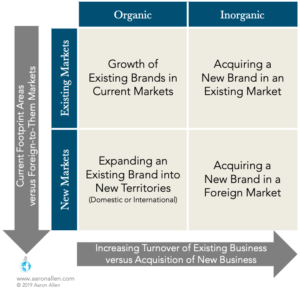

There is a spectrum of opportunities for restaurant acquisitions available for operators and investors alike.

Savvy investors can look at this time of uncertainty as an opportunity to broaden the landscape of potential attractive acquisitions. While some may be moving into this scenario opportunistically — smelling blood in the water — the most successful are realizing that this can be the perfect timing for a mutually advantageous acquisition to optimize portfolios and gain market share.

We are seeing a variety of opportunities across geographies, categories, cuisines, and phases of the business lifecycle. And just as hunters do not wait until they’re hungry to go out hunting, preparing for this flurry of investment activity ahead of it kicking off lays the foundation for a successful hunt.

The M&A fever is catching and burning white-hot from foodservice tech startups and corporate venture capital initiatives to budding emerging brands and the consolidation of mature and distressed brands around the world.

We think foodservice-related investments can be grouped into one of three types.

Some investors could be interested in all three buckets, or in certain angles of just one. There is going to be capital that wants to operate and knows how to integrate well into existing platforms, but there are others who need specialized expertise to manage a new system (that may even be in a different segment, category, or geography). The best data and advisors can help with each or all investment buckets and to propel organizations and investors forward.

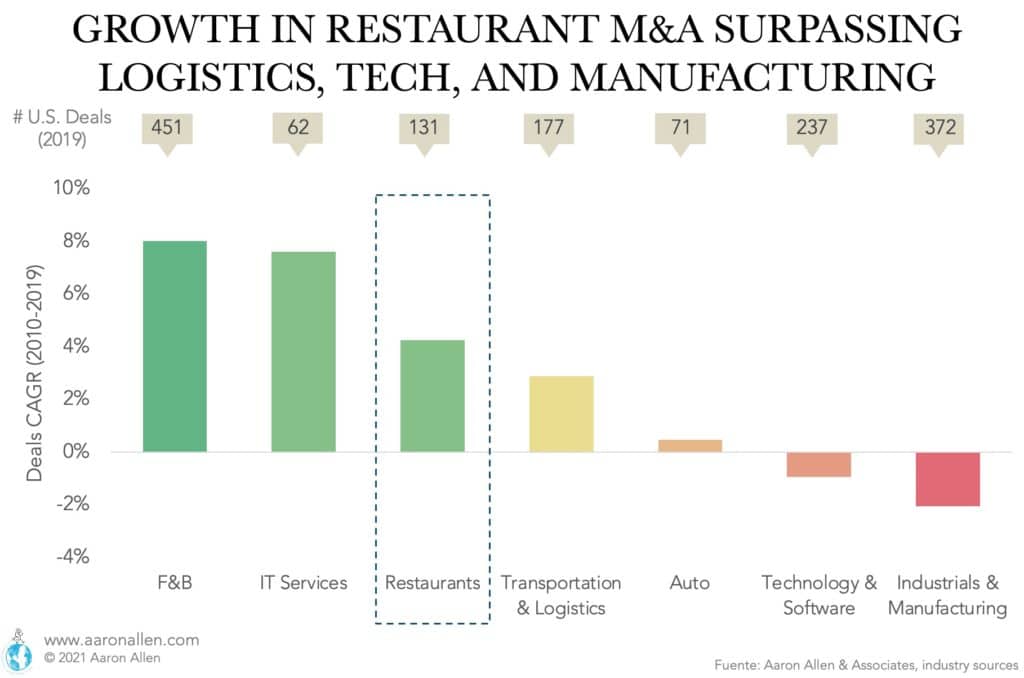

M&A activity has ebbs and flows, especially in the foodservice space, but there is a trend for consolidation. Forward-looking executives are using mergers and acquisitions to fortify their operations: achieving top-line growth, consolidating market share, and adding necessary technological capabilities. The deals being made today will have a profound impact on the future of these organizations.

M&A activity across all sectors remains around $3.5 trillion globally (versus a peak of $4 trillion in 2018). Restaurants account for a small piece of this activity around the world — and it’s in the tens of billions for the U.S. foodservice market. Deals in the food and beverage industry grew at a 9.7% CAGR between 2010 and 2017, while the restaurant portion of that sector enjoyed 6.6% growth over the same period.

Emerging brands are studying incumbents and segment leaders for weaknesses to exploit — and some are, successfully. Those with size and scale are throwing their muscle and might into buying more muscle and might. Look no further than foodservice technology, where McDonald’s, Yum, and Starbucks have each made sizeable acquisitions over the past several years.

There are many explanations for this harried pace of M&A activity:

As interest rates rise and margins shrink, organic growth will become harder and harder to achieve in saturated categories and markets. Though restaurants have been gaining a steady share of stomach year-by-year in most geographies, the battle for the biggest piece of that share is escalating. In mature markets, the slugfest is brutal and unapologetic among existing restaurant chains all while grocery stores have started to fight back.

While industry growth is stable and steady, some sub-sectors and categories may be characterized by a sometimes-gruesome competition. In some environments, it’s more dangerous to stand still than to take calculated risks. Even frontier economies are quickly moving from fragmented to chain-dominated, and restaurants will have to do even more to stand out from their competitors and strengthen their systems with growth in size and scale.

This period of inexpensive capital and global opportunity is coming to an end, and leadership teams face a stark choice: execute a robust and aggressive acquisition plan to grow quickly or try to survive the squeeze against larger and/or more agile competitors that used this moment to lay the groundwork for a secure future. Acquisitions make strategic sense only if these moves are backed by solid due diligence and forward-looking strategy.

For mature brands, M&A offers expansion and consolidation opportunities. In the U.S., this is the case of many casual dining restaurants — 33% of pre-COVID deals (2018-2019) involved targets in the full-service category. In other cases, deals are often more focused on growth companies. This strategy has been successful for the fast-casual sector in the past and is increasingly starting to benefit the companies that have a “future of foodservice”™ angle to them — whether that’s technology, innovation and optimization in the front and back of the house, improved unit-economic model, or delivery companies (which have received a tremendous amount of capital investment over the last few years).

