A public restaurant company’s current stock price can tell you a lot about its past and current performance, but it doesn’t offer much insight into the future. Chipotle’s investors would have probably loved some warning signs before the food safety scandal that cut the chain’s value in half. Though they aren’t perfect crystal balls, an organization’s earnings per share (EPS) and dividends per share (DPS) say a lot about the executive team’s priorities, helping investors make educated decisions about where to put their money.

Before we get into the numbers, some quick definitions. EPS is calculated by subtracting dividends distributed from net profit and then dividing that figure by the average number of shares outstanding. As result, the lower the number of outstanding shares, the higher EPS — which explains why buybacks can increase EPS.

DPS measures the portion of a restaurant company’s earnings that it distributes to shareholders. While some investors see consistent payouts as a signal of the company’s strong performance, a high DPS might indicate that the firm is not reinvesting capital, possibly due to few positive NPV projects or growth investment opportunities. Companies with expected low growth rates often pay out high DPS rates.

Looking at the difference rates of EPS and DPS, not to mention the ratio between the two figures, tells us quite a bit not only about individual foodservice companies but also about the industry landscape as a whole.

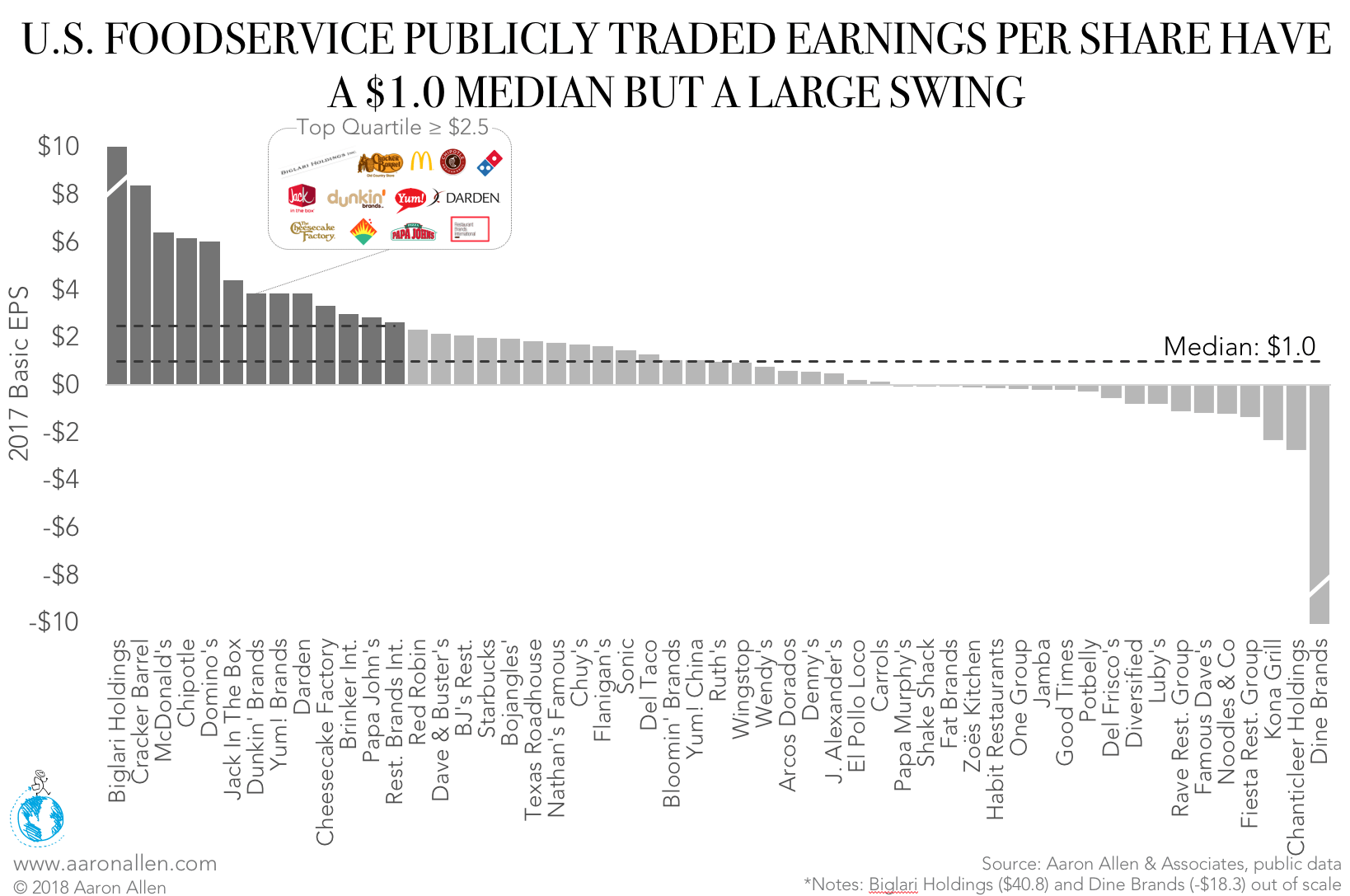

Restaurants Show a Large Swing in EPS

