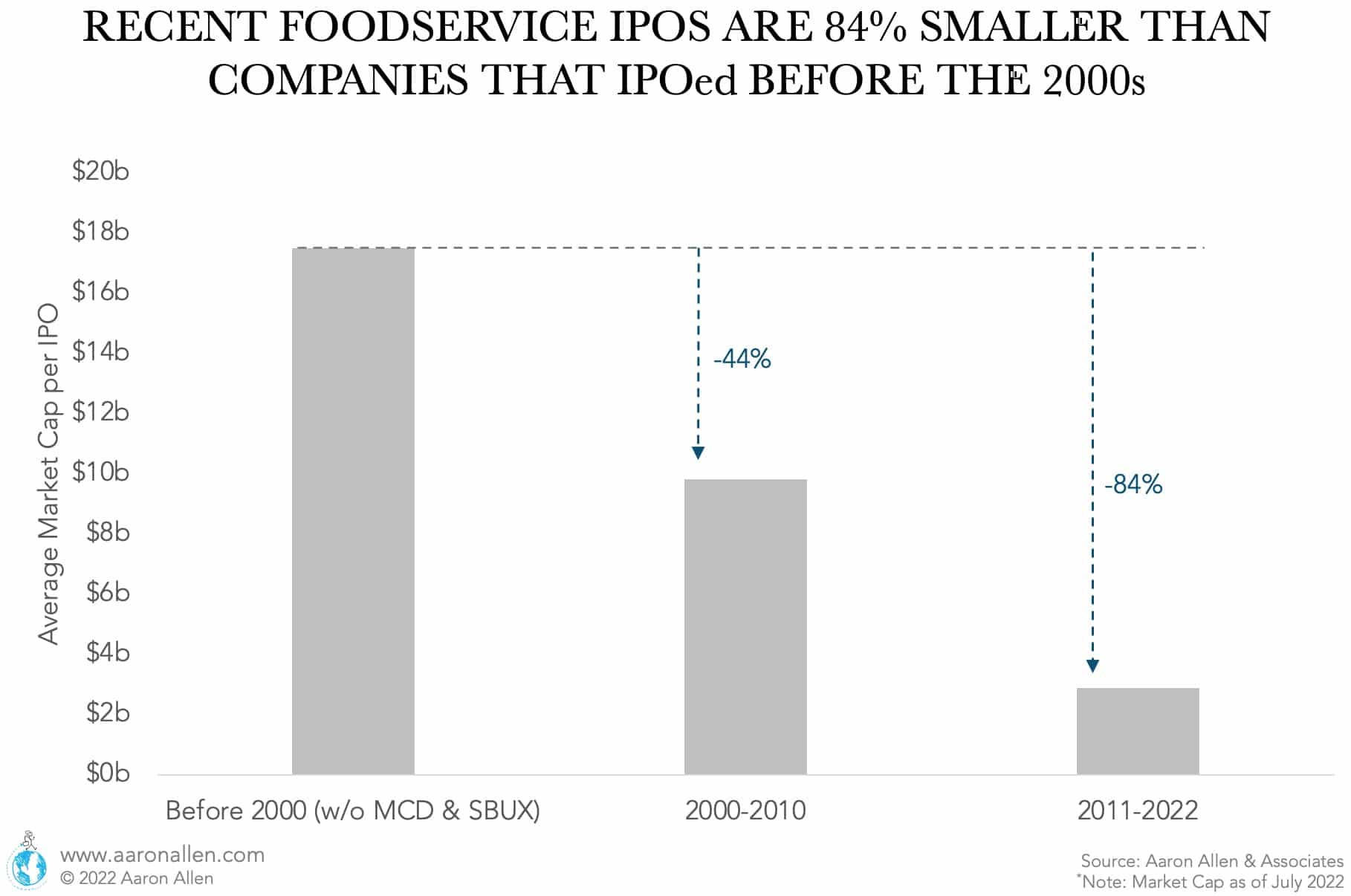

- The recent foodservice IPOs are significantly smaller than established companies that IPOed before the 2000s (even excluding giants like McDonald’s and Starbucks). On average, the market cap of restaurant IPOs in the last decade has been $2.9b while companies that went public before the 2000s have current market caps averaging $17.5b. Part of this difference could be related to the maturity of those that have been public for more than two decades. But it also seems to be indicating smaller IPOs in recent years.

RECENT RESTAURANT IPOs, FOODSERVICE TECH IPOs, AND POTENTIAL FUTURE ACTIVITY

The most recent flurry of restaurant IPOs occurred in 2021, and offered a variety of restaurant industry segments (fast-casual, QSR, casual dining) and menu types (salad, hot-dogs, coffee, breakfast).