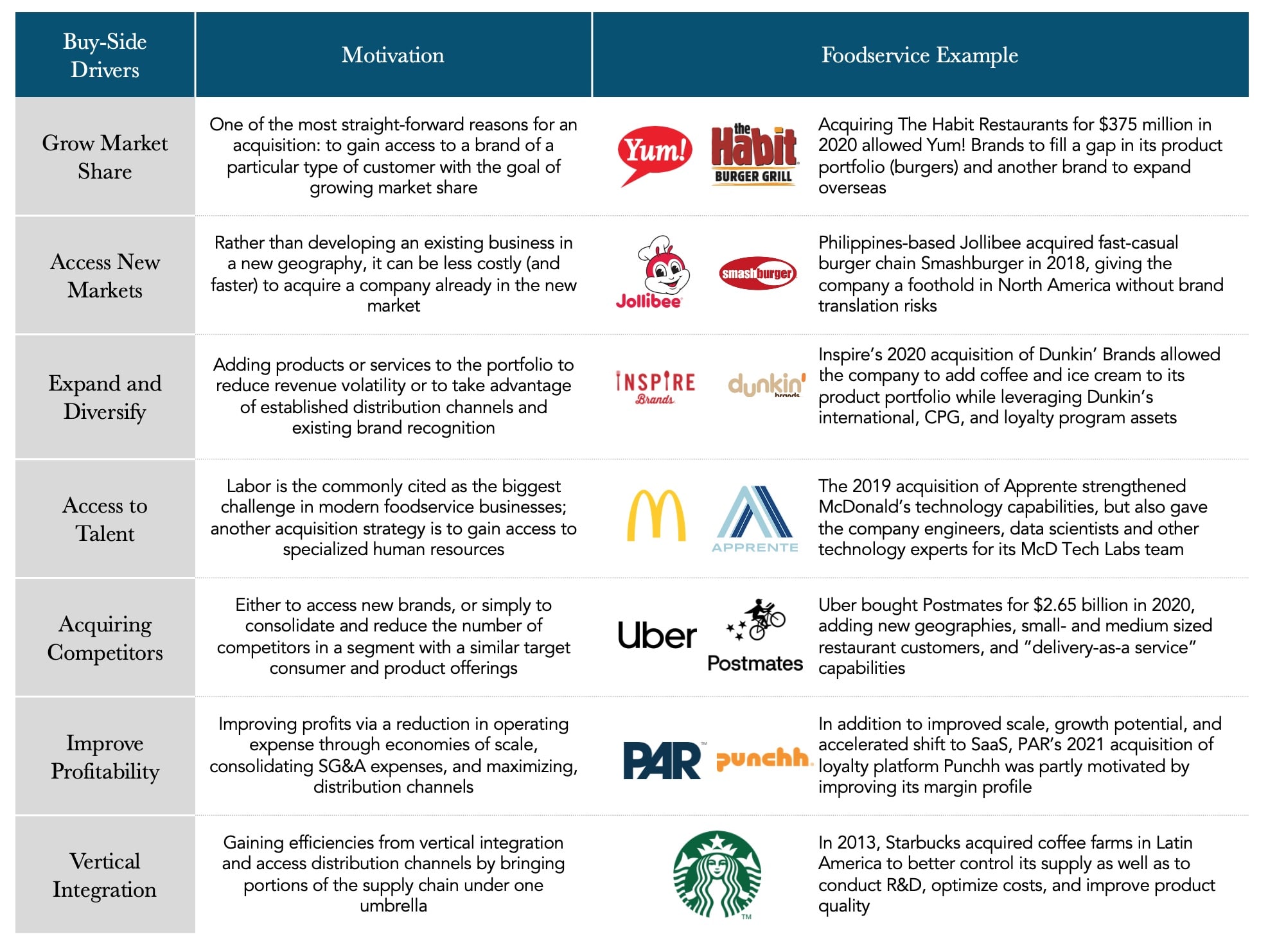

There are a variety of factors that influence mergers and acquisitions decisions, whether focused on mainly strategic or financial motivations. While these drivers for M&A are not necessarily new, understanding the evolving landscape helps to identify non-traditional value creation opportunities and a better assessment of risk.

Consolidation in sectors enables companies to gain market share which can then help from a management point of view and optimizing overhead. In other cases, investors put more of a focus on reducing costs. Next, we present some of the benefits motivating restaurant M&A.

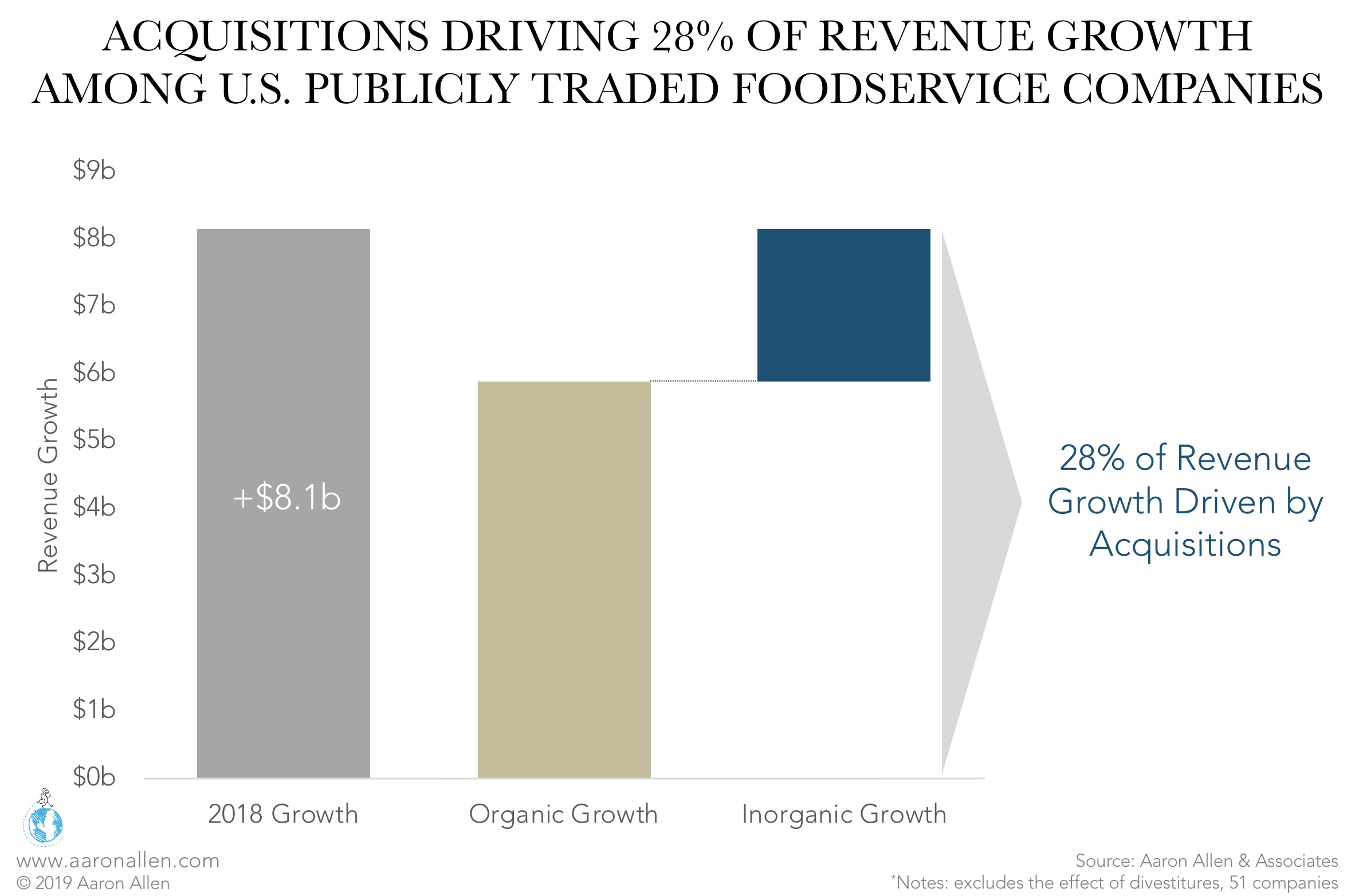

When organic growth may be hard to come by, acquisitions can keep overall company revenue lines climbing steep slopes. An existing concept comes to its new owner with all its tangible and intangible value — from units and equipment to menus and brand — as well as its customer base with it. Combined, these new additions to the original portfolio accelerate revenue growth.