Public restaurant companies in the top quartile have an EPS of at least $2.49, 2.5 times the industry median.

The gap between the highest EPS in the industry and the second highest value is striking. Biglari Holdings had an EPS of $40.80 in 2017, 41 times the industry median. Second-place Cracker Barrel earned $8.40 for each outstanding share of stock outstanding.

Bilgari Holding’s high EPS can be explained by its small number of outstanding shares. As of December 31, 2017, Sardar Biglari held approximately 52.6% of the company’s stocks leaving only 2.1m shares outstanding, the lowest among peer companies. In comparison, Cracker Barrel has 24.3m shares, and McDonald’s allocates its earnings to 807.4m outstanding shares.

On the other side, Dine Brands reported an EPS of -$18.28, attributable to -$330.54m earnings in 2017, with a total revenue of $804.8m. The decline was primarily due to lower revenue from Applebee’s, which cut into the gross profit from franchise operations. An increase in bad debt expenses and growing G&A expenses due to labor-related costs also contributed to the loss.

Interestingly, both Biglari Holdings and Dine Brands are casual-dining restaurants, implying a swing of $59.08 not only in the industry as a whole but specifically within the casual dining segment.

Compared to other industries, foodservice has a moderate swing. Finance & insurance has the highest, at $259.06/share. Many industries, such as healthcare, education services, and oil & energy have a negative median EPS. Foodservice ranks third in median EPS, only surpassed by construction and finance & insurance.