In 2018, revenue growth among publicly traded foodservice companies in the U.S. amounted to $8.1b (+7% year-over-year growth, from $122.1b to $130.3b). Inorganic growth (from acquisitions) was responsible for 28% of the increase. In the increasingly saturated U.S. market, inorganic growth will continue to have significant impacts for both private and public companies.

Consolidation is a major theme across foodservice, from the declining casual-dining segment to the booming delivery sector, and we expect this trend to accelerate. This strategy is especially useful for mid-sized firms hoping to increase their market share.

Example: In April 2018, rumors of a merger between DoorDash and Postmates began swirling. As of February 2018, Postmates controlled 9.1% of the U.S. delivery market while DoorDash claimed 13.9%. Their combined 21% would push them ahead of Uber Eats, which controlled 19.9%, and solidify their lead on Amazon (4.0% market share).

HelloFresh successfully completed a similar strategic acquisition when it bought Green Chef in March 2018. The purchase helped HelloFresh pass Blue Apron and become the largest meal-kit company in the U.S.

Acquisitions can be a means to penetrate foreign markets or new segments or categories “without doing the work” and spending time setting up a supply chain, establishing a location strategy, testing the new concept, etc.

Example: Amazon purchased the Middle Eastern e-commerce firm Souq in July 2017, giving the U.S.-based firm access to 45 million users in a region where online purchasing is growing at record speeds. E-commerce doubled between 2015 and 2017, and it is projected to post growth rates above 20% through 2021.

Amazon’s acquisition strategy also helps it gain a foothold in segments it has struggled to penetrate. Recognizing the growth of home delivery for groceries — 70% of shoppers are projected to buy at least some of their food online by 2025 — Amazon launched Amazon Fresh in March 2017. By November of that year, it had discontinued service in nine states, with some employees privately blaming the U.S. Postal Service. The acquisition of Whole Foods is giving Amazon another shot: with brick-and-mortar stores to serve as hubs and independent contractors working as drivers through the Amazon Flex program, the company is set up to claim a significant share of this new market.

Adding brands to a portfolio can bring new kinds of guests into a system’s orbit.

Example: Coca-Cola has been buying up and developing new beverage lines for almost two decades. From Odwalla (2001) to Honest Tea (2008) and coffee shop leader Costa Coffee (2018), the undisputed soda-champion is trying to reach more health-conscious customers.

These purchases, alongside the in-house development of brands like Dasani, give Coca-Cola an opportunity to sell to every consumer.

When Marriott International bought its former rival Starwood Hotels & Resorts in 2016, it acquired all Starwood properties — physical and intellectual. In the fourth quarter of 2016, Marriott reported a $42m increase to the bottom line and a 47% revenue improvement. In addition to the revenue and profit benefits Marriott reaped with the Starwood acquisition, it also got its 21-million-member-strong SPG loyalty program.

Foodservice is still undergoing seismic shifts and the pace of change is expected to continue — if not accelerate — in the coming years, sparked not only by even more transformative technological developments but also by the arrival of Gen Z, set to become the largest demographic group in the U.S. in 2019. Acquisitions can help companies keep pace with the evolving industry, and Starbucks’ handling of its Teavana acquisition is a key case study in this strategy.

Example: Since purchasing the tea company in 2012, Starbucks has integrated its products into its own units, building Teavana into a $1b brand. Where the parent company failed was in developing and nurturing standalone units: the real-estate strategy focused primarily on malls, which continue to suffer from declining traffic. In July 2018, Starbucks announced that it would close all 379 Teavana locations. Some were quick to classify this as another example of Starbucks’ spotty acquisition history, which includes Evolution Fresh juices and the La Boulange bakery.

But the company’s pivot from retail locations to grocery-store sales shows a canny understanding of market trends (and its solid understanding of corporate M&A strategies). Not only does the move rescue the brand from the graveyard of shopping malls, but it also gives Starbucks a new line of retail revenue, especially key after selling the rights to coffee sales in groceries to Nestle in May 2018.

As recently as 2009, some restaurant operations still saw their online presence as optional. At the NRA conference that year, Sally Smith of Buffalo Wild Wings said her organization would take a wait-and-see approach to social media. Such an attitude today feels incredibly outdated: the question isn’t whether to integrate technology, but how to do it. Acquisitions are a surefire way to add technology to an operation.

Example: As venture capital has increased in popularity over the past several years, corporations have also gotten in on the game. There are many merits to building a corporate venture capital (CVC) group, and it’s not just generating future financial returns. The right CVC investment can unlock new layers of growth, open channel expansion opportunities, or drive improved systemwide efficiencies through new technologies. Several foodservice companies have pursued CVC programs because of this, including Starbucks, Chipotle, and Yum Brands. Other foodservice companies like McDonald’s have been actively investing in technology startups the past several years, including the acquisition of Dynamic Yield (predictive analytics) and Apprente (voice recognition).

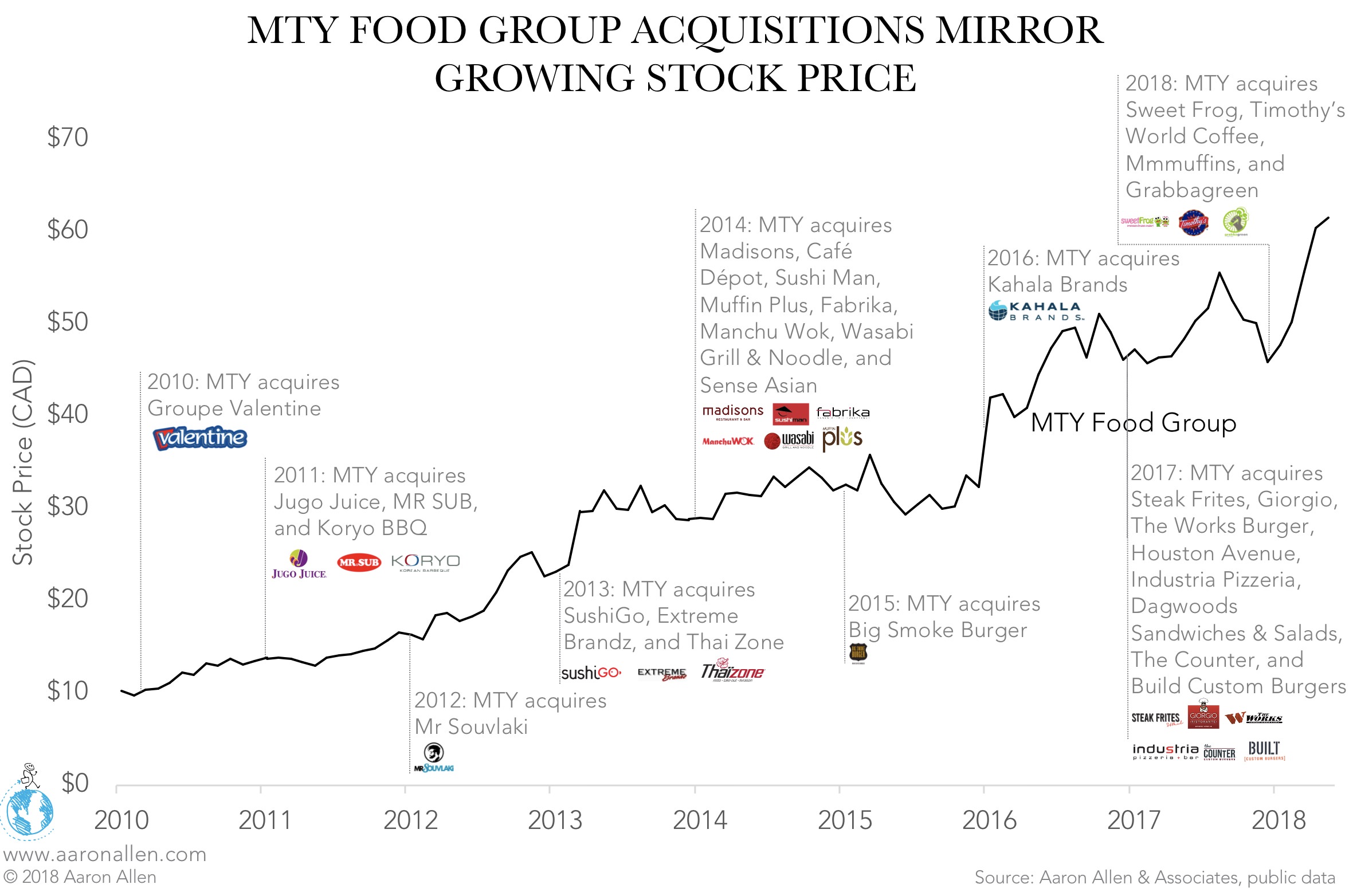

For multi-brand portfolios that want to add new concepts, acquisitions skip the development and proof of concept phase and go right to expansion.

Example: This strategy seems to motivate the massive MTY Food Group, which now controls over 70 brand names. In November 2017, it added two burger concepts, The Counter and Built Custom Burgers, to further expand its portfolio.

Other players in the food and beverage space are making similar moves. In May 2018, Kroger supermarkets spent $700m on Home Chef, a Chicago-based meal-kit company that already delivers 3 million meals to people’s homes every month. Home Chef will continue its original business while making its products available in Kroger grocery stores, allowing the chain to access the growing meal-kit sector, which is expected to have $10b in revenue in 2020.

By 2015, intangible assets, which include intellectual property and goodwill, accounted for a staggering 84% of the S&P 500’s value. This shows a 394% increase in 40 years. Globally, the most profitable businesses are those in the idea and knowledge economies, and value increasingly comes from brands and trademarks. Acquiring restaurant operations out of bankruptcy can revive still-valuable IP, adding its value the purchaser’s portfolio.

Example: In 2017, Landry’s won an auction for Joe’s Crab Shack and Brick House Tavern, spending just $57m for the two brands. With 95 locations open at the time, each unit cost Landry’s approximately $600k, a steal considering the concepts’ reported $3.1m AUV in 2013.

IP-focused acquisitions are also heating up the delivery space. In January 2018 Uber Eats bought New York-based start-up Ando; a company spokesperson explained that “Ando’s insights will help [Uber’s] restaurant technology team as we work with our restaurant partners to grow their business.” As delivery companies continue to consolidate, we’ll see more large platforms buying smaller competitors for access not only to their proprietary tech but also to the data they’ve collected on consumer behavior.

Large firms may make small acquisitions to consolidate market share, buy out competitors, or enter new markets. Many of the deals mentioned here qualify as bolt-on acquisitions, in which a smaller operation is integrated in a larger organization’s supply chain and distribution network. That’s the strategy General Mills is following as it adds brands like Annie’s Organic Foods, Larabar, and, most recently, Blue Buffalo Pet Products. The deals let General Mills enter the organic and healthful market and give the acquisitions access to many more retail outlets.

For this reason, lower middle-market leaders often look for a larger company to acquire them. As operations transition from emerging to emerged brands, they often find their capabilities — in human resources, marketing, supply chain, and governance — stretched their breaking point. They’ve gotten too big to keep staffing levels low and lean, but they’re still too small to completely fill out the corporate structure. Being bought out by a larger organization, with greater managerial capabilities, might be the safest way to grow.