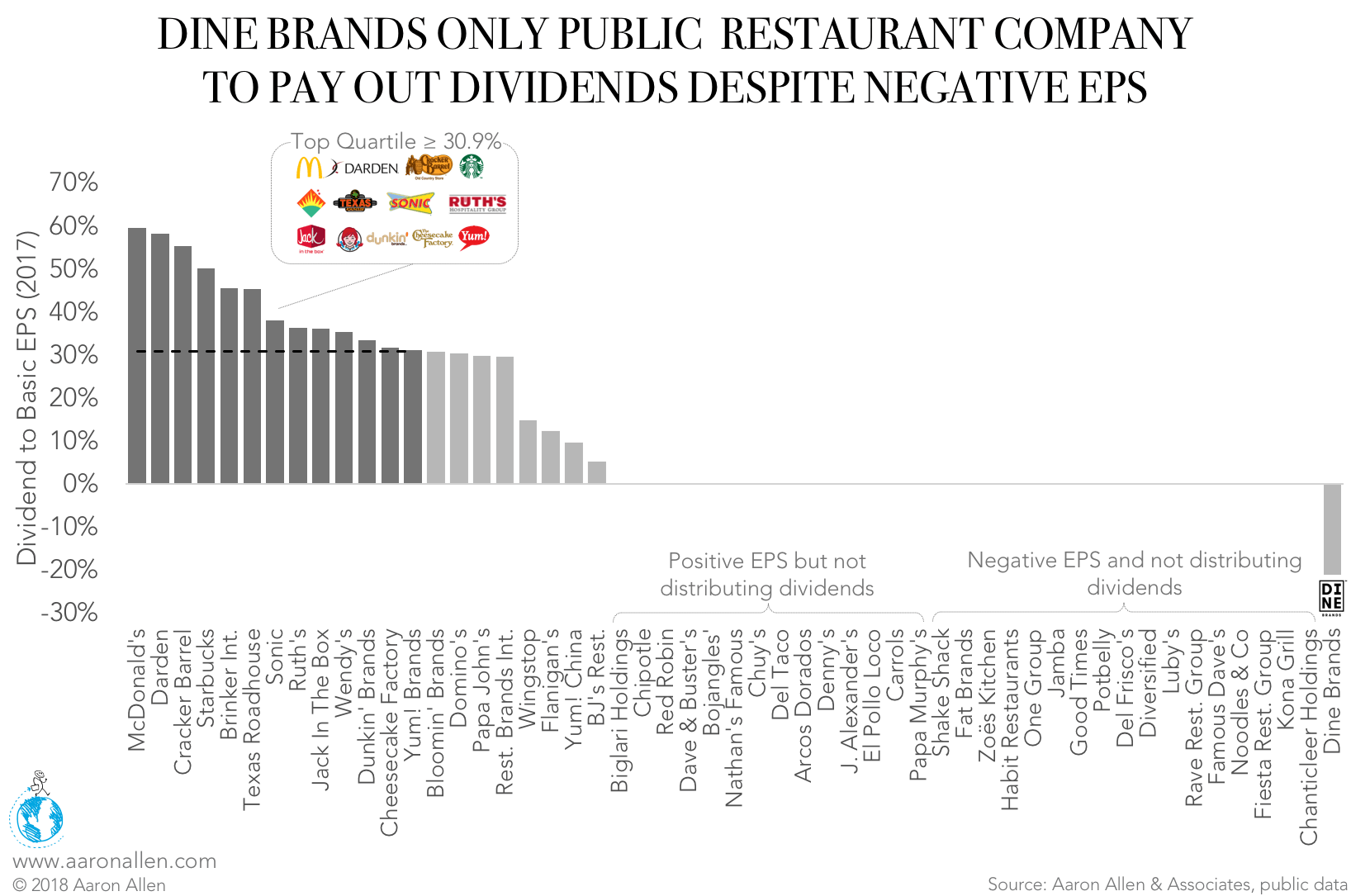

Fast Casuals Not Distributing Dividends

More than half of U.S. publicly traded foodservice companies don’t pay dividends to shareholders. The top quartile for all operations is $0.81 or greater. While the ratio of casual-dining and quick-service companies paying dividends is similar to the distribution across the industry, fast-casual restaurants are under-represented. The share of fast casuals paying dividends is 5%, but this segment accounts for about a fifth of the foodservice companies on the stock exchange. Only 34% of fast casuals have positive EPS, and, of those, only Wingstop paid dividends in 2017.

Likewise, no upscale restaurants appear in this group, likely because their 0% franchise rate means they have more substantial CAPEX requirements than QSR or CDR chains. Most restaurants in this category prioritize reinvestment into new store openings, maintenance, and remodeling.

Foodservice has a low median DPS when compared to other industries. Finance & insurance once again has the highest swing, at $50/share — 10.75 times foodservice’s $4.65 swing. The utilities industry has the highest DPS median ($1.26). This is more evidence that companies with lower growth prospects distribute higher dividends: stocks in utility companies are relatively stable and have fewer opportunities for earnings growth beyond inflation.

Dividend Cuts Can Spook Markets

It’s quite surprising that Dine Brands continued to pay dividends despite a negative EPS, but some organizations maintain their payouts no matter what because markets can react negatively to reduced or eliminated dividends, leading to a drop in the company’s share price.

Even some established chains may prefer to reinvest their earnings rather than issue dividends. These retained earnings are used for CAPEX investments, concept acquisitions, and as a cushion to protect the operation from future losses or extraordinary events.

An executive team’s decisions about whether to distribute or reinvest their earnings will come down to their overall strategy, but operators should consider the signals these decisions are sending to investors. It’s true that regular, high dividends will attract investors, as long the payouts do not compromise long-term growth and success. The stock market runs on perceptions — and everything from a restaurant’s interior design and logo to its EPS and DPS figures contribute to current and potential investors’ opinion of the operation.

ABOUT AARON ALLEN & ASSOCIATES

Aaron Allen & Associates is a leading global restaurant industry consultancy specializing in growth strategy, marketing, branding, and commercial due diligence for emerging restaurant chains and prestigious private equity firms. We work alongside senior executives of some of the world’s most successful foodservice and hospitality companies to visualize, plan and implement innovative ideas for leapfrogging the competition. Collectively, our clients post more than $100 billion in sales, span all six inhabited continents and 100+ countries, with locations totaling tens of thousands.