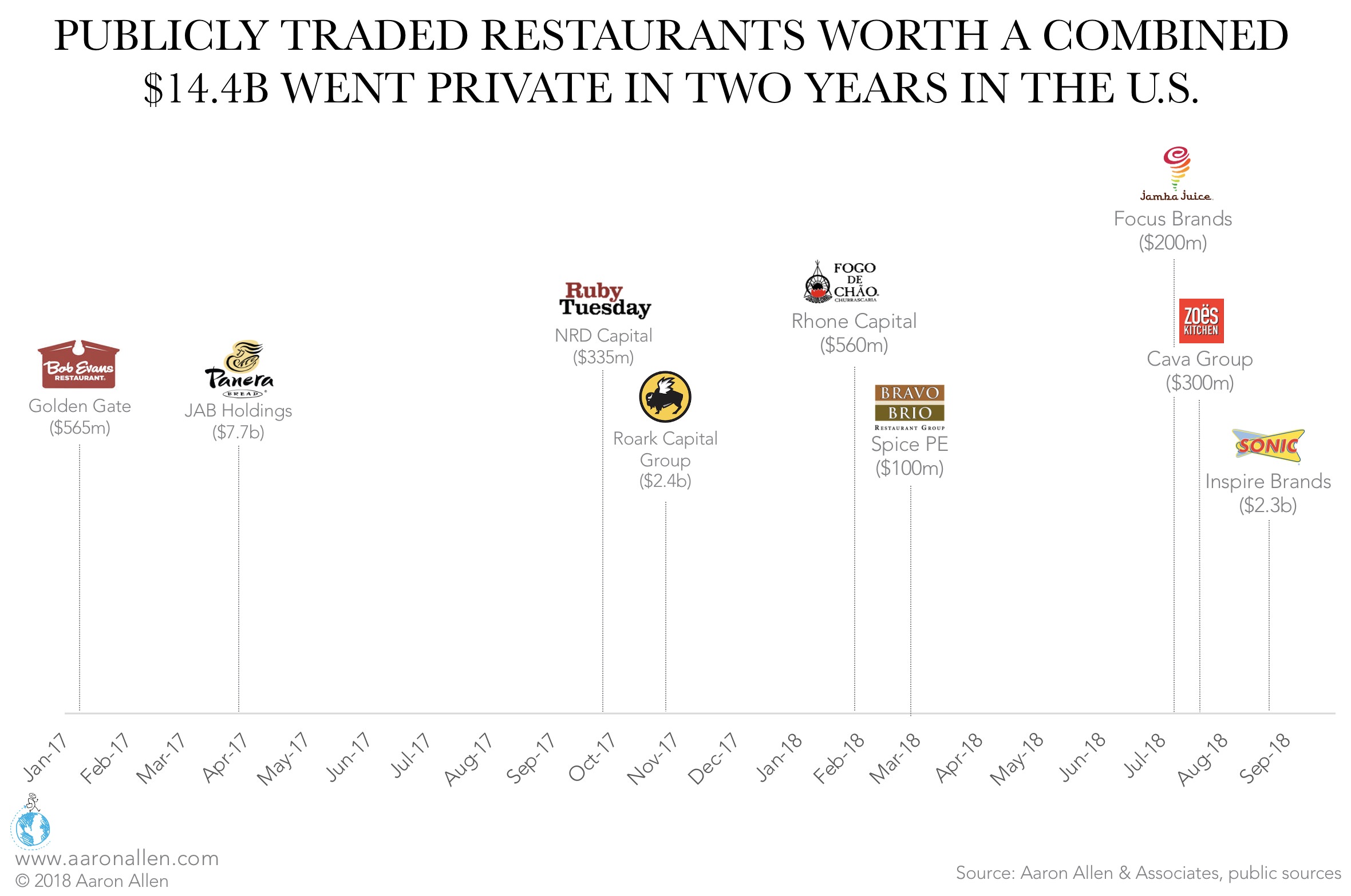

Example: In the world of foodservice acquisitions, few firms have been as active — or as focused — as JAB. Since 2012, the German holding company has been building a coffee-and-bakery empire. Starting with Peet’s Coffee and Tea in 2012, JAB has bought up Keurig Green Mountain (2015), Krispy Kreme Doughnuts (2016), Panera Bread (2017), and most recently Pret a Manger (2018). Besides gaining market share in the café-bakery segment, JAB is also pushing competitors to make big moves of their own, as Nestle’s massive, $7b distribution deal with Starbucks demonstrates.

The deal between Krispy Kreme and Insomnia Cookies, announced in July 2018, is a perfect example. With over 1,000 locations globally, Krispy Kreme is more than five times the size of Insomnia, which has almost 200. Both organizations contribute unique capabilities to the deal: besides its standalone locations, Krispy Kreme sells its frankly perfect donuts in grocery and convenience stores, and Insomnia specializes in late-night delivery. More than that, Krispy Kreme, which has been in the business for more than 80 years, can help Insomnia move seamlessly out of the lower middle market as they transform from a start-up to a mature brand.

The deal between Krispy Kreme and Insomnia Cookies, announced in July 2018, is a perfect example. With 1,400 locations globally, Krispy Kreme is more than ten times the size of Insomnia, which has just 135. Both organizations contribute unique capabilities to the deal: besides its standalone locations, Krispy Kreme sells its frankly perfect donuts in grocery and convenience stores, and Insomnia specializes in late-night delivery. More than that, Krispy Kreme, which has been in the business for more than 80 years, can help Insomnia move seamlessly out of the lower middle market as they transform from a start-up to a mature brand.

This isn’t the easiest way to make money, of course: turning around a struggling restaurant concept, especially one in the casual-dining sector, is a task only the bravest in the industry are willing to take on. But the potential rewards match the challenge, with a successful turnaround creating ten- to twenty-fold returns on investment.

In March 2018, Spice Private Equity acquired Bravo Brio Restaurant Group for $100m. The last registered valuation for the company was 2.8x (EV/EBITDA) as of December 2017 — well below the industry median of 10.6x. These fire-sale prices offer the new owners an incredible opportunity to build value over the holding period. If Spice can bring Bravo Brio’s valuation up to just the industry median, without making any EBITDA improvements, it would result in a more-than-doubled enterprise value.

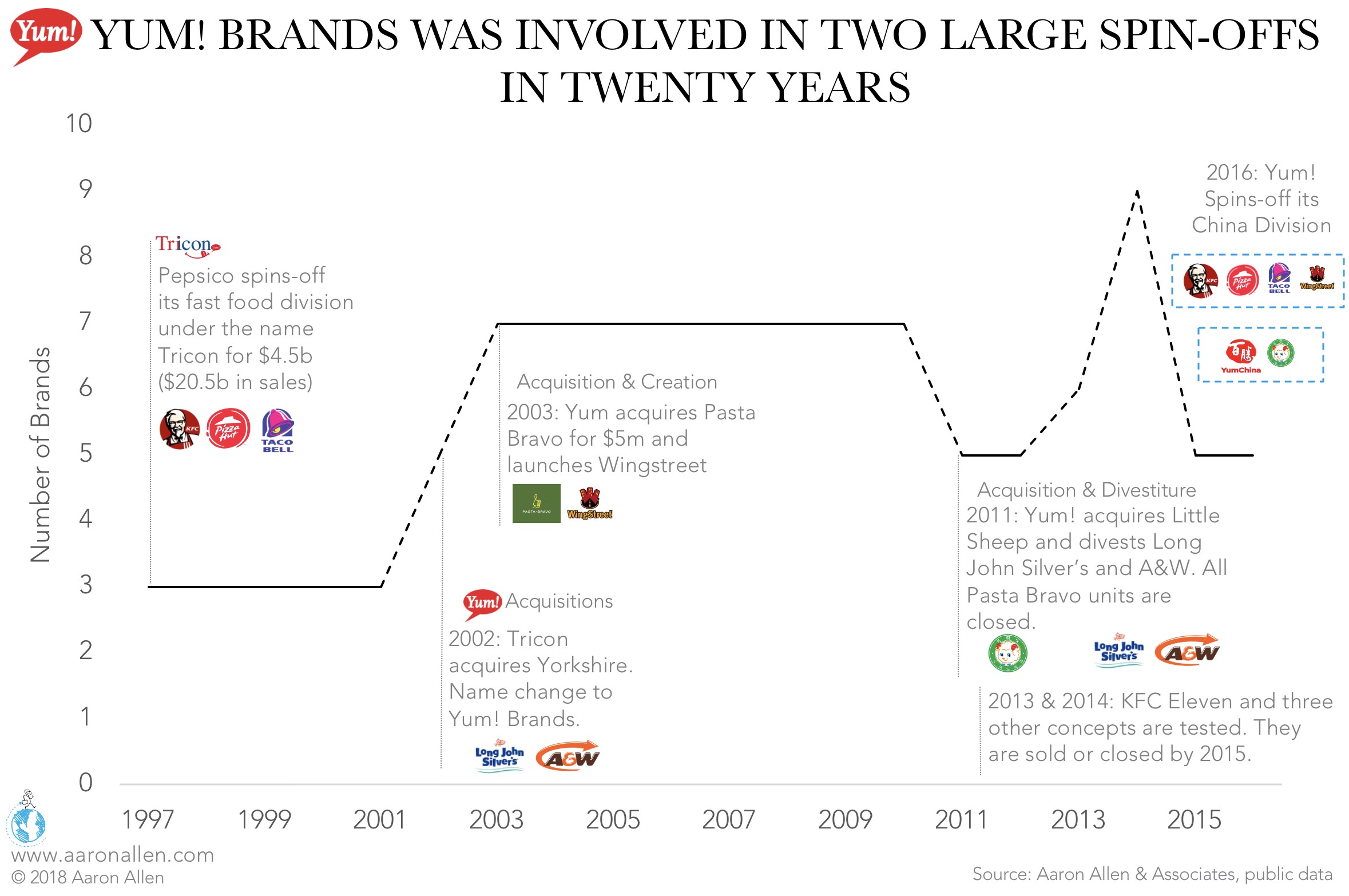

The history of Yum! Brands isn’t a story of strategic acquisitions; it’s actually a case study in smart, perfectly timed divestitures and spinoffs. Yum! Brands started as Pepsico’s fast-food division, which was spun off as Tricorn in 1997.

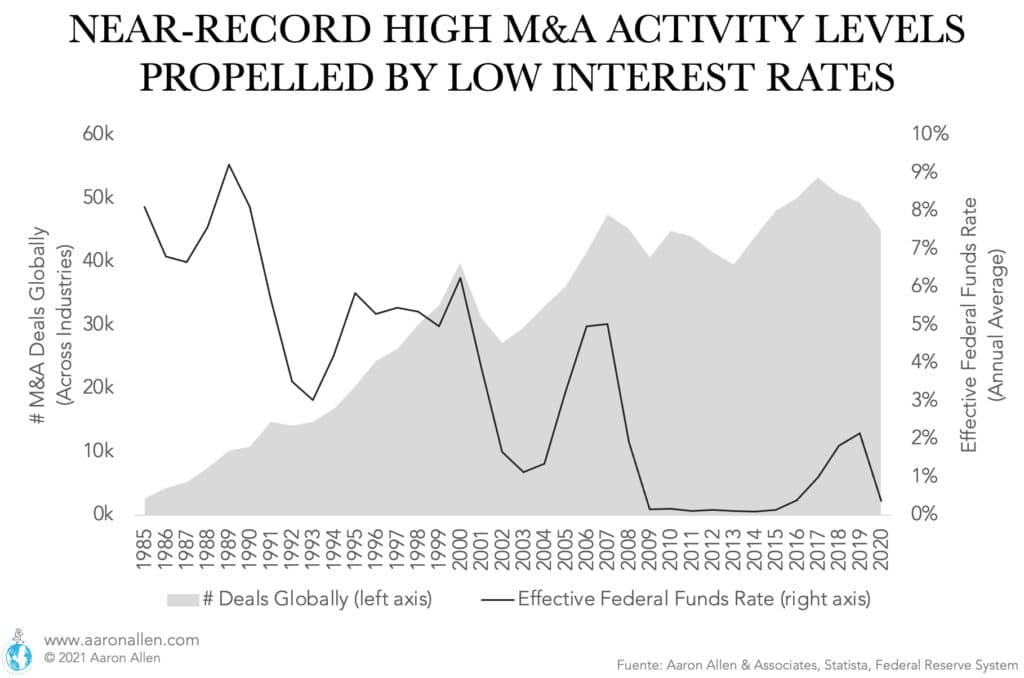

Restaurant M&A activity was white-hot from 2017-2019. However, the rise of investments in the foodservice industry had started long before. The number of restaurant M&A deals in the U.S. increased by 86% between 2004 and 2016.

Initially, it looked like 2020 would be a down year for M&A activity in the foodservice industry due to hardships caused by the COVID-19 pandemic, but lower interest rates and ample dry powder (both corporate and strategic) drove a big recovery in deal activity during the second half of the year.

Below, we’ve included some takeaways from recent years’ M&A activity in the restaurant industry.

Though the foodservice M&A activity slowed down in 2022 compared to 2021, there were still plenty of deals happening. Firstly, a significant number of franchisees changed hands. Secondly, fast-casual was a very active segment (much more than QSR or full-service). Thirdly, there were several high-profile deals happening outside the U.S. (including McDonald’s Russia sale, Autogrill-Dufry merger in Europe, and BlinkIt merger with Zomato in India.)

Even with higher interest rates and a more challenging economic environment, private equity, venture capital, family offices, and institutional investors are getting deals done.

The M&A activity surged back in the restaurant industry in the U.S. in 2023. There were a number of acquisitions evenly distributed across segments, from snacks to fast casual to full-service and QSR. There was also a lot of activity among franchisees for QSR brands (including some bankruptcies).

There were a few significantly large transactions including the Subway acquisition by Roark Capital for $9 billion plus earnout and some debt, the acquisition of Tao Group for $550 million, and Darden acquiring Ruth’s Chris Steak House for $715 million.

2024 saw a bounce back in restaurant M&A:

Inorganic growth is key in mature markets like the U.S. where growth only comes at someone else’s expense.

More companies have gone private than public in recent years, and the volume and value of M&A activity continues to rise.

When Ron Shaich announced his resignation as CEO of Panera Bread, he explained that he wanted to “really push this debate… about how short-termism has infused our capital markets.” The focus on short-term results, he went on, “stops innovation. It stops the very things that drive economic growth. And it makes us less competitive as an economy.” This is why Shaich took Panera private: so the company could focus on more complex, long-term strategies like digital integration that may reduce more immediate payouts but can significantly increase future returns.

Shaich’s harsh words for the industry have made the merger between Zoës Kitchen and Cava, financed by Shaich’s Act III, huge news. The two Mediterranean concepts have a combined footprint of almost 350 stores. Though Zoës has struggled with declining traffic, especially in regions where over-expansion resulted in self-cannibalization, Shaich’s involvement in this deal signals that the chain still has a lot of potential.

We’ve also seen this with Inspire Brands, another multi-concept portfolio under the Roark umbrella which acquired Dunkin’ Brands for $11.3 billion in 2020. It adds coffee (Dunkin’) and ice cream (Baskin Robbins) concepts to an empire that already includes Arby’s, Sonic, and Buffalo Wild Wings. The group has a proven track record for bringing back struggling concepts: since the Arby’s turnaround began in 2013, the roast beef restaurant chain has increased sales by 20%.

CEO Paul Brown focused on making the brand more appealing for young people: social media became less corporate, more emphasis was put on high-quality ingredients, and stores were remodeled (which also helped with efficiency). Like Shaich, Brown is focused on longer-term strategy, acquiring a multi-billion company every year and integrating them efficiently. The company is already the fourth-largest restaurant company in the world (and they only got started in 2017).

The volume and value of M&A activity continues to rise. With trillions sloshing around in the global private equity and alternative assets markets — and the rise of family offices with fortunes to invest — it is no surprise that the foodservice industry is a hot target.

What’s also shaping up though, is that investors, analysts, and innovators alike all share a sense of optimism and enthusiasm for the convergence of technological advancements, rapidly evolving consumer dining behaviors, massive stockpiles of corporate cash and investment capital, and the opportunity that spells for future of foodservice type investments.

The foodservice industry is being reshaped globally by delivery, self-ordering, alternative foodservice formats, tech-enabled turnarounds, and quickly changing dietary preferences. We’ve all read plenty about that. But, what not everyone is seeing yet is just how much more the performance of the industry, experience for the guest, and returns for investors can be as these trends accelerate and combine with other emerging ones to create super-trends.

Here, we take a look at some recent M&A activity to identify patterns and look broadly at the benefits and outcomes of companies accelerating growth through strategic acquisitions.

Restaurant mergers and acquisitions deals are gravitating more towards strategic buyers (rather than purely financial investors): the share of strategic deals increased 16% between 2004 and 2016. That suggests that a level of understanding (one supported by a specialist with knowledge of the external and internal factors affecting restaurants today and tomorrow) will be much-needed for deals in the future. We’ll likely see even more restaurant M&A deals in the future, thanks to more funding flowing into the space.

More investment is being placed into high-growth concepts — those in categories like snacking and coffee, rather than in slumping segments like casual dining. Outdated concepts in saturated sectors will struggle to find buyers, while on-trend concepts will likely prove to be the most worthy investments.

Restaurants with no physical locations have been cropping up around the country, largely in response to the success of delivery platforms like UberEATS and GrubHub. For restaurant concepts, the move is a win-win. A recent report by Fast Company found that many fast-casual restaurants dedicate 75% of their stores to seating, while some 90% of their customers take their meals to-go. A “ghost” storefront — in which customers can order their meals to have it delivered, but never actually go in the restaurant — certainly solves that problem. It also remedies high rent costs, as delivery-only units don’t necessarily have to be located in busy, walkable (i.e. high rent) locations.

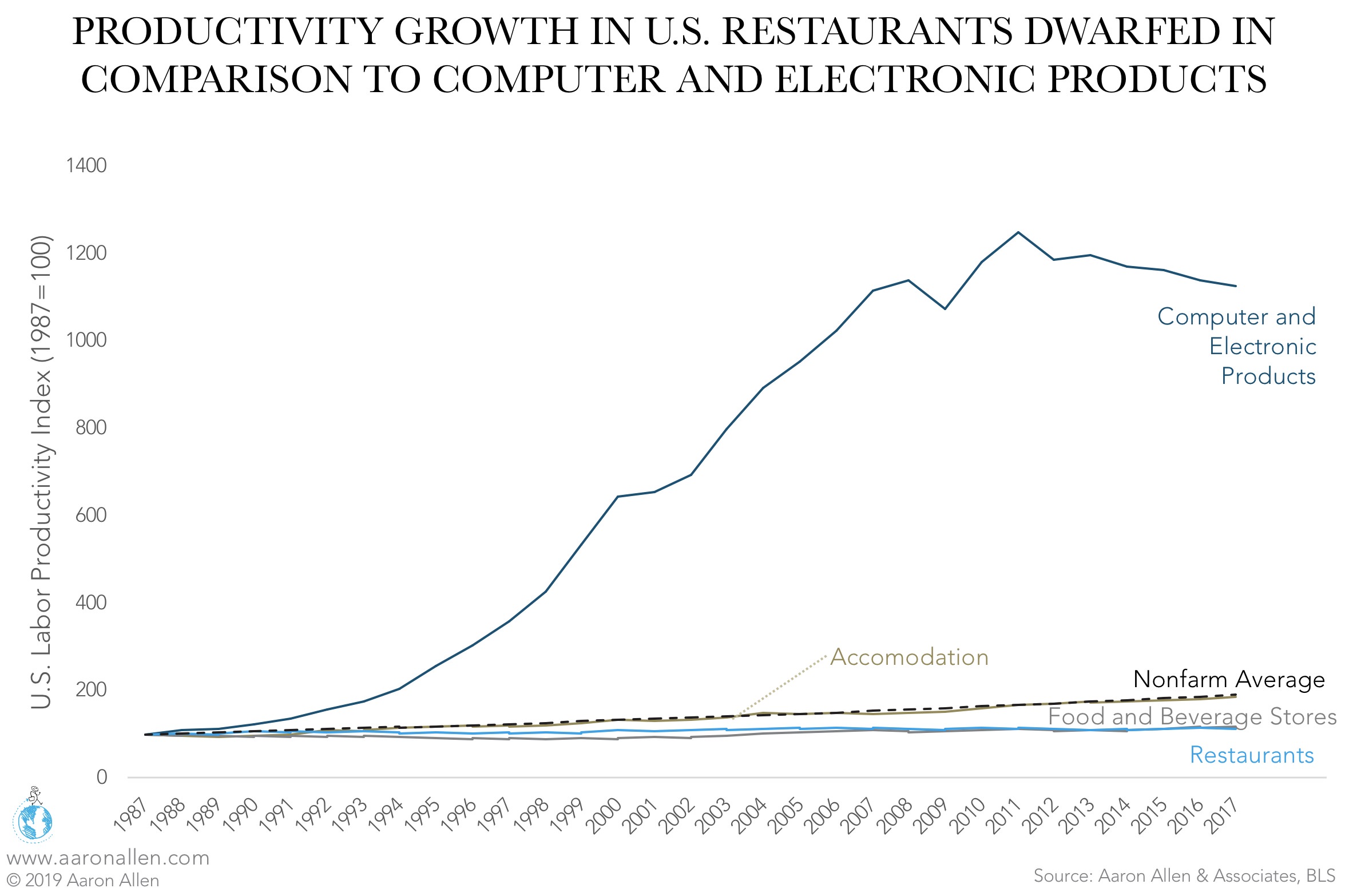

While other sectors have historically seen significant increases in productivity, improvements in the foodservice industry have been minimal over the last 30 years. The Second Industrial Revolution benefited the industry (overall) with improvements in agricultural production. The Third Industrial Revolution, where consumer and electronics products led growth, had a very slight impact on foodservice, with the adoption of the point of sale system — most of which are really a glorified cash register.

But the sector is now in a prime position to make modernization efforts with the impacts of the Fourth Industrial Revolution and — in doing so — is becoming a more attractive target for investment.

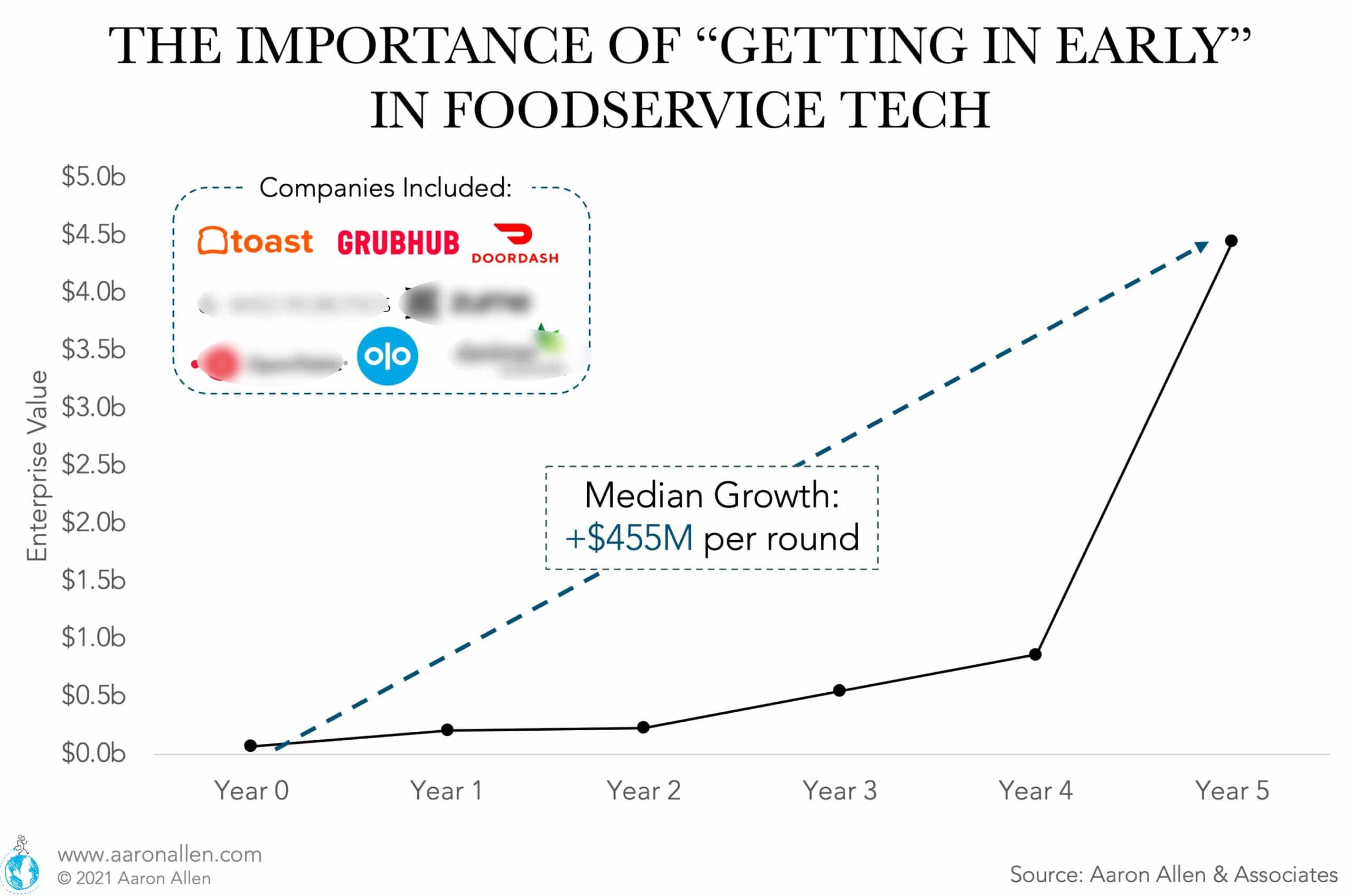

In our view, we’re still living in the bronze age of foodservice tech, where most of the category’s success stories are largely-delivery focused (including DoorDash, GrubHub, and Olo). However, as operators begin to rethink their operating models for a post-pandemic world and may be more open to new technology solutions, there are several reasons to be bullish about the future of foodservice tech investing:

We took a small sample of foodservice tech companies (including categories like delivery, POS, robotics, SaaS, and more) and calculated that on average, enterprise value grows $455 million per funding round (from Seed Round and Series A onwards). Investors getting in early can see huge valuation growth.

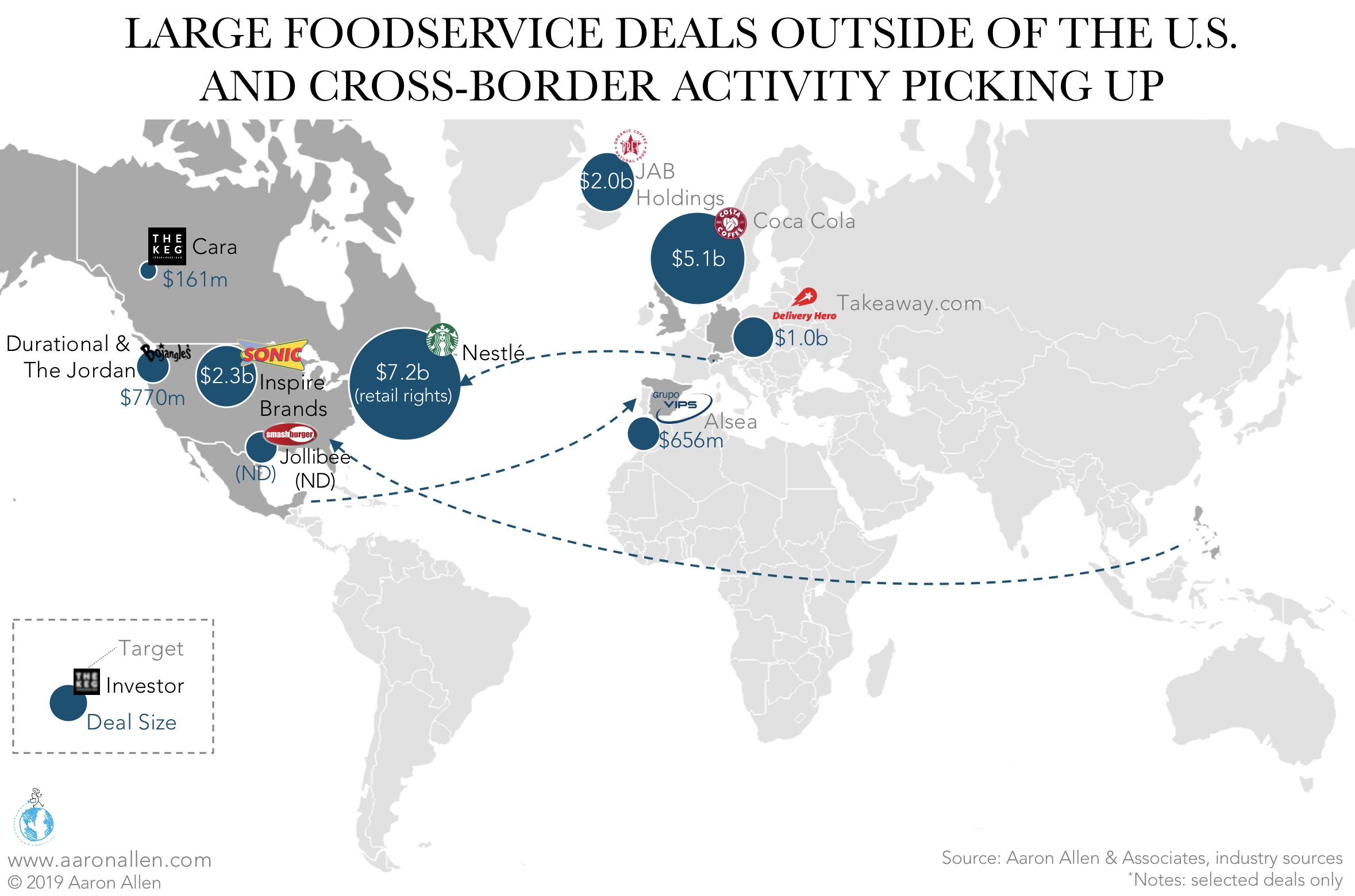

Jollibee, for instance, finalized its acquisition of Denver-based Smashburger in 2018. The company initially tried to expand to other markets and they met unforeseen challenges and struggled because customers outside of the Philippines were unfamiliar with the brand. But Jollibee does know QSR operations well, so they looked for an opportunity in the U.S. with a large enough footprint to gain scale.

Larger foodservice groups have been using cross-border transactions to grow for a while now. Growth in the U.S. for large established companies is at a point of saturation — any new units for one brand are coming at the expense of someone else. So inorganic growth and foreign expansion are the greatest opportunities.

We anticipate more foreign buyers coming to the U.S., and U.S.-based investors making further investments globally. This strategy is a way to gain immediate access to a footprint, infrastructure, talent and human resources, and a regionalized know-